TL;DR: UnitedHealth Group’s worst quarter…ever? The highlights:

- UnitedHealth Group cut its 2025 guidance and profitability significantly, with a two-pronged whammy playing out in 2025 within senior populations and Medicare Advantage.

- OptumHealth faces significant cost and revenue pressure stemming from struggles to adjust to the new v28 risk model (year 2 of the 3-year phase-in) along with onboarding unprofitable, unengaged members acquired from other MA carriers who exited OptumHealth markets and were naturally picked up by Optum.

- Elevated utilization mostly in group MA caught UnitedHealthcare off guard. Higher premiums ironically led members to seek out preventive care, leading to downstream specialty and inpatient care.

- The updates call into question UnitedHealth Group’s strategy around capitation and value-based care, and the dynamics at play may have uniquely impacted UHG versus its peers (Humana, CVS)

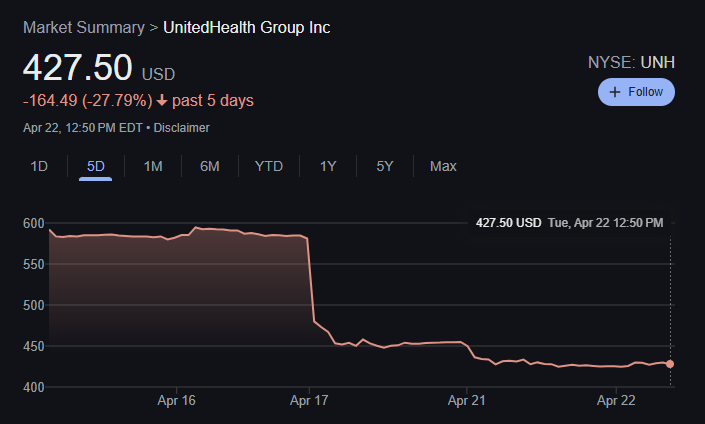

- UNH management seemed a bit dodgy tone-wise on the call. First time in what feels like forever they’ve missed earnings. Maybe a decade-plus. And they had to re-explain their entire thesis behind transitioning Optum members to VBC. Since earnings, UnitedHealth Group experienced a $150B+ drop in market cap, a move larger than all of the public hospital operators combined.

Going Deeper: UnitedHealth Group earnings analysis

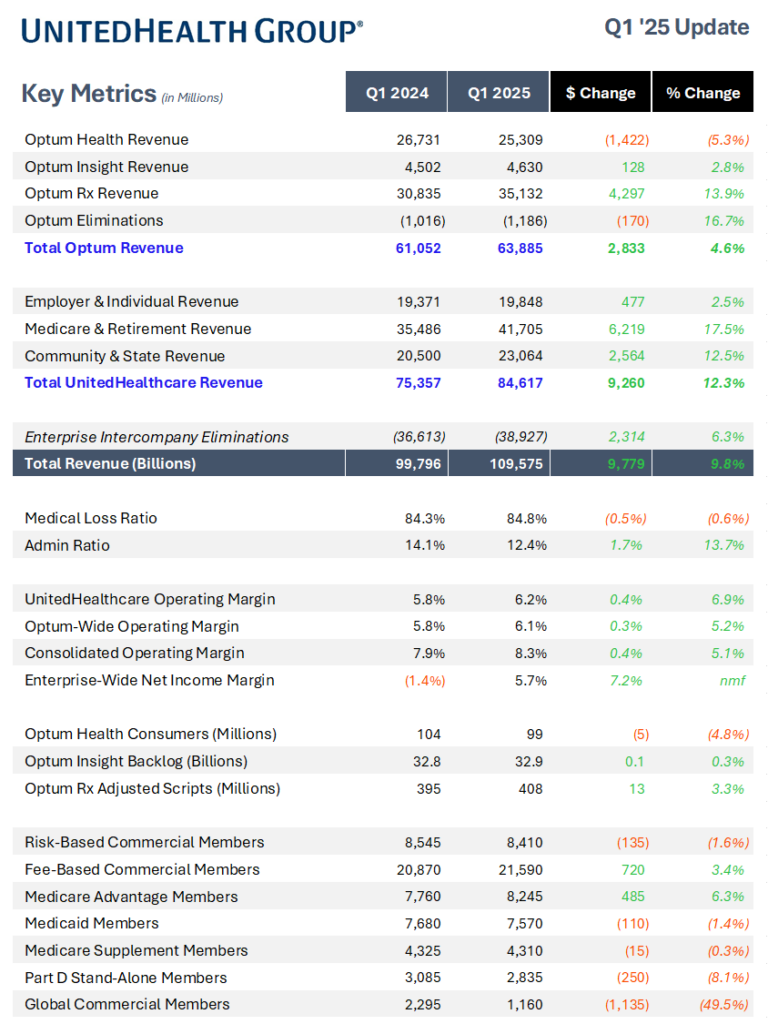

OptumHealth Woes Drive Underperformance: The big miss was in Optum, and OptumHealth specifically (the segment housing all of the physicians and clinicians). OptumHealth membership added more full risk membership than expected, and because utilization spiked (notably calling out outpatient care and OP behavioral health), coupled with v28 transition challenges (less revenue from coding), Optum faced significant medical cost pressure from this new cohort. UHG also mentioned these member profiles were not specific to any one market or carrier.

So the dynamic played out something like this:

CVS, Humana, and other MA players exited certain unprofitable markets given 2024 MA headwinds → by staying in those markets and gaining market share by subtraction, and being a large, payor agnostic player, OptumHealth picks up these ‘discarded’ members → This segment of members is expensive, unengaged, and therefore, unprofitable → this problem compounds with v28 risk adjustment challenges → Optum makes significantly less profit.

- Our patient profile post AEP included many new to Medicare as well as new to OptumHealth who are meaningfully less engaged by their prior health plans and providers. We believe that market specific plan exits driven by v28 caused this dynamic.

- [New Medicare patients] experienced a surprising lack of engagement last year, which led to 2025 reimbursement levels well below what we would expect and likely not reflective of their actual health status.

- Engagement remains the key

There’s writing on the wall here that’s just a hunch for me, but is probably directionally correct: Optum just bought a crap ton of physicians and didn’t fully integrate them, so now maybe they’re a bit blindsided by current utilization and MA dynamics, and existing levers UHG has to pull in its operating model aren’t cutting it. So they need to prioritize engagement heavily at the clinic level.

- Fourth, to more effectively transition to the new CMS risk model, we’re investing significantly in improving physician clinical workflow to help ensure better care and timely insights on when and where care is most efficient and effective.

- …First, enhancing access for employed and network PCPs especially around new patients to diagnose document and treat conditions. We’re expanding home-based visits and wraparound services, particularly as it relates to post-discharge visits after in patient care. And…we’ve accelerated EMR unification, deploying smarter clinical workflows and point-of-care tools to better adapt to the V28 related changes.

On the insurance side, Medicare Advantage (note: not commercial or Medicaid) utilization doubled what UHG expected in physician, outpatient, and to a lesser extent, inpatient services:

- In UnitedHealthcare’s Medicare Advantage business, we had planned for 2025 care activity to increase at a rate consistent with the utilization trend we saw in 2024. Instead, though, first quarter 2025 indications suggest care activity increased at twice that rate.

In the Q&A, Josh Raskin asked a great question: “in this environment, why are you allocating so much capital to transitioning patients to value-based care, full-risk arrangements if this quarter is the result? Aren’t you exposed to elevated utilization trends like these moving forward? Is this strategy still sustainable long-term?”

UHG executives noted that the problem didn’t lie in patients seeking out their PCP – generally, patients are seeking out more preventive care. But the ‘problem’ lies in that once they see their PCP, they then are receiving follow-up care, and the extent to which that occurred is what UHG didn’t foresee. UHG management responded by highlighting Optum’s differentiated approach and reiterating that engagement is key, but also dropping the following quote around major cuts the MA space has seen over the Biden Admin:

- So what we’re seeing here is not really a challenge to the underlying principle of value-based care. What we’re seeing is how to adjust to a very dramatic price cutting regime that’s been implemented over the last couple of years by the administration. And it’s important to recognize that, that was across the average of the industry, independent analysis would say that was about a 9% price cut across the industry. Now that’s a significant downdraft in terms of pressure, and obviously, that affects participants, whether you’re a payer or a provider in the marketplace.

- What we’re going through like the rest of the industry, is a dramatic, really never seen before adjustment in pricing for this marketplace. And what we’re seeing this year is two or three areas where the pressure that, that has created across the market is creating new dynamics we haven’t seen. That’s exactly what we’re responding to here, and we believe that they are largely addressable as we go through the rest of this year, and in no way undermine our confidence in the value-based care strategy of the company.

OptumRx Notes:

Strength in OptumRx and biosimilar pipeline; removal of prior auth for 80 drugs accounting for 10% of OptumRx prior auth’s in general.

- Lastly, OptumRx revenues grew 14%, exceeding 35,000,000,000 for the quarter. Both customer retention and new customer wins contributed to script growth of 3%.

- On the new Arkansas law, UHG management mentioned the new legislation would impact patient access and integrated care delivery. So they’re obviously not fans.

- …one of the things that has been honestly most disappointing over the last year or 2 is obsession with the role of the PBM versus everybody else in the system. And if you read the EO carefully, what you’ll see in there are quite good, sensible questions to explore what’s going on either side of PBM in terms of the manufacturers and also ultimately, many of the providers in the network. And I think what you’ll see from that is the PBM plays a unique role in trying to bring down drug prices for Americans.

Open-ended questions and thoughts:

Besides regulatory breakup or other policy-driven risks, this current dynamic is probably the biggest bear case for UnitedHealth Group as seen by the slide in stock price post-Q1 earnings. Over the past few years UHG has been preaching “value based care. Capitation.” This quarter opposed this thesis, as seen by Optum’s 10% revenue guidance cut and a marked shift back to fee for service. Whether this continues long-term remains to be seen, but UHG management didn’t seem to think so.

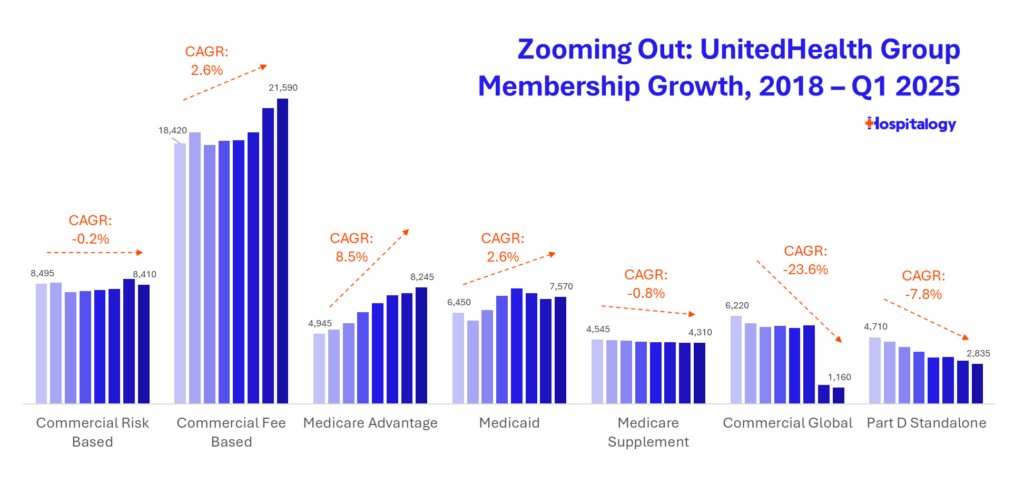

What will happen for Humana, CVS earnings later this week and next? Did they get ‘lucky’ by shedding members in 2025? A blessing in disguise? Investor eyes will be on these names next to understand the full picture.

What does it say about healthcare, and Medicare Advantage as a whole, that there is an entire segment who are unprofitable and unreachable (at least currently)? And how do we find something that’s sustainable for this population?

UnitedHealth Group continues to face scrutiny from media outlets like the Wall Street Journal and StatNews, getting heat for everything from aggressive risk adjustment analyses to algorithmic care denials investigations to member experience. They’re still the media’s favorite punching bag for woefully broken components of our healthcare industry.

Still, at the end of the day, you might as well still buy UnitedHealth Group, because they’re not going anywhere. (Not investment advice, of course). Operating in healthcare involves the long game:

Additional Reads & Resources:

- UnitedHealth group earnings release. (Link)

- UnitedHealth Group Q1 Earnings (Jeff DelVerne)

- Medicare Advantage costs ‘manageable’ for Elevance: 8 notes (Beckers)

- Bonus: Elevance key highlights from its report today. (Full slide deck here)

Join my Hospitalogy Membership! If you’re a VP or Director working in strategy or corporate development at a hospital, health system or provider organization, you will get a lot of value out of my community as I purpose-build the content, fireside chats, and conversations for this group. Join for free today.