Today we dive back into Privia’s recent performance, management commentary, and value-based care / physician employment implications. If you enjoy this, feel free to throw a few of these charts into your board deck. Free advertising for me!

Executive Summary on Privia’s Q1

- Bumped guidance given broad-based outperformance: Privia management increased full-year guidance given strong ambulatory utilization, operating leverage on its existing book of business, and rest of 2025 outlook.

- Strong fundamentals: Balance sheet remains a fortress at $469 million cash and no debt, giving Privia flexibility for disciplined M&A and tech investment.

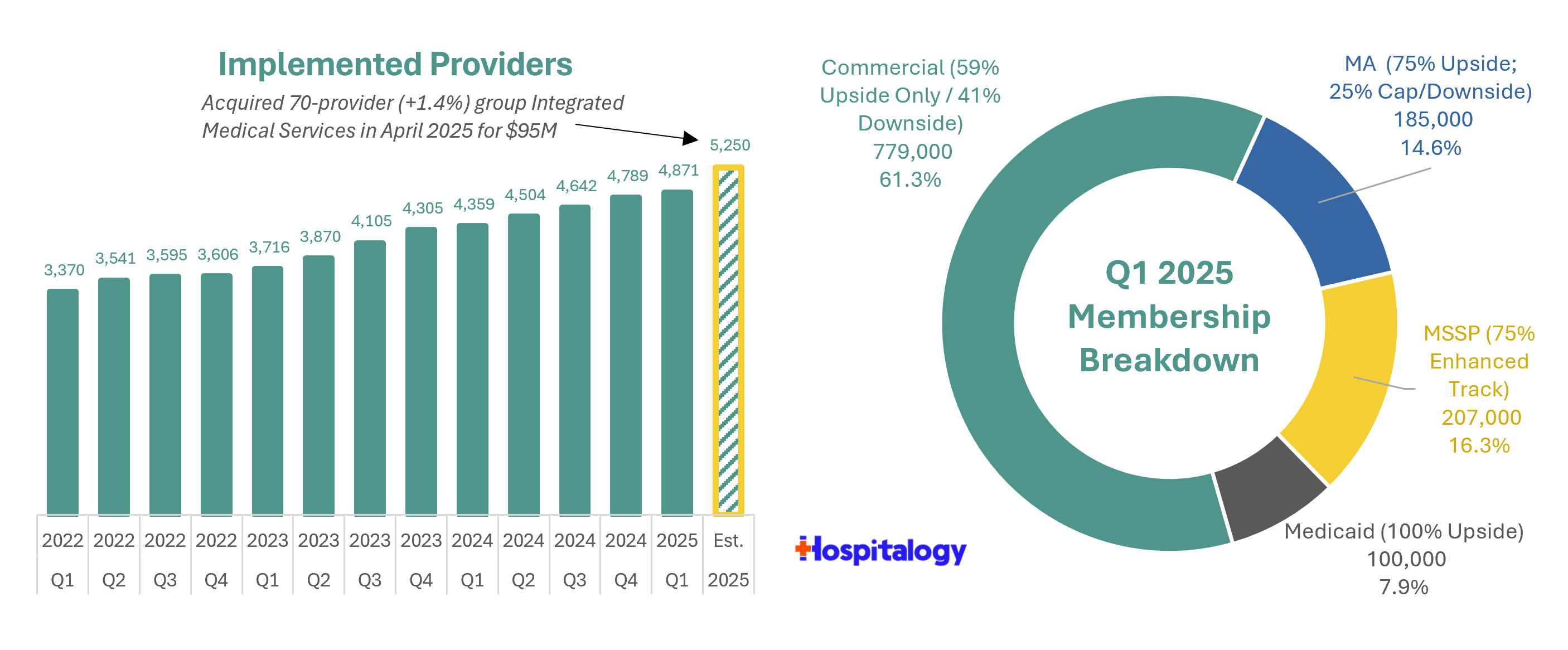

- Anchor practice = acquired in AZ: It looks like Privia picked up an excellent acquisition in Integrated Medical Services, which marks the enablement player’s entry into Arizona The $95 million acquisition adds 70-provider scale, 28,000 value-based lives (with existing participation in risk programs but no capitation), and is expected to be EBITDA positive by Q4, illustrating Privia’s “anchor practice” expansion strategy with further opportunities in both VBC and physician tuck-in’s from here.

- Model flexibility limits MA exposure, diversification of risk: Medicare Advantage risk exposure stays limited and shared-savings focused, though Privia picked up some capitated members through organic growth. Diversified VBC member mix (61 percent commercial, 31 percent Medicare, 8 percent Medicaid) and aversion from full capitation continues to benefit Privia versus its peers.

- AI and tech adoption; Navina is crushing: Broad rollout of Navina’s AI assistant (shout out to the Hospitalogy sponsor making waves!!) is improving documentation accuracy, closing care gaps, and reducing physician burden. Privia is also targeting areas like RCM, and VBC through clinical workflows, decision support, data aggregation and analytics, and payor contracting.

- Privia’s outperformance leads to better M&A opportunities: Competitive positioning strengthened further as risk-heavy peers struggle (even Optum!!); Privia’s cash, profitability, and physician-friendly model make it a potential landing spot for groups reconsidering past partnerships especially given its focus on clinical autonomy – a compelling talking point for many physicians looking for an alternative to hospital-based employment.

Privia Health is a good business.

They’re quietly (but with a steadily intensifying drum beat) becoming a formidable scaled, nationwide physician enablement platform in an era when others either flew too close to the sun and stumbled, or took a step back amid major industry headwinds.

Privia’s Q1 2025 shows a company hitting its stride.

Growth is up, margins are up, and strategy is more than intact. And they continue to stay disciplined under CEO Parth Mehrotra’s helm – the characteristic I love most about Privia. They’re not swinging for home runs with risky bets. They’re hitting singles and doubles consistently (with the occasional strategic swing like the Arizona deal).

And so we see the steady compounding drum beat, quarter after quarter.

Spotlight on M&A in the physician practice management market in 2025

Privia’s differentiation in attracting a large, multispecialty physician group.

Any practice that size, as we’ve stated in previous calls, has been approached by everybody you can imagine, health systems, private equity, bigger payers, other consolidators, so on and so forth, other enablement companies. I think what was key to them partnering with us is, number one, we just have a unique model that can cater to the entirety of the practice. All specialties, every single patient, every single line of business, every payer, comprehensive tech services platform. And that, coupled with an ability to maintain clinical autonomy in a model like Privia where you’re not getting employed by another entity from your compensation perspective, you’re able to make the decisions in day-to-day working at the clinic and how you practice medicine. I think that was immensely important to the physician leadership there. They came out of a health system.

And so obviously, the group was — is fiercely independent and believes in autonomy of private practice which leads us to having a pretty strong cultural alignment. And I think we can have a great business in Arizona with their help and grow that business, grow their clinic as well as grow random. So I think it’s a combination of all of those. They did partner with other enablement companies, and I think we’ll just evaluate those contracts over time, but we fully own the medical group risk entity MSO entities. And so we’ll just evaluate how we move some of those contracts over time. And that, again, highlights the importance where even though some of these practices can partner with other entities once we come in with our comprehensive solution that overweighs any prior decision. So we’ll just see how those play out and what the contractual terms are and how they’re performing and data from there.

Privia’s competitive advantage in M&A

We’re seeing an interesting effect. Optum’s woes and stepping back from M&A provides a better opportunity for enablement players like Privia to step in to that strategic void, albeit at a much smaller scale. Meanwhile, other risk-bearing players who didn’t do their homework are also taking a step back, leaving better, profitable operators in a more favorable M&A environment

- And I think a lot of these companies entered into some contracts that didn’t validate that [capitation] thesis. And financially now, some of these contracts or structures might be impaired, just unsustainable from a payer enablement company perspective or unsustainable from the relationship that they have with the provider group that they signed in terms of economic sharing, overall opportunity to earn share savings, so on and so forth as all these impacts happen on the MA book from V28 and star scores utilization, so on and so forth. So I think all that should bode well for us. I think we’ll continue to see some disruption. We’ve said previously, we look to take advantage of that and get these groups in, hopefully, which is a model that is much more sustainable like ours, so organically and then also inorganically.

Rolling 12-month Profitability Metrics

Q1 Overview

Key Metrics

Here are some of the more pertinent metrics for Privia from the quarter:

Implemented Providers and Q1 Membership Breakdown

As the main driver of the Privia engine, Privia continues to pick up providers to its platform. This quarter was no different as Privia netted 500+ new providers over Q1 2024. Privia will tack on another 70 or so with its aforementioned acquisition of Integrated Medical Services in Arizona, a 1.4% M&A bump to edge closer toward the 5,000 to 5,500 implemented provider guidance number Privia management set out at the beginning of 2025.

Join the thousands of healthcare professionals who read Hospitalogy

Subscribe to get expert analysis on healthcare M&A, strategy, finance, and markets.

No spam. Unsubscribe any time.

Revenue Breakdown

VBC revenue saw a sharp increase on the back of a 37.8% increase in capitated revenue for the quarter (more on this in a sec). FFS revenues continue their steady upward march. Over the past 3 years, Privia’s value-based care and fee-for-service based revenue streams have increased 16.3% and 14.8% compounded annually, respectively.

Growth Analysis

Privia saw impressive 11.1% member growth across all of its segments leading to 15.6% topline growth, including strong upticks in care management fees and organic member capture in new capitated lives. On the expense side, Privia saw significant leverage on G&A costs. Provider expense notably outpaced overall revenue growth in the quarter.

Privia blew profitability out of the water in Q1 with adjusted EBITDA growing a whopping 35% year over year. All profitability metrics saw material margin expansion given the strong broad-based outperformance on Privia’s book.

2025 Guidance Updates and Outlook

As mentioned, Privia upped its guidance noting the favorable outlook for the rest of the year, with the biggest lever here being its value-based care book of business. Since utilization is high, Privia collects higher dollars on the FFS book of business.

My Take

Privia’s Q1 looked almost boring, and that is a compliment. While peers serve up plot twists, Privia keeps stacking quarters (or singles and doubles, depending on your preferred metaphor), adding providers, expanding margins, and hoarding cash. They’re proving that physician enablement can scale without blowing up the income statement or the balance sheet.

Arizona should be a nice proof point that the playbook travels. If they integrate IMS smoothly, expect Privia to rinse and repeat in another state or two next year. Meanwhile, competitors battered by MA risk, interest-rate reality, or the hospital physician employment model may start leaving physician groups on the curb. Privia, with fresh powder and a disciplined filter, could go shopping. Are we finally seeing the pendulum swing?

Privia continues to be the quiet compounder of physician enablement, and Q1 2025 only bolsters that thesis. If they keep threading the needle between growth and risk, I suspect the Street will keep rewarding them with a valuation premium.

Join my Hospitalogy Membership! If you’re a VP or Director working in strategy or corporate development at a hospital, health system or provider organization, you will get a lot of value out of my community as I purpose-build the content, fireside chats, and conversations for this group. Apply for free today.