Happy Thursday, Hospitalogists!

Today’s post is all about Oscar Health and its ascent out of the abyss. Why am I posting an upbeat essay on an insurtech in 2024? I’ll tell you why, and then you can tell me what you think.

By the way, don’t forget to register for my upcoming virtual event chatting about everything behavioral health and managing risk here: Register Here!

Thanks so much to Turquoise Health and NeuroFlow for sponsoring today’s send. Big fan of both organizations as you guys know!

Welcome to Hospitalogy, a newsletter breaking down healthcare finance, M&A, and strategy twice weekly. Join 26,700+ executives and investors from leading healthcare organizations including HCA, Optum, and Tenet, nonprofit health systems including Providence, Ascension, and Atrium, as well as leading digital health firms like Oscar, Oak Street Health, and Aledade by subscribing here!

SPONSORED BY TURQUOISE HEALTH

Fresh off their Series B milestone, Turquoise Health is revolutionizing price transparency. Amid intense contract negotiations, rate negotiation and contracting is top of mind for everyone.

Turquoise Health wants to make price transparency and contract management simple for everyone.

By introducing AI-enabled tools like Ask TQ into its end-to-end Clear Contracts platform, Turquoise makes it easy to glean key insights on rates, quickly find answers within hundreds of thousands of pages of reference documentation, and manage your contracts all in one tidy location.

Oscar the Pirate Ship

“I sort of see Oscar as a pirate ship with cannons, amidst Spanish galleons filled with gold. They’re called big insurance companies.” – Mark Bertolini, CEO Oscar Health

(I didn’t think I’d be doing pirate ship research for a newsletter but here we are)

Last year I wrote a couple articles around insurtech dynamics – first noting a challenging environment for insurtech players post-ZIRP environment, and then diving into the Oscar hero’s journey: trying to redefine what health insurance is, the challenges it faced in entering that arena, and ultimately a fall from grace.

Despite it all – the cynicism, the noise, the ‘I told you so’ skeptics – Oscar Health is clawing its way out of the abyss. The firm is reinventing itself with Mark Bertolini at the helm of the ship, so let’s dive into why they’re set up for success in 2024.

Oscar the Plunderer

Like a small pirate ship, Oscar is nimble today. They’ve exited bad markets, narrowed focus to core competencies, and shed off the fat from the past ‘growth at all costs’ mindset. In 2024, Oscar’s singular, most distinct advantage lies in its ability to outmaneuver larger, slower players with more sophisticated, specialized weaponry for the task at hand: plundering the incumbents.

What’s the specialized weaponry? What it always has been for Oscar: consumer experience, a tech forward approach, and a great culture which attracts talented people. The only difference between past Oscar and today’s Oscar simply lies in the fact that the timing is right for them to start taking advantage of these differentiators financially through 3 big tailwinds.

To that end, Oscar’s 3 main pillars of ‘plundering’ – AKA, sustained success – include:

Join the thousands of healthcare professionals who read Hospitalogy

Subscribe to get expert analysis on healthcare M&A, strategy, finance, and markets.

No spam. Unsubscribe any time.

- Marketplace growth;

- Consumerization of health insurance through vehicles like ICHRA; and

- Selling its tech, +Oscar, to other healthcare organizations.

1. Marketplace Growth:

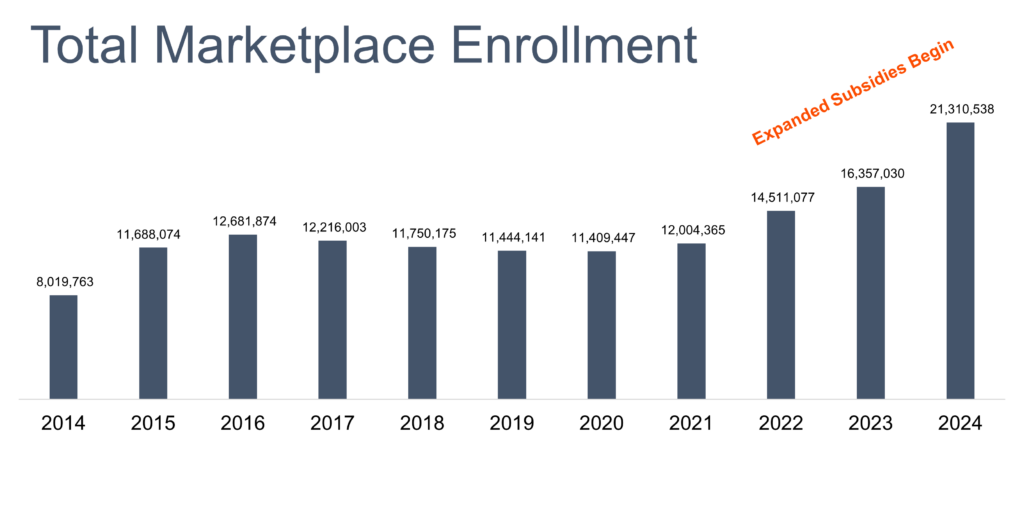

In 2024, 21.3 million people are on Marketplace plans – unprecedented, record-breaking growth. And Oscar’s membership growth in the Marketplace. We’re seeing historic growth in the Marketplace, mostly from Medicaid redeterminations. On top of redeterminations, an increasing number of smaller employers, contractors, and gig workers are choosing the individual market. Oscar holds 1.3M of those members, or around 6%, expanding to 165 additional counties in 20 states in 2024.

With sustained success in Florida, Georgia, and Ohio while outperforming in Cincy, West Tennessee, Topeka, and Iowa markets, Oscar is demonstrating an ability to launch and succeed in markets outside of major metropolitan areas.

2. Consumerization trends present a sustainable growth vehicle:

In an environment with never ending, egregious increases in health benefits costs, Employer market disruption is slowly taking form through vehicles like defined health benefit contributions (ICHRA) among small to medium employers. Someday more employers will realize taking health benefits cost containment more seriously will present an extreme competitive advantage for their organizations, freeing up significant tied up dollars to do other actually strategically important things. Oscar is positioned really well among consumers to take advantage of movement in consumerization. Its NPS is 60, significantly above its peers. That consumer focus also presents a cost savings opportunity – Oscar tested paying brokers lower commissions in certain markets to see if existing members would stay on their plan, and they did:

- “…we’ve tested NPS in a couple of ways. Last year…we priced by lowering some of the broker commissions. We’re holding them while other people were raising them, and we didn’t lose members. They stayed. They wanted to be with us.”

3. +Oscar’s Rise from the Ashes:

The final strategic growth pillar for Oscar lies in its ability to commercialize its internally engineered tech stack for other healthcare organizations to leverage. It’s a huge potential whitespace for Oscar, and one that it doesn’t have the best track record in to-date.

It’s probably not new to anyone reading this newsletter that Oscar’s initial tech platform rollout hit major speedbumps and led to some headaches for its first customers, like HealthFirst (+Oscar at the time was rumored to struggle to perform core functions like claims processing).

Back in January 2022, Packy McCormick wrote a (albeit sponsored) deep dive on Oscar laying out some bets on the technology side for the company:

- Bet #1: Technology can meaningfully improve member engagement, which leads to a better insurance business.

- Bet #2: A better, tech-powered insurance business will help Oscar sell its technology to hospital systems who want to take risk, improving margins and increasing revenue without increasing Oscar’s risk.

- Bet #3: Turning its tech into a platform for third-parties will build scale into both the insurance and tech businesses, which will help improve care and lower costs.

Will tech actually make a difference? Is this time different? With AI, can you finally translate better tech, and a more engaged, satisfied member into higher margins for an insurance co?

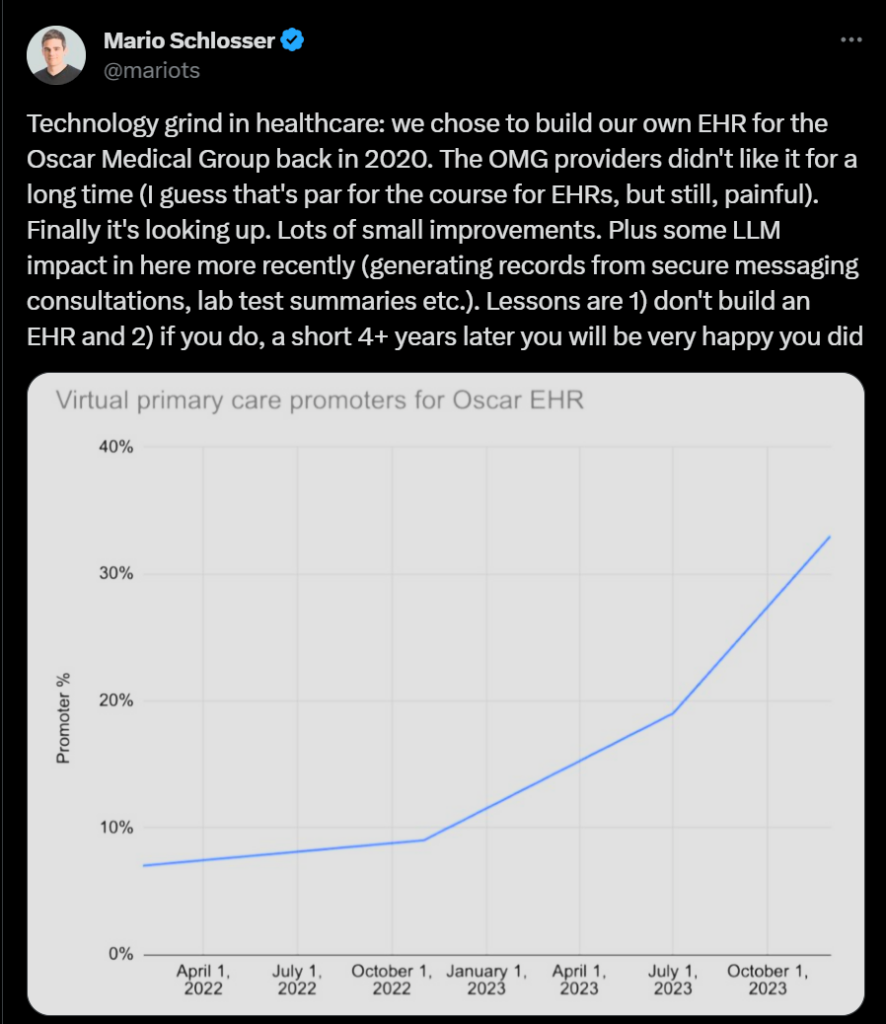

I think so, and so does Oscar. Not only do Mario Schlosser and team consistently post the crazy, over-my-head stuff they’re working on with LLMs internally at Oscar (and do continuous hackathons), even Mark Bertolini is on board with AI initiatives. On its Q4 earnings call yesterday, Bertolini mentioned Oscar had saved 200 employees’ worth of call center time, while boosting satisfaction rates, through using AI. Along with call centers, Oscar has noted a number of initiatives over the past year or so which sets itself up for competitive advantages:

- Total cost of care measures including diabetes and other chronic disease programs, and an enhanced Spanish-first experience

- Campaign builder integrated into client workflows

- Secure AI messaging platform and self-serving features freeing up team members to serve more complex patient needs

- Decrease in call abandonment rates

& plenty of other stuff that Mario & team outline on a consistent basis.

These types of initiatives are what will give Oscar leverage on variable operating expenses, lend credibility in sales calls with organizations looking for the tech, and will ultimately drive value for Oscar enterprise-wide. And if Oscar can pass along those savings to health systems through various point solutions or pain points over time via +Oscar, it’s a win-win.

- “And ultimately, we will get into the Medicare Advantage business, but that’s a few years out using our +Oscar platform with health systems in the market by enabling them to provide private label opportunities in their local markets to their patients versus having to sell through brokers to the market.”

Oscar’s new Captain: Mark Bertolini

The Bertolini Breakthrough: Looking back, assuming Oscar continues its trajectory, we might consider the hiring of Mark Bertolini as one of the greatest strategic moves in health tech history. Coming from Aetna, Bertolini knows how to run a health insurance shop. And he cleaned up Oscar’s book from day 1 less than a year ago (e.g., PBM savings). Oscar had plenty of low hanging fruit to cut, and they’re finally starting to do the blocking and tackling needed to function like a profitable health insurance company.

Here’s one of the most important features of bringing on Bertolini, though, which tends to be overlooked – his compensation package is tied to getting internal Oscar employees paid as well as getting Oscar’s share price back to its IPO price. You have to think this structure creates pretty nice goodwill within Oscar and its employees internally. And it’s a far cry from Bright, where executives were paying themselves up the wazoo for burning a company to the ground.

- “And so we put together the comp structure, which I and Josh and Mario talked about was I don’t get paid until the internal people get paid. So my gets are above their strike prices. And then there’s a little bonus at the top if we get back to IPO. And I thought it’s a good way to do it. I’m getting less salary than I have in probably 20 years, but that doesn’t matter. It really is the opportunity to sort of pay it forward and create a whole new way of attacking, what is an intractable problem in the United States, our health care system.” – Mark Bertolini, May 10 2023 Bank of America Global Healthcare Conference

Oscar’s …Booty: P R O F I T A B I L I T Y

(I know, at this point the whole pirate ship metaphor is cringe. I can’t help myself)

Bertolini laid out 3 financial goals for Oscar:

- Getting the insurance company segment to breakeven (done)

- Achieving Oscar enterprise-wide breakeven (expected in 2024), and

- Commercializing +Oscar in a robust way.

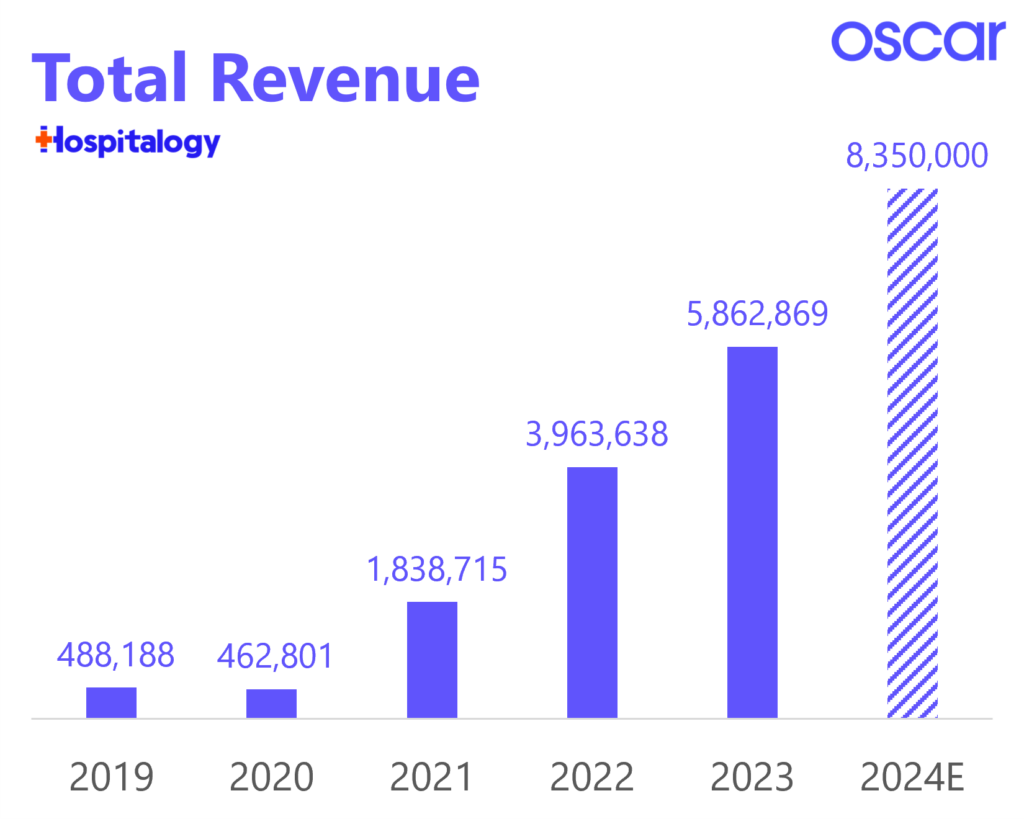

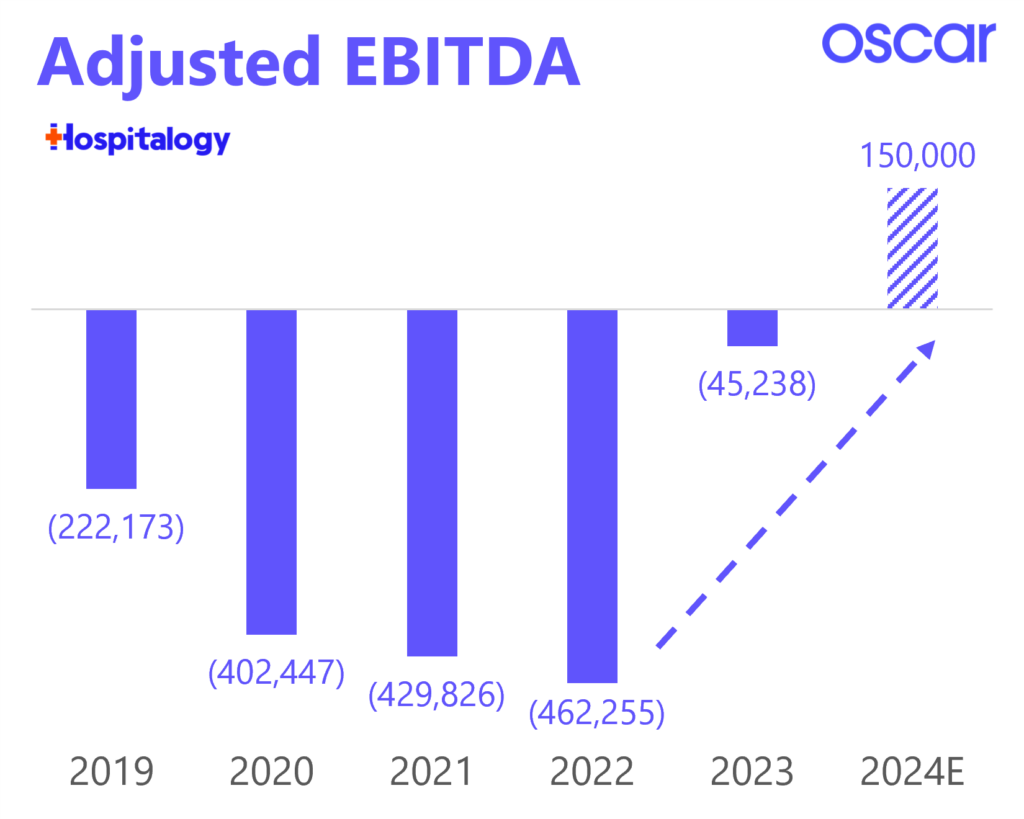

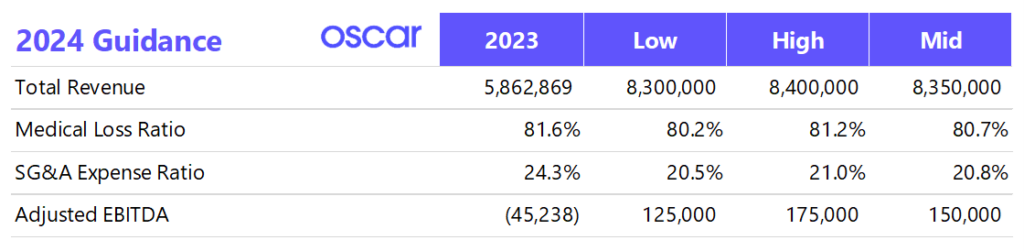

None of this means anything if Oscar can’t turn its 2024 tailwinds into financial results. And Oscar is doing just that, expecting adjusted EBITDA profitability in 2024. Profits!! As an insurtech!

Look at this rise from the abyss (like, literally) for Oscar:

Adding to this, Oscar is actually going to start reporting financials and operations like its health insurance company peers, which is probably the biggest signal that Oscar is ready to accept that they are, in fact, an insurance company:

Interest rates bolster Oscar’s cash flow: Here’s a really important dynamic positively affecting Oscar. With interest rates over 5%, Oscar (and other health insurers, of course) can reinvest its reserves to generate higher than normal investment income. For a company trying to grow and flip to profitability in 2024, this interest rate environment is a low key fantastic backdrop for Oscar and a material reason why it’ll achieve positive adjusted EBITDA this year.

- “So Josh, I think that the importance of the adjusted EBITDA metric for total company is that, that would — with the growth, we’ll be getting additional cash prior to paying the risk transfer estimate. So we would anticipate that the total company will be cash flow positive. We’ll be building capital in our insurance subsidiaries.”

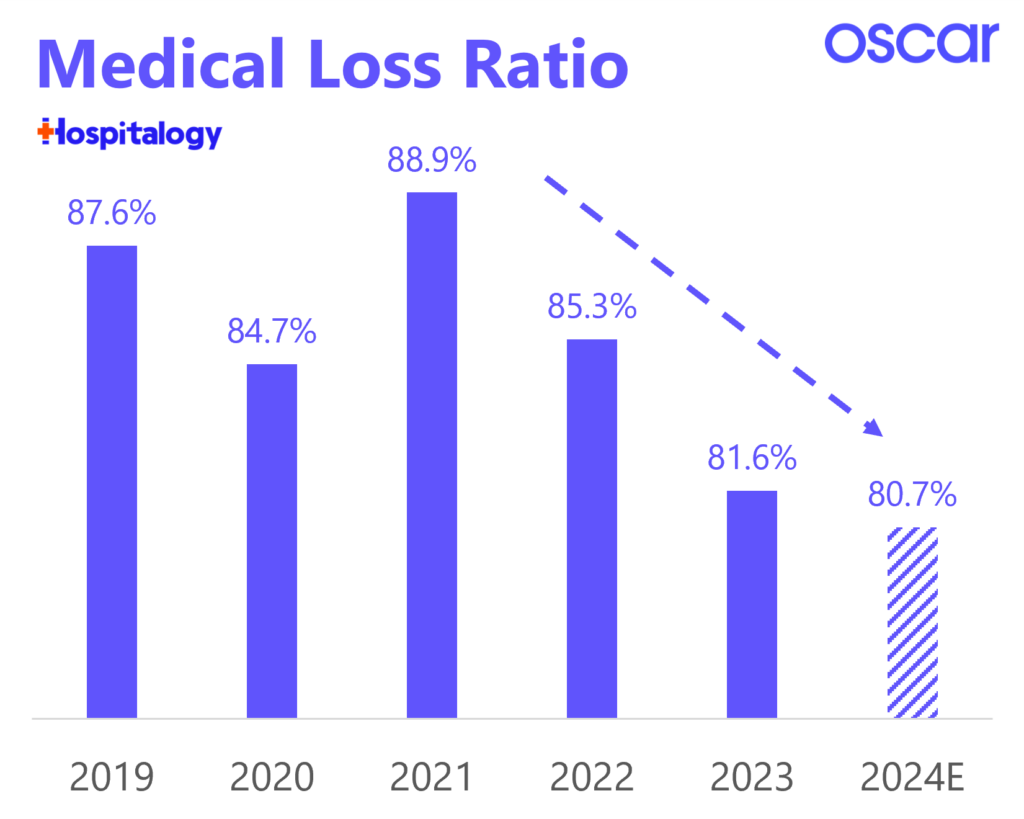

Oscar noted an ability to drive total cost of care down further, with more levers to pull in its MLR. They specifically called out provider and hospital contract negotiations on both terms and rates bases. The firm has a prioritized list based on renewal dates and market size where they’ll begin conversations and forge better relationships with them on utilization management. Adding to this, with increasing scale, Oscar can finally start to gain leverage on its fixed cost structure and overall operating costs given its return to growth assuming its AI cost savings thesis plays out.

All in all Oscar expects to grow at a 20% clip for the foreseeable future. I’d expect that estimate to be on the conservative side given Bertolini’s prior commentary around conservatism in quarterly results.

Oscar’s Bilgewater

On a pirate ship, the ship’s bilge is the lowest part inside the ship, within the hull itself which is the first place to show signs of leakage. The bilge is often dank and musty, and considered the most filthy, dead space of a ship.

Where might we start to see leakage in Oscar’s business?

- The low-hanging fruit is gone: Bertolini and co have corrected for all of the normal things a health insurer should have been doing all along (e.g., quarterly pharmacy contracts). From this point forward, growth and expense management for Oscar requires legitimate execution – continuing to drive automation forward with AI, growing in the Marketplace, and regaining trust in the +Oscar platform.

- Declining political support for the ACA: From an existential perspective, the threat of dropped subsidies or a ‘Repeal and Replace’ healthcare law facilitated by Republicans exists, but is unlikely. Most of the growth in Marketplace plans come from red states. The Marketplace, now at 21M+ members, has reached critical mass. Subsidies ending in 2025 and affordability thereafter if left undone are the bigger issue.

- “…in this open enrollment, 63% of new ACA consumers are from red states and 76% during the open enrollment and year-over-year in the ACA, our market growth is in red states. So I kind of find it hard that the political dynamic that was going on 6, 8 years ago is going to be the same relative to the Republican party going after a group of people that largely are going to be their own constituents.”

- “Folks in the group we worry about most are the people in the 100% to 200% federal poverty level that have 0 premium plans and would potentially be paying somewhere around $60 or $70 a month. That’s the place where we think the impact is.”

- ICHRA and small-medium employer market disruption fizzles out: I actually think that defined health benefit contributions like we’re starting to see in ICHRA presents one of the biggest long-term growth opportunities for Oscar. If ICHRA fizzles out or if these employers choose a different mechanism for health benefits savings, the window of opportunity would of course slam shut.

- They’re still a blip on the radar: Despite $8B+ in revenue projected for 2024, Oscar is a rounding error compared to other large managed care players and will have to continue to capture market share while maintaining prudent pricing discipline. Adding to this, Oscar mainly attracts young, healthy members meaning the insurtech is a chronic net-payor in the Marketplace’s risk adjustment transfer zero-sum game.

Everything is still in front of Oscar

“We have done what we said we would do. Oscar is delivering on its commitments.” – Mark Bertolini

Ultimately, I want Oscar – and other consumer-oriented healthcare companies – to succeed in healthcare. In 2024, Oscar looks like it’s ready to do just that. But I’m curious for your thoughts on Oscar given what I’ve laid out. Feel free to respond to this email with your thoughts!

Resources:

- Oscar’s Q4 2023 earnings release

- Oscar’s JP Morgan presentation

- The Oscar Puzzle

- The Oscar Odyssey

SPONSORED BY NEUROFLOW

For risk-bearing organizations, it’s critical to recognize that behavioral health acuity is rising across your populations, and unfortunately, there’s no sign of this slowing down.

Data has shown individuals with chronic diseases coupled with behavioral health conditions drive 2-6x higher healthcare costs. You need a cohesive strategy around this population.

On 2/15, join me, the NeuroFlow team, and a panel of experts in a virtual event.

We’ll have a much-needed conversation around how health systems, payors, and risk-bearing orgs can proactively measure and address the behavioral health of their complex patient populations. Register Today!

If you enjoyed this, consider subscribing to Hospitalogy, my newsletter breaking down the finance, strategy, innovation, and M&A of healthcare. Join 26,000+ healthcare executives and professionals from leading organizations who read Hospitalogy! (Subscribe Here)