Shout out to Pat Mahomes, Scottie, and CVS for the wins in their respective arenas this week.

- Also, in case you missed it: I wrote a comprehensive deep dive into CVS, Oak Street Health, and why vertical integration is the dominant strategy among payors in 2023. Check it out here.

Join 18,000+ executives and investors from leading healthcare organizations including HCA, CVS, and OneOncology, nonprofit health systems including Providence, CommonSpirit, and Atrium, as well as leading digital health firms like Tia, Carbon Health, and Aledade by subscribing here!

| Join the first ever Hospitalogy Virtual Panel |

| The first Hospitalogy panel is this week on Thursday – history in the making! Join the panel to hear from Herd Midkiff and Kyle Kirkpatrick, healthcare experts and partners at JTaylor with a combined 40+ years of experience. It’s gonna be a fun discussion! During the panel, we’ll cover interesting topics like: – Vertical integration emerging as the dominant payor strategy; – Hospital headwinds and current dynamics facing providers; and – How hospital M&A is changing in light of the above trends Sign up below – the panel is in 2 days, on February 16th at 11am CT! Save your Seat |

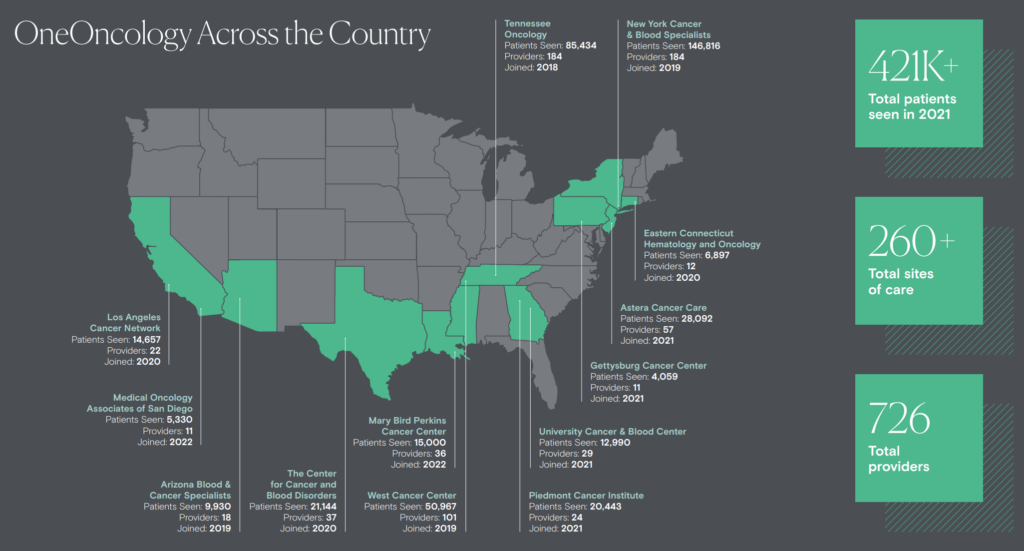

OneOncology rumored to get $2 billion price tag

Bloomberg reported on February 6th that General Atlantic is weighing a $2B sale of its cancer-specific MSO platform, OneOncology.

By the numbers: As of December 2022, OneOncology reached a footprint of 850+ physicians and APPs across 500,000 patients and 275 sites of care. Based on its 2021 annual report, that implies growth of around 18% on both a patient and provider basis for 2022 (although I should note the 2022 report hasn’t been published yet). In 2021, OneOncology affiliates generated $2.1B in practice collections across its affiliated partnerships, with $900M in additional affiliate revenue projected in 2022.

Remember that OneOncology’s model is focused on oncologist enablement – e.g., physicians retain their independence when agreeing to affiliate. In addition, all 14 of OneOncology’s practices applied to participate in the Enhanced Oncology model – the next phase of value-based care in oncology, and the successor to CMMI’s Oncology Care Model (which failed to generate meaningful savings for CMS but made meaningful progress toward value-based oncology care). That means for certain cancer treatment plans under EOM, OneOncology will help oncologists transition to risk-based arrangements and allow them to take on some level of two-sided risk.

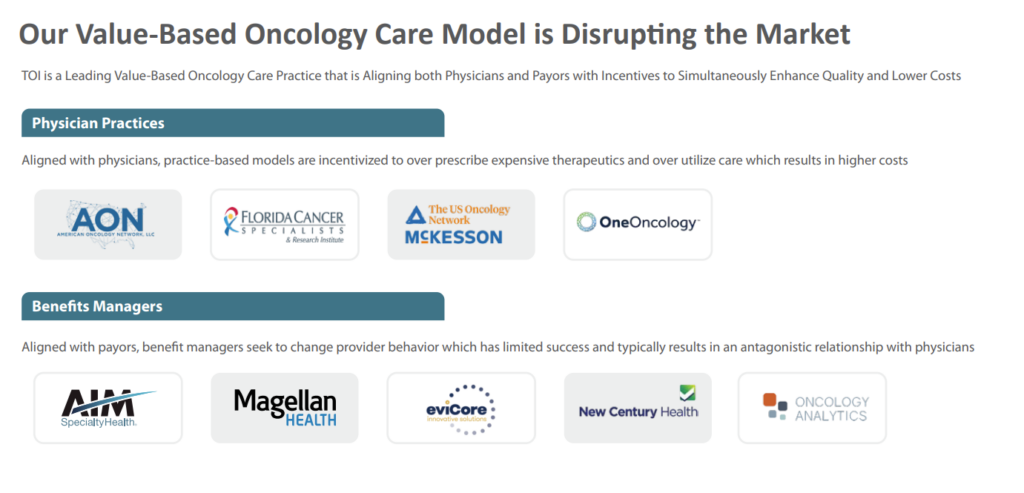

As far as the broader oncology market is concerned, keep the following players on your radar:

The Oncology Institute, which SPAC’d in November 2021 at an enterprise value of $840M with $155M in trailing revenue and $345M in 2022E revenue, implying a 2.4x revenue multiple. Unfortunately, TOI is yet another SPAC that overestimated its success in 2022. As of Q3, it dropped its full-year 2022 revenue guidance to $250M at the high end, or about a 30% cut from expectations at SPAC. TOI now trades at around 0.5x revenue and an EV of $129M. Rough. As of Q3, it operated with 74 clinic locations in 14 markets, 5 states, 111 providers. 60 of the clinics are employed by TOI while 14 are affiliated with TOI under its MSO (how OneOncology’s MSO model works; TOI is more of a ‘staffed’ model). (Prospectus) (Q3 results)

- Tough scenes for this slide (at least for now):

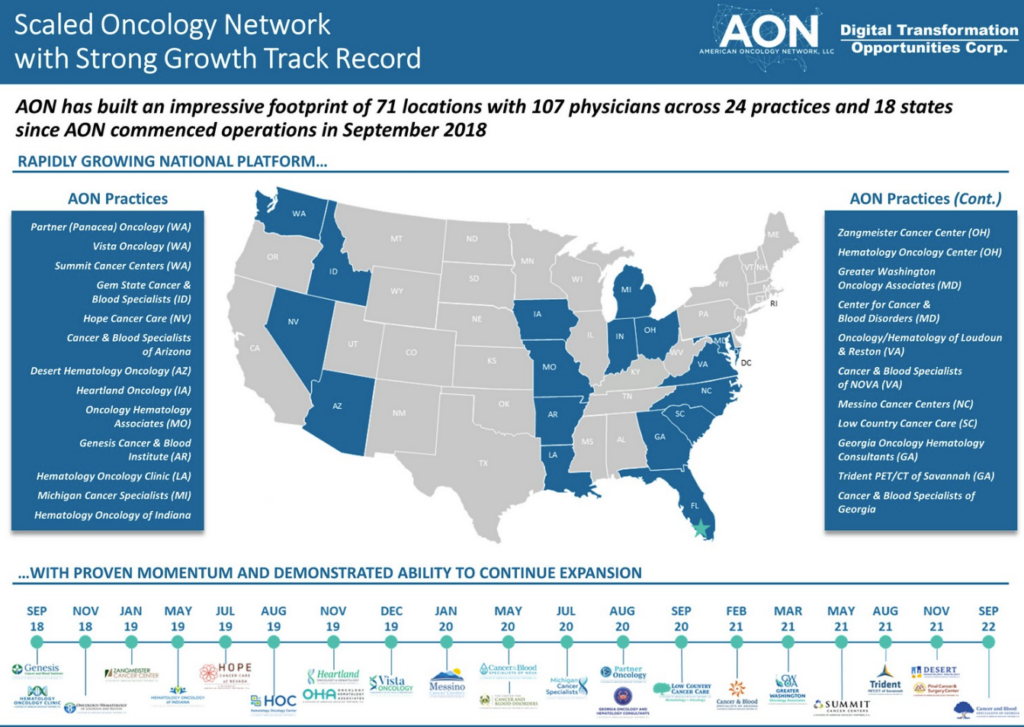

The American Oncology Network, which announced its intention to SPAC in October 2022 at an enterprise value of $497M. This deal is expected to close in the first half of 2023. In 2021, AON generated revenue of $944M implying a trailing multiple of 0.53x. It is slightly profitable, though. (Investor presentation)

The US Oncology Network, backed by McKesson, which is likely the most comparable company to OneOncology. USON just affiliated with two large independent oncology practices – Epic Care and Nexus Health – bringing USON’s total affiliated physicians to 1,400 (2,000+ total providers) across 500+ sites of care. It’s becoming increasingly obvious, as with most other independent physician groups, that there’s an immediate need for a capital partner to fuel growth/equipment needs and transition into risk.

GenesisCare, which holds a global footprint of cancer centers and purchased 21st Century Oncology in May of 2020 to boost its presence in the US to 130 centers.

Finally, another enablement and risk-based player to keep on your radar is Thyme Care. Thyme has backing from players like a16z, raising $22M in a Series A in October 2021, and I had a great conversation with Scott Voigt and Bobby Green the other day about Thyme’s business model.

Cancer care is an emerging area to watch when it comes to risk-based arrangements, and patient outcomes can be vastly improved in this arena while lowering total cost of care. The broader trend is clear: specialty care is a key area to watch in 2023 and beyond for risk.

Resources:

- General Atlantic weighs $2B sale of OneOncology (BBG – paywall)

- OneOncology 2022 performance press release

- OneOncology 2021 annual report (scroll down; I can’t link PDFs)

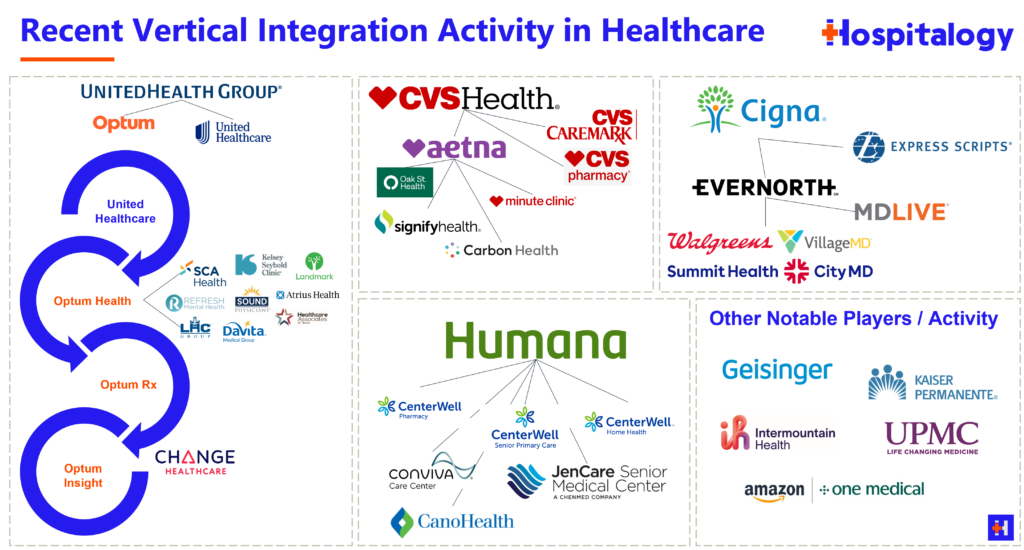

Visualizing Vertical Integration in Healthcare

I made this for the panel Thursday, but figured “why not share it now?” So here’s some of the more notable vertical integration activity among payors over the last couple of years or so:

Partnerships and Strategy Updates:

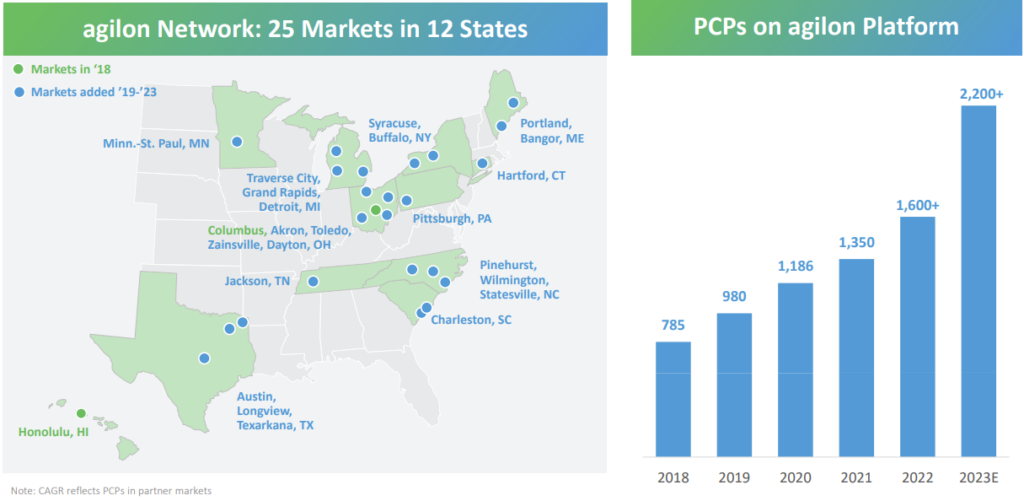

agilon partnered with Central Kentucky’s largest multispecialty physician group Lexington Clinic. Over the coming years, agilon will help support LC’s transition to value-based care programs through a huge footprint that includes 25 locations, 600,000 annual patients, 200 providers, 30 specialties, and 60 primary care providers, specifically. This seems like a huge win for agilon, which can now leverage this partnership to expand to other practices throughout Kentucky in its ‘hub and spoke’ physician acquisition model. The affiliation brings agilon up to 23 physician groups across 12 states and 2,200 primary care physicians. (Link)

Humana and ChenMed announced their 5-year agreement on the same day that the CVS-Oak Street Health news dropped. We love the mind games here. Humana and MA-focused primary care provider ChenMed have had a longstanding relationship and hold a joint venture, JenCare – which was rumored to be exploring a sale for $4B as recently as August 2022. The JV operates in 5 states and cares for about 50,000 patients. JenCare also recently appointed former Co-CEO and UnitedHealthcare exec Steve Nelson as its new CEO. ChenMed as a whole operates 120+ senior care centers in 15 states.

Join the thousands of healthcare professionals who read Hospitalogy

Subscribe to get expert analysis on healthcare M&A, strategy, finance, and markets.

No spam. Unsubscribe any time.

Providence is outsourcing 2,000 IT and admin jobs to a major tech hub in India as health systems look for ways to cut back on costs. (Beckers)

Cigna rebranded to The Cigna Group and aligned its corporate structure under 2 brands – Cigna Healthcare and Evernorth Health Services. Aha! Vertical integration! (Cigna)

Labcorp spun off its independent clinical trials business and renamed it Fortrea. (Link)

Henry Ford Health System has rehired 25% of the nurses who left during the pandemic. (Beckers)

Finance and M&A Updates:

The healthcare sector tops Morningstar’s distressed bond and loan index leaderboards, most of which are related to pharmaceutical companies in distressed, with facilities and services also contributing. (Pitchbook)

- The health facilities sector on Jan. 25 had 20% of its bonds (17% by dollar-price) trading at distressed prices. Public companies within the subsector, such as Community Health Systems Inc. and Cano Health LLC, cited higher salaries as well as inflationary cost increases and other charges for lower third-quarter margins.

- The same is true for the health services sector. S&P Global Ratings comments that some of the private health services issuers have encountered inflation-driven increases in staffing and other costs. For example, Heartland Dental LLC was facing higher costs for staffing such as hygienists, while Radiology Partners Holdings LLC was facing “rising wage costs because of the tight labor market,” according to a recent S&P Global Ratings report.

Kaiser Permanente posted an operating loss of $1.27B for full-year 2022. Will update with more detail once the full audit comes out. (Kaiser)

Tenet posted consolidated revenues of $19.2B and adjusted EBITDA of $3.47B, in-line with expectations. (Tenet)

Tower Health and Penn Medicine canceled their plans to merge on February 10. (Beckers)

Oscar’s full year earnings seem to have blown investor expectations out of the water (Oscar)

Centene Q4 and full year 2022 earnings included expectations of losing 2.2 million Medicaid members post public health emergency. It has also agreed to pay a total of $805.6M so far – while it has $1.2B reserved – in PBM settlements (HCD)

Digital Health and Startup Updates:

The firsthand team raised $28M. Instead of linking to that press release, check out some of their job openings here.

Clinical trials platform Medable was selected by the Nova Scotia Health Innovation Hub to improve patient access and clinical trials diversity across Canada. (Link)

OCD-focused NOCD raised $34M. (BHB)

Included Health partnered with Solv to help facilitate Included’s longitudinal, integrated care delivery platform. (Link)

BCBS of California added diabetes care company Virta Health to its statewide provider network for 2023. (MedCity)

GE HealthCare acquired AI-enabled ultrasound player Caption Health. (Link)

Doximity rolled out a beta version of its ChatGPT tool for docs – DoctGPT.com, which will integrate with Doximity’s fax service. Potential uses include using the generative AI platform for healthcare-specific medical prompts, prior authorization drafts, and more. Of course this opens up a whole can of worms if docs start doing the bare minimum for documentation. (Fierce)

Evvy, a femtech startup, launched a new research tool focused on specialized areas of women’s health. (Fierce)

Policy and Payment Updates:

In a win for freedom and competition, the state of South Carolina repealed its Certificate of Need program. (WLTX)

In a recurring theme for the state, North Carolina is once again weighing doing the same as South Carolina and repealing its CON program while expanding Medicaid. (TNO)

Biden said a few interesting things during his State of the Union address:

- The end of Covid

- Desire to cap insulin costs at $35/mo and address overdoses from opioids and fentanyl, continuing the Cancer Moonshot initiative

- Drawing a strong stance on abortion

- Protecting Medicare and Social Security at all costs

HHS has paused arbitration in surprise billing payment disputes after a Texas court decision vacated parts of the No Surprises Act. (HCD)

Costs, Data, and Other Updates:

An interesting piece from NPR covers a dynamic slowly unfolding in healthcare: more mid-level providers are staffing critical parts of the healthcare system (AKA, CRNAs or nurse anesthetists instead of anesthesiologists; employing nurse practitioners instead of physicians in the ER). As full practice authority increases in prevalence throughout the US, so does physician animosity toward the trend. Very noteworthy and likely worth a deep dive. (NPR) and a good overview here from Axios on the bigger issues at hand.

The Warped Incentives Behind Amgen’s Humira Biosimilar Pricing–And What We Can Learn from Semglee and Repatha (DrugChannels)

The healthcare industry added 58,200 jobs in January, with ambulatory healthcare services seeing the highest job gains, according to data from the Bureau of Labor Statistics. (Advisory)

Whitepapers and Resources

The BDO 2023 Healthcare CFO Outlook Survey had some interesting commentary from CFOs. (BDO)

The AHA released its 2022 National Healthcare Governance Survey Report with some summary insights linked here. (AHA)

Workforce challenges ranked No. 1 on the list of hospital CEOs’ top concerns in 2022, according to the American College of Healthcare Executives’ annual survey of top issues confronting hospitals. (ACHE)

The Brookings Institute posted an essay on nurse licensure compacts and how these have changed over the past few years. (Brookings)

Hospitalogy Top Reads

Betty Chang wrote a nice overview of common pitfalls facing digital health startups and her thoughts on how to overcome those challenges. Easier said than done! (Link)

A nice dissertation from Liz Kirk on how payment models are financially incentivizing value-based care, which is pushing the movement forward. (HCD)

That’s it for this week! Join 18,000+ executives and investors from leading healthcare organizations including Privia, ApolloMed, and HCA Healthcare, health systems including Providence, Ascension, and Atrium, as well as leading digital health firms like Cityblock, Oak Street Health, and Turquoise Health by subscribing here!