Private Equity, Care Platforms, and the Future of the Physician Practice

In case you missed it, I sent Hospitalogy’s first newsletter on Tuesday, but I think it was sent to spam for a lot of you. Dang deliverability issues! You can read it here. I covered HCA’s bad Q1, Humana’s hospice sale of Kindred, and the unraveling of MercyOne by Trinity and CommonSpirit.

New here? Subscribe to Hospitalogy today.

What’s next for the physician practice?

Are we repeating the mistakes of the 90’s era physician practice management companies?

After reading Jan-Felix Schneider’s excellent piece on the death of physician independence, I went down the rabbit hole researching physician employment dynamics, the current transaction space, and the 1990’s physician practice management crash to make a more educated opinion on where I think the physician practice is headed in the coming years.

Let’s get after it!

Intro

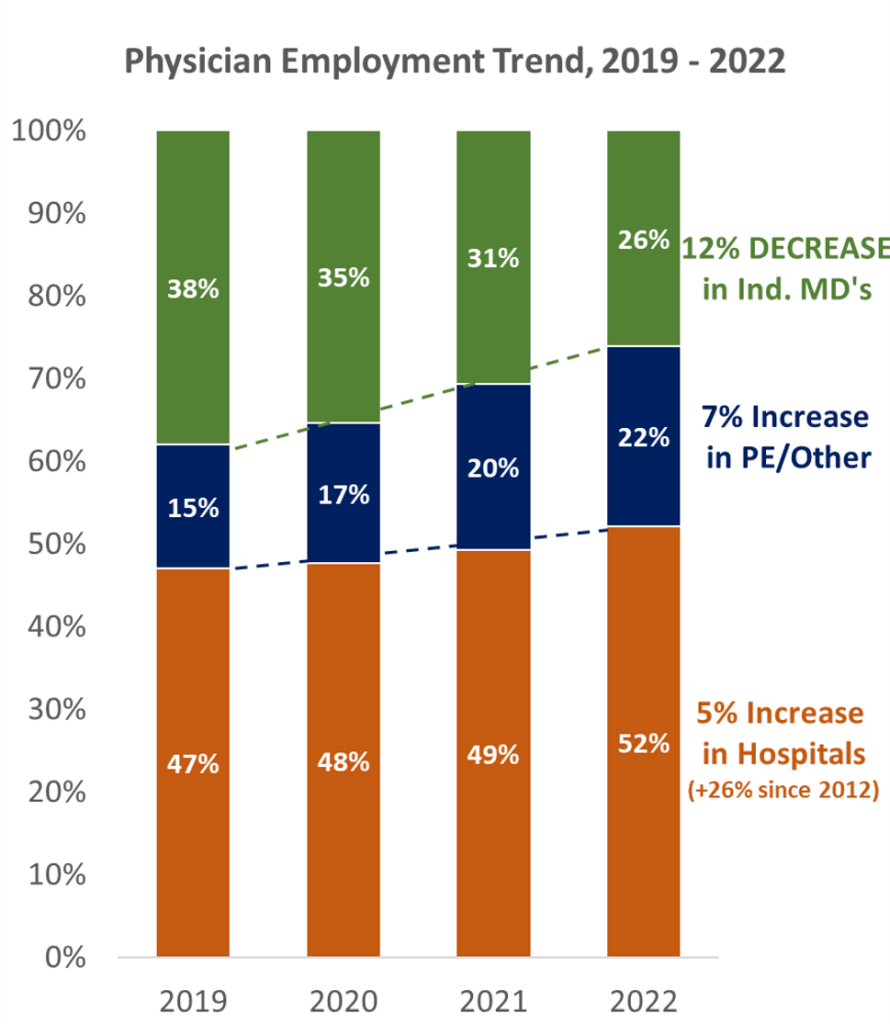

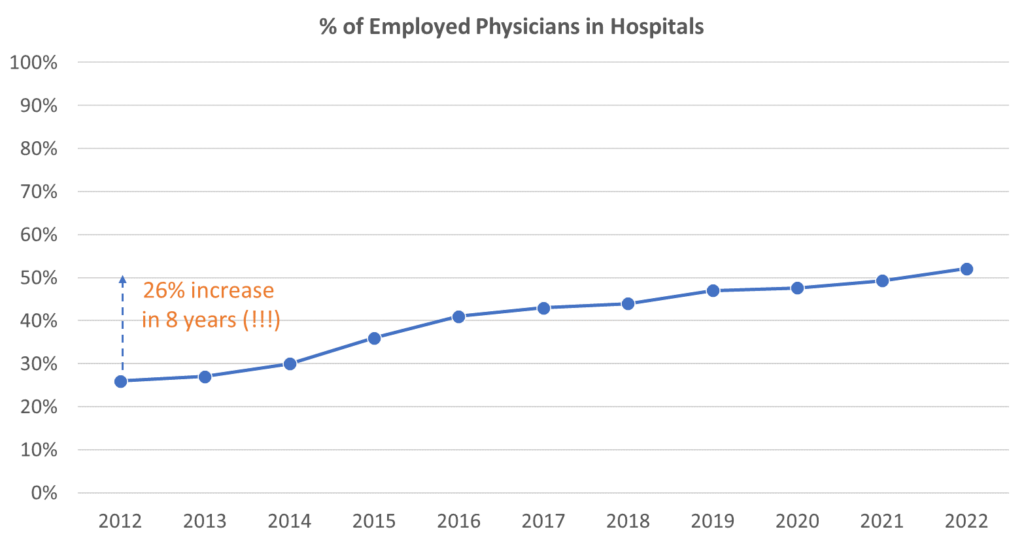

More healthcare players than ever are crowding the physician M&A space to scale and gain market share. Corporate and hospital employment of physicians is accelerating like crazy, similar to the roll-ups of the late 90’s (shout out PhyCor). Employment of physicians has increased 19% over the last 3 years, accelerated by ‘Rona.

- In fact, basically 75% of all physicians are now employed by a hospital or corporate interest.

Current market dynamics are creating bidding wars for physician practices of all sizes, and an aging, retiring physician base is looking to cash out. These dynamics create a perfect storm of events for physician practice M&A to accelerate, which has definitely happened since the pandemic.

As a result of this acceleration, physician practices are, and have been, in red-hot demand. Hospitals and corporate interests are bidding up physician practice valuations. There are a lot of organizations trying to make a quick buck and grow as quickly as possible, which will lead to repeating the sins of PhyCor and MedPartners.

On the other hand, many PPMs are much more sophisticated operators when compared to 90’s operators. Value-based care and capitation arrangements are not so new anymore, and population health strategies are now being encouraged and incentivized by CMS and others.

My Thesis

There will be a reckoning for certain bad players in PPM land, but the best operators will survive and thrive by growing at responsible levels and being prudent in their M&A strategies.

For the worst operators, physicians will grow increasingly difficult to manage. The inorganic growth unbound will lead to cultural clashes between employed physicians and their bosses among the operaters who can’t successfully integrate. The culture issues, always overlooked, will result in AT LEAST a partial unraveling of the physician practice roll-up and employment trend.

Most importantly, players who fail to produce organic growth once M&A dries up will see their equity values crumble, leading to a physician exodus from the platform.

My hypothesis above begs the question: what’s next for the physician practice?

Because this rapid M&A dynamic is unsustainable, I’m predicting that the physician employment pendulum at least partially swings back toward independence. An opportunity will arise for new-age care platforms and startups who are building out resources to enable the independent physician practice once again.

- AKA, creating the ‘Shopify’ for physician practices, which would provides all of the necessary tools for a physician to operate successfully in an increasingly hostile environment while dealing with expense pressures and reimbursement pressures on the top line. While it’s not a perfect analogy in healthcare, it works for grasping the scope of what these platforms are trying to do.

Background of PE groups & Physician employment

Hospitals, private equity firms, insurers, and new-age care platforms are snatching up physician practices across the nation. Since ‘Rona, over 83,000 physicians left their independent practices to join one of these entities.

Join the thousands of healthcare professionals who read Hospitalogy

Subscribe to get expert analysis on healthcare M&A, strategy, finance, and markets.

No spam. Unsubscribe any time.

- The employment trend isn’t slowing down.

The Physician Acquisition Playbook.

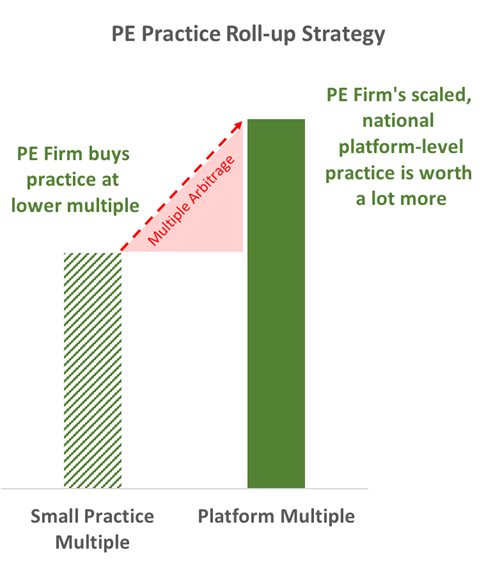

Why physicians? Physician practices USED to be super fragmented with small independent groups scattered across the nation. Fragmentation meant that PE firms or other care platforms could acquire smaller practices (AKA, one or two man physician practices) for lower multiples, then add that practice to their larger platform, which is valued at a higher multiple. It’s a similar model in hospitals with downstream pick-up leading to higher patient revenue.

Private Equity 101: The PE playbook tends to work something like this: Raise funds → use those funds to create a physician practice management platform → make a splashy first acquisition of a larger physician practice in that particular specialty → finance tuck-in acquisitions via debt → acquire smaller physician practices at lower multiples via a combination of cash and equity → practice earnings are immediately worth more because the scaled platform co. commands a higher multiple → adjust comp and improve the expense structure of all acquisitions → sell the platform business to another PE sponsor or strategic player.

On the physician and clinical side, physicians don’t want to deal with the hassle of back-office and administrative tasks. Practice management companies have an easy sell – “Let us do the heavy lifting for you. We’ll take a bite out of your collections off the top, but you’ll be able to focus on care and leave work with fewer headaches.”

This thinking led to the creation of PhyCor, MedPartners, and other PPMs in the 90’s, and the same thing is happening today. It’s a great idea for a business model, but execution has to be strategically sound especially in any model involving physicians.

At this point, Private equity players have created large practice management companies across a number of physician specialties. Private equity (PE) is now heavily involved in healthcare. Among all industries in 2021, healthcare investments represented about 14% of total PE transaction activity. What started as investments in high-margin specialties like dermatology, fertility, and ophthalmology has expanded into every type of physician practice – even including lowly primary care.

Private equity-backed groups aren’t the only firms engaged in this strategy. As the ACA fueled industry consolidation, this trend is playing out across a number of healthcare services verticals. It’s just most apparent in physician practices right now, where employment is approaching full capacity.

- For instance, publicly traded companies like LHC Group, U.S. Physical Therapy, RadNet, and others perform tuck-in acquisitions all the time. Buy at a 5x, those earnings are instantly worth 9x at the platform level. Boom – immediate multiple expansion. If integrated successfully, of course.

Things Fall Apart?

Here’s where my thesis comes in to play: the physician tuck-in playbook is starting to fray as a multiple arbitrage opportunity, and the late 90’s PPM crash may (partially) repeat itself. We’re already starting to see some groups dissolve, just like PhyCor in ‘99.

PE-backed provider groups, Optum and other managed care orgs, and new-age care platforms have joined the physician practice M&A black hole, driving up tuck-in multiples. Translation: physicians have more options than ever to sell their practice OR align with a care platform like Privia. As a result, the historical market dynamics for physician M&A have shifted:

- There’s an insane amount of cash floating around and way too many players with cash to burn. Optum can probably outbid anyone and is a valuable strategic partner – too valuable for selling physicians to ignore. Just ask Kelsey-Seybold and Atrius physicians.

- Spiking demand for physicians, inelastic demand of physician services, physician willingness to sell to private orgs, and new primary care reimbursement models all are increasing speculation. These factors are forming a huge disconnect between valuation and actual practice performance – whose margins are suffering from medical supplies inflation, staffing shortages, & ‘Rona volume headwinds. Those paying inflated multiples will be left holding the bag.

- Not only are new reimbursement models, quality metrics, and other regulations increasing speculation, they’re also fueling administrative complexity. That complexity necessitates a sophisticated management partner to navigate if you want to participate in these arrangements.

- Most physicians selling their practice are on the tail end of their career and view selling the practice as a retirement / transition plan. The younger guys and gals kind of get screwed, since they don’t have existing equity in the practice and don’t have a say in their future employer. These are the physicians that will likely leave the practice, go off on their own, or seek employment elsewhere. The big question here, of course, is whether or not younger physicians are content with current employers, or if they’ll jump ship.

- So what happens as a result of the above? Culture issues. People don’t leave jobs. They leave bad managers. Certain care platforms, especially in private equity where there’s a higher likelihood for profits, volume, and cash flow to be prioritized, are most likely underestimating culture and clinical integration issues when tucking in newly acquired practices. This issue is similar to what happened in the late 90’s. Those buyers that fail to do proper diligence or piss off physicians will see their platforms crumble. You don’t want to piss off physicians. Physicians have short memories. Yes, they just received a lump sum payment for their practice, but once their equity value shrinks and comp/profitability is affected, problems inevitably begin.

So you can see why overpaying for a physician practice could be problematic. As multiples expand ever upward into the sky, PE portfolio companies and VBC players will have to operate more efficiently OR negotiate higher reimbursement to justify higher platform-level multiples. Platform multiples will start to creep up into the ‘too expensive’ realm…17x, 18x, 19x. In my mind, the days of getting by on inorganic growth through M&A seem to be coming to an end, and it’s pretty hard to grow a physician practice organically. Private valuations are artificially high, and I’m of the opinion that this trend is unsustainable.

If multiples don’t expand, ROI will decay and PE margins will shrink.

- Undoubtedly, certain late-to-the-game care platforms and PE firms looking for growth unbound will continue to snap up physicians at bad prices. As I said before, players overpaying for physicians will be left holding the bag, and the bag will literally crumble, spilling out all of the physicians to once again do as they wish with their practice.

Based on the trends outlined, I’m expecting to see the following consequences:

- At least a few private PE-care platforms will go public over the next couple of years. These now-public platforms will correct quickly, affecting private valuations.

- Private valuations SHOULD come down a notch as interest rates rise and entry multiples expand unless PE players are successful in increasing prices and operating more efficiently, patient care aside – thus justifying higher platform multiples. Adjusted EBITDA can only go so far, even for financial gurus with magical Excel fingers.

- Some private equity roll-ups will fail or declare bankruptcy, giving physicians an out and once again increasing the level of independent physicians.

My take: the current boom of physician practice management is approaching its tail end as physician employment nears full capacity.

Physician Practice Management players to watch: Oncology roll-ups like GenesisCare, OneOncology (Link) U.S. Radiology. U.S. Anesthesia Partners, Ophthalmology roll-ups like AEG Vision, Retina Consultants of America, American Vision Partners, etc. Finally, other specialties like gastroenterology and GI Alliance, fertility, dermatology, or urology.

PE-backed firms already publicly traded include The Oncology Institute, ATI Physical Therapy, and Mednax. Without really even needing to look, I can tell you that their stock prices are performing incredibly poorly since going public.

Bottom Line: The physician practice roll-up trend will lose its runway over the coming years, creating an opportunity for new enablers of independent physician practices. While there may not be a crash landing, I’m definitely expecting some money to be lost.

Thanks for reading, and feel free to reach out with any hot takes, vehement disagreements, or reinforcement of the above.

Resources:

- Physicians Advocacy Institute report on physician employment.

- PwC M&A report on health services.

- Brookings Institute report on Private Equity investment in physician practices.

- A history of PhyCor

Miscellaneous Maddenings

- Today I learned that Jupiter rotates 2.5 times faster than Earth despite being 11 times as large!! Insanely cool to see them rotate side-by-side. How is that possible?

- Deutsche Bank is predicting a mild recession in the U.S. on the back of a rise in interest rates to 5-6%. I mean, the Fed’s hands are tied at this point. How else can we counteract 8.5% inflation other than to hope that it just goes away?

- Elon Musk officially bought Twitter, which seems to be more controversial than I was expecting.

- For all my Wordl-ers out there, I got ‘Heist’ in 2 the other day. First guess being ‘Noisy’ finally pays off baby!!

- Any Apex fans in here? Respawn dropped a new teaser for Season 13 this week.

Hospitalogy Top Reads

- This was an absolutely fantastic read on the present and future of risk-based businesses in healthcare by Jacob Effron. It also ties in to this write-up – there’s a lot of steam for risk-based arrangements going on.

- To save on space, health systems are increasingly targeting malls to scale outpatient footprints.

- The House introduced the Telehealth Extension and Evaluation Act, which would expand current telehealth loosened regulations from the public health emergency over the next 2 years.

- The AHA published an eye-opening, data-driven article on inflation and massive growth in expenses that hospitals are facing. This article goes hand in hand with what I’ve been saying about inflation over the past month and also reinforces HCA’s bad Q1.