Welcome back to another edition of Hospitalogy, where we dive into the business of healthcare twice a week!

Join 9,900+ thoughtful healthcare professionals, executives, investors, and consultants from leading organizations and stay on top of the latest trends in healthcare. Subscribe to Hospitalogy today!

Walgreens, Summit Health, and a $10B price tag?

Do you hear that? The M&A rumor mill is swirling once again! This time, it’s a substantial one. Walgreens is reportedly in talks to acquire the massive healthcare organization Summit Health. According to unnamed sources first reported by Bloomberg, the deal would value Summit between $5B and $10B. Yes, billion with a B.

So why the huge price tag? Just take a quick look at the highly attractive organizational footprint that Summit Health has built with its physicians:

- 2,800 providers

- 80+ specialties

- 13,000 employees

- 370 locations (urgent cares + clinics)

Summit operates an expansive footprint throughout most of the Northeast (New Jersey, New York, Connecticut, Pennsylvania, and Oregon). Backed by Warburg Pincus, Summit was formed in 2019 through a merger of Summit Medical Group, a huge multispecialty physician practice management company, and CityMD, a huge urgent care platform (this is a really nice breakdown of the deal).

Since 2019, Summit Health has almost doubled in size. At the time of the press release, its footprint included 200 locations and 1,400 providers. In 2018, Summit Medical Group held 1,069 providers under management and generated around $208M in revenue and $8.7M in EBITDA seeing 4.35 million patients that year. So from 2018 to now, Summit has gained more than double the number of providers! I assume the financials have followed a similar path.

Madden’s Musing: Assuming that Summit went through a competitive bid process, I’m shocked to hear that Walgreens is potentially the player that won?? There are a number of strategic buyers that would be chomping at the bit for Summit (CVS, Optum come to mind very quickly). My guess is that Optum may have had too much overlap from an antitrust standpoint. That likely wouldn’t have stopped them from responding with a bid, though.

But that still leaves CVS, and CVS has been very vocal about wanting to buy regional platforms and players to bring its clinical services footprint up to speed with the other payors. Another idle speculation – Given Walgreens’ current healthcare strategy with heavy focus on VillageMD, might Walgreens purchase the CityMD portion of Summit? It’d be a nice bolt on for VillageMD.

I’ll be fascinated to follow this storyline as it unfolds in the coming months.

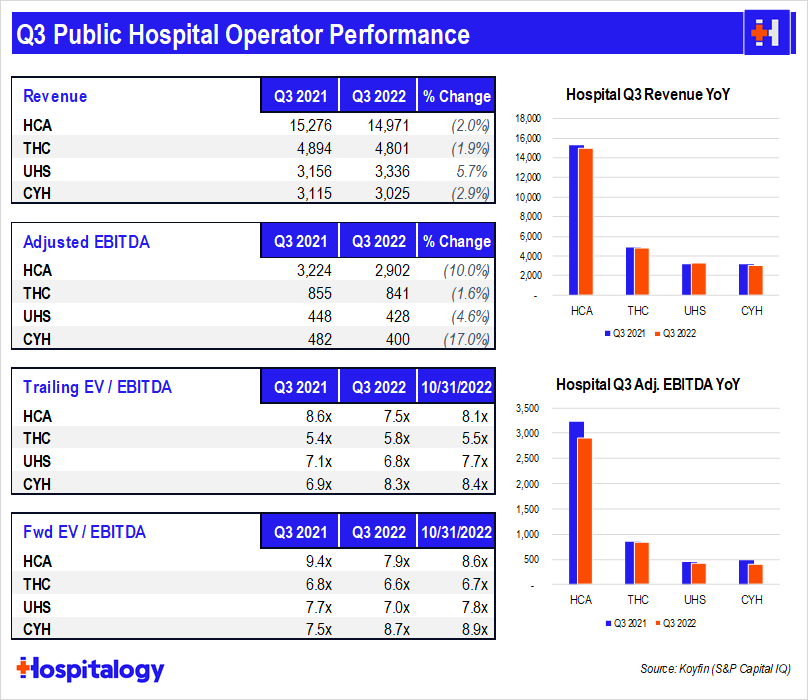

UHS, CYH Q3 earnings updates

You know the drill Hospitalogy fam. HCA and Tenet report last week, Community (CYH) and Universal (UHS) report Q3 earnings this week. Here are some quick notes and what you need to know about the earnings call:

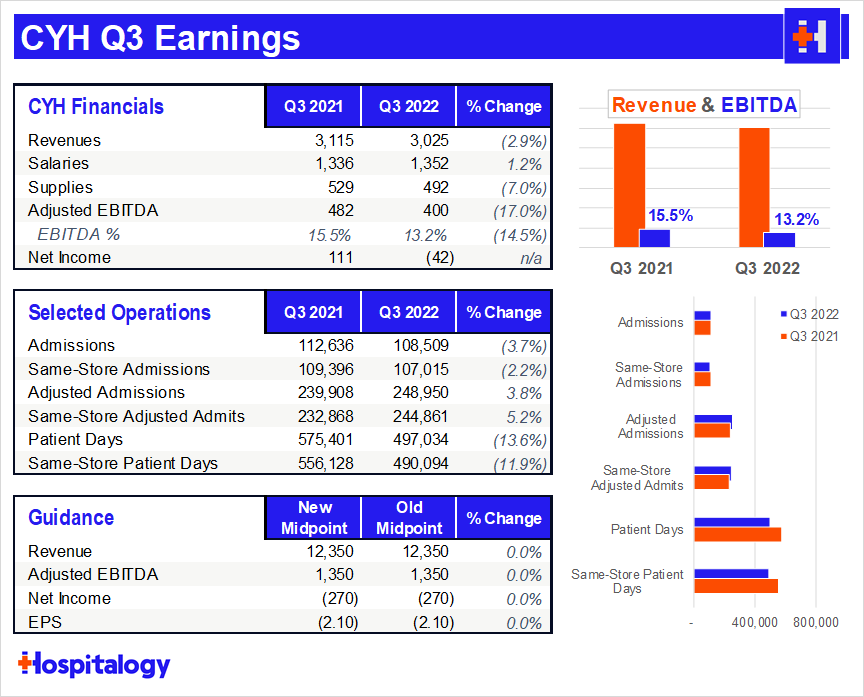

CYH:

- Big drivers: lower admissions and acuity on the inpatient side; labor and inflation crushing margin on the expense side. The hospital environment is getting better, but slower than expected.

- CYH was very happy to note they’d extinguished $267M worth of outstanding debt during Q3. They were able to extinguish that debt with just $174M in cash. Incredible. Net debt to EBITDA sits at 7.3x.

- Interestingly, CYH received about $115M in Covid relief funds from a tranche that had been announced in Q4 2021. No more relief dollars are expected for any hospital operator going forward. Excluding relief funds, CYH only made $285M in EBITDA, or 9.4%.

- Similar to HCA and Tenet, Community experienced an uptick in patient volume in Q3, most notably surgeries and outpatient visits (you can see the adjusted stats above, which adjust for outpatient, were both strong and positive). Same-store surgeries grew 5.3%.

- CYH is seeing higher acuity (note: more complex) patients with strong growth in specialties like neuro, ortho, spine, and GI.

- CYH expects contract labor to drop 50% in 2023 as it remains elevated for them in 2022. Q3 contract labor totaled $100M (7.3% of SWB) down from $150M in Q2 and $190M in Q1. RN hiring and retention rates are both improving and contract labor will drop sequentially. Amazing what can happen when you pay folks more money?

- Under its joint venture with Acadia, CYH is opening a 120-bed inpatient behavioral health facility in December.

- As far as 2023 is concerned, CYH is expecting a commercial rate lift in the 4-6% range and same-store net revenue growth around the same mid-single digit area.

- A big point of emphasis for hospital operators has been length of stay management (patients are staying in hospitals longer since there have been fewer discharge destinations with labor issues). CYH’s non-Covid length of stay is better than where it was in 2019.

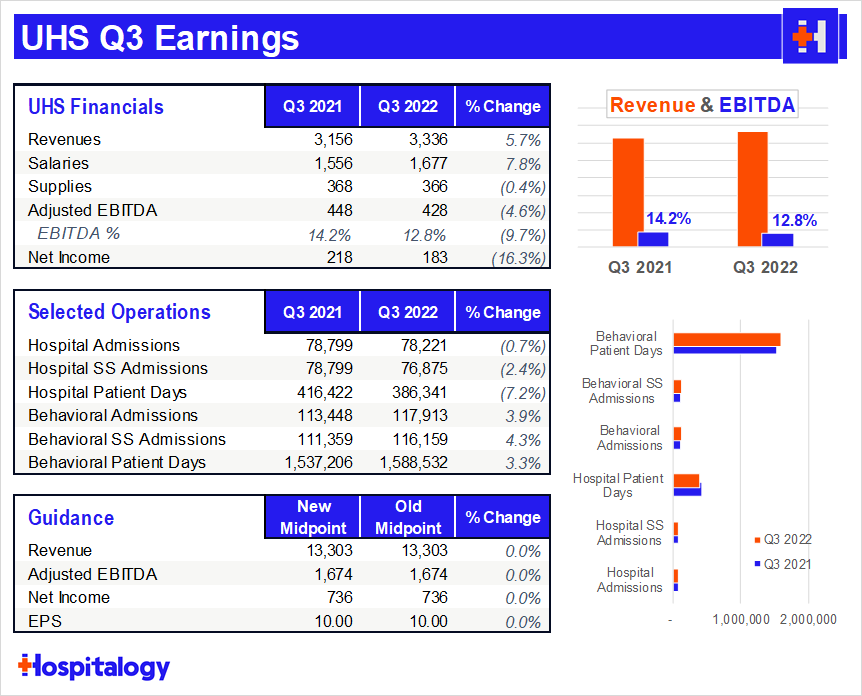

UHS:

- UHS experienced revenue softness (pressure from outpatient shift) on the hospital side. On the behavioral side, UHS saw solid growth in the quarter.

- Similarly to the other hospital operators, UHS saw contract labor costs drop from $150M in Q1 to $117M in Q2 to $81M in Q3 (just under 5% of salaries and around 10% of acute care salaries). For context, that number was ~$35M for UHS pre-pandemic. Its main, number one priority is continuing to reduce this further and filling as many vacancies as it can.

- Utilization is slowly returning to UHS facilities as a common theme across all hospital operators.

- Still a ton of uncertainty from UHS and other operators re: the 2023 effects of inflation and other economic pressures. None of them have really discussed 2023 expectations since they’re in ‘wait and see’ mode.

- UHS continues to play hardball with payors on rates, going to their lowest paying payers and demanding higher rates or otherwise terminating those contracts. Most of their larger commercial payors seem to be playing ball with them on rates.

- “I think most of our not-for-profit peers are struggling financially, and then that may be an understatement. So I think, again, the hope is that their willingness to give what we believe will characterize as outsized pay increases, they’re going to have much less of an appetite for that in 2023.” – Steve Filton, UHS CEO

Anddddd finally, here’s a handy comparison between the four pubco’s:

Resources:

- CYH Q3 earnings press release

- CYH Q3 call transcript (paywall)

- UHS Q3 earnings press release

- UHS Q3 call transcript

Market Movers

Finance and M&A Updates:

- Pretty massive news on the PBM front – Centene is moving its pharmacy benefit services business from CVS Caremark to Cigna’s Express Scripts. It’s a major win for both Cigna, which will manage about $35B in annual prescription drug spend, and Centene, which appears to be saving on PBM management costs.

- The market seemed to react well to Teladoc’s Q3 earnings this week with improved gross margins and decent BetterHelp performance.

- Medicaid managed care player Molina has notched a string of Medicaid contract wins this year, amounting to $5.8B in additional premium revenue.

- Navvis and Esse Health, two population health management players, are merging into a NewCo called Surround Care, which will employ 1,200 FTEs across 9 states, cover 4 million lives, and work with 4,600 affiliated physicians.

- The National Nurses United union is asking the Louisiana AG to intervene in the previously announced 3-hospital transaction between HCA Healthcare and LCMC Health.

Partnerships & Strategy Updates:

- The Hospital for Special Surgery with Flare Capital launched a new virtual musculoskeletal physical therapy company, which will undoubtedly leverage HSS’ clinical footprint to create a nice downstream hybrid offering for patients. Win-win.

- The Medical University of South Carolina health system (MUSC Health) and The MetroHealth System (MetroHealth) have formed a partnership to create Ovatient, a new, comprehensive virtual and in-home care company with the aim of transforming health care delivery while building and maintaining connectivity to health systems and the high-quality care they provide

- Four anesthesia groups in the Midwest have partnered to create the Association for Independent Medicine. The group is now comprised of over 400 anesthesiologists.

- Health systems and other providers are all competing for the same labor pool alongside players like Walmart, Target, and Starbucks.

- Children’s Memorial Hermann partnered with Hazel Health. Students at schools with agreements with Hazel will be able to use the platform for virtual care and will connect with Memorial Hermann specialists for follow-up services.

- Amazon Pharmacy partnered with Florida Blue to become its exclusive home delivery provider for the Blues’ 2M+ members.

- Non-emergent healthcare transportation company DocGo is expanding its service area to more counties in the New Jersey and New York areas.

Digital Health and Startup Updates:

Join the thousands of healthcare professionals who read Hospitalogy

Subscribe to get expert analysis on healthcare M&A, strategy, finance, and markets.

No spam. Unsubscribe any time.

- Memora Health and Mayo Clinic are piloting a program to improve postpartum care in Mayo’s patients.

- Heal clinched a partnership with Cigna to provide home-based primary care services to Cigna members across several Mid-Atlantic states.

- On a similar note, Monogram Health notched a partnership with Humana to provide in-home value-based chronic kidney disease services to Humana MA members in 4 southern states.

- Dispatch Health and Home Instead (a personal care co and subsidiary of home healthcare company Honor) formed a partnership to offer Home Instead customers with Dispatch’s higher acuity service offerings (hospital at home)

- Color announced the acquisition of Mood Lifters, a mental health platform catered toward group-based therapy.

- Redesign Health launched a new startup aimed at treading autoimmune disorders called Motto.

- GeekWire scooped that Google acquired a digital health startup called Sound Life Sciences, which has developed an app to monitor breathing.

- Solera Health launched an interesting offering for women’s health that aims to address a broad spectrum of women’s health issues.

- Sanctuary Health and Awell partnered to integrate Sanctuary’s patient education library into Awell’s clinical workflows.

- Digital mental health investments hit $700M in Q3

- Elion, a company focused on becoming the marketplace for health tech stack buildout, launched this week.

Policy & Payment Updates:

- CMS is enforcing harsher nursing home penalties

- Expanding Medicaid is a popular talking point in several statewide midterm elections.

- ACA enrollment grew among minority populations in 2022

- CMS is restricting Medicare Advantage TV ads after it secretly watched them in between Jeopardy rounds and noted “huh, these are kinda shady and suck”

Costs, Data, and Other Updates:

- A new report published by Doximity found that physicians are overwhelmed by the amount of clinical material they have to keep up with. Who’s building the AI to summarize clinical papers?!

- Hospitals have reported a 300% rise in RSV cases. The flu is trending up too earlier than expected. Get your flu shots folks, it could be a rough winter.

- YouTube is working with healthcare professionals to create credible videos and combat misinformation on the platform.

Miscellaneous Maddenings

- In case anyone has been keeping track, Blake’s Bets has been doing quite poorly lately. Good thing I’m a creator and not a gambling shark am I right?

- So get this. I’m going to a wedding this Saturday. My wife offered me up to the bride to video the ceremony and speeches during the reception on my phone just to have since there isn’t an official videographer. Well…it turns out that the event planner has added me as the official videographer on the program agenda!! To make matters worse, Texas plays Kansas State right smack dab in the middle of the wedding!! Am I expected to take videos instead of streaming my Horns during the ceremony?!? A cruel twist of fate. Anyway, I’m gonna do the mature thing here but I’d be lying if I said it didn’t cross my mind…

- My wife and I were driving back from a quick Home Depot trip when we noticed this guy weaving through traffic behind us. He and his buddy sitting in the front cut us off and take the next bend at a super high speed. Well folks…it had been raining. As if I were watching in ultra slow motion, we witnessed this truck hydroplane across the median, crunch into the side of a poor car, ricochet to the right, and utterly obliterate the front of another truck in a head-on collision. My wife and I just sat there for several seconds, in absolute shock as to what we’d witnessed. By some miracle (and honestly technological advancement in car safety), nobody was seriously injured. 2 things to take away from this story: play stupid games, win stupid prizes. and 2) you’re truly in control so little in life. There’s nothing those other two cars to avoid getting hit.

Hospitalogy Top Reads

- Zach Miller wrote a great series on end-stage renal disease that I think is right up Hospitalogist’s alleys. Give the 3-part series a read here and subscribe to Zach’s newly launched newsletter, the Post-Op, while you’re at it! (Part 1 – what is ESRD?) (Part 2 – the business behind ESRD) (Part 3 – dialysis clinic economics)

- Jan-Felix dove into Medicare brokers – a massive middleman – and how there is lots of potential for change in the space.

- This was a nice read and analysis done by Trilliant Health on current utilization patterns for primary care services and demand destruction.

- Great read from Health Affairs on what happens when inflation squeezes hospital margins. Damn. It’s almost as if I’ve been harping on these points for like 6 months now. Hate them or love them, hospitals struggling financially have significant downstream effects on local economies and patient care.

Join 9,900+ thoughtful healthcare professionals, executives, investors, and consultants from leading organizations and stay on top of the latest trends in healthcare. Subscribe to Hospitalogy today!