Welcome to the latest Hospitalogy!

Today we’re taking a deep dive into the healthcare benefits space. I’m super excited to be partnering with First Dollar on this post, who provided me with some behind the scenes intel on what’s going on in the healthcare benefits space, their business model, the pain points they solve for their customers, and what’s next at the intersection of healthcare and fintech.

While this is a sponsored deep dive, I also hope it provides Hospitalogists with interesting tidbits on what’s going on in health benefits and major pain points that TPAs and health plans face daily. I personally thought it was fascinating and love exploring new and emerging spaces in healthcare.

Let’s get into how companies like First Dollar are changing the game!

As mentioned, this is a sponsored post, where I cover interesting healthcare and health tech companies making a difference and improving the future of healthcare – if you’re interested in diving deep with me on a sponsored post or learning more, e-mail me direct at [email protected]

Join 14,000+ executives and investors from leading healthcare organizations including HCA, Optum, and Tenet, nonprofit health systems including Providence, Ascension, and Atrium, as well as leading digital health firms like Tia, Carbon Health, and Aledade by subscribing here!

TL;DR: First Dollar and Health Benefits

The healthcare benefits space is fragmented and outdated, but also growing. First Dollar offers a software-as-a-service (SaaS) product (Health Wallet) to simplify healthcare benefit programs, partnering with third party administrators, health plans, and financial institutions to solve pain points in benefit administration and drive revenue for their partners via a more competitive benefits offering. First Dollar’s solution is easy to integrate via APIs, seamless to white label, and painless to manage on the back end. The team’s thoughtful product design results in higher usage among consumers and a competitive edge for First Dollar-powered solutions.

- To learn more about First Dollar, check out their website here.

First Dollar: Key Takeaways

The healthcare payments and benefits industry holds incredible, tax-advantaged financial vehicles. These vehicles include health savings accounts (HSAs), health reimbursement accounts (HRAs), and flexible spending accounts (FSAs). All help consumers with healthcare affordability. Demand for these benefits will keep growing as the trend towards the consumerization of healthcare persists.

In response to rising costs and a need to differentiate, supplemental benefits have become increasingly popular. Some examples of supplemental benefits in Medicare Advantage include directed spend programs that give members funds for designated expenses (e.g., OTC) and health rewards programs that reward members with funds when they perform a desired behavior. (AKA, “We’ll give you $25 for healthy groceries if you get your flu shot.”) These supplemental benefits are also becoming increasingly popular in the commercial insurance space as plans seek to differentiate & innovate with new risk-taking models. (e.g., using rewards to drive members across a preferred network of providers)

Like everything else in healthcare, the benefits and payments space is rampant with 1990s Internet Explorer-levels of fragmented offerings. If you have 4 vendors with 4 cards and 4 distinct portals (each with their own passwords – yikes), your benefits are going to be pretty hard to use. I can speak from experience: it took my old HSA account 90+ days to transfer to my new vendor. I can only imagine what Medicare Advantage beneficiaries go through.

Legacy product design frustrates both plan administrators (TPAs, health plans) and end consumers. Frustration and confusion leads to lost benefit dollars for consumers. It also leads to lost business for TPAs and health plans as they distribute these benefits in an increasingly competitive employer market.

First Dollar is fixing the problem of fragmentation and poor customer experience. They partner with plan administrators behind the scenes to offer an embeddable, integrated solution. This method empowers TPAs to own their data and control their own benefits platform. After launching with an HSA product in 2020, First Dollar now offers all consumer-directed and supplemental benefits for partners.

In a healthcare world where putting the consumer first doesn’t happen often, First Dollar is challenging that status quo. They made major design team investments to create thoughtful, Apple-level design to optimize consumer use. Along with clean interfaces, the First Dollar team prides itself on integrations with their health plan and customers, leading to easier control over benefits. Better UI + simple control = higher use of benefits and satisfaction.

Players who put forth competitive offerings with both plan administrators and the end user in mind are well positioned to succeed in the transforming world of payments and benefits, especially as payments grow more connected and easier for consumers to manage. Plan administrators who choose to stick with anti-consumer offerings will fall behind. The benefits + payments market is ripe for design and consumer innovation.

First Dollar is well positioned for a long growth runway in a large market with a clear value prop. Health plans and TPAs want a comprehensive suite of products and services, and First Dollar delivers that. Consumers are still learning about HSAs and benefits that can lower out of pocket costs. Adoption of these healthcare savings tools will increase.

First Dollar’s Beginnings

Colin Anawaty and Jason Bornhorst are no strangers to healthcare problems. The two founded Patient IO, a care coordination and patient engagement platform ultimately acquired by athenahealth back in 2016.

Join the thousands of healthcare professionals who read Hospitalogy

Subscribe to get expert analysis on healthcare M&A, strategy, finance, and markets.

No spam. Unsubscribe any time.

But while working at athena post-acquisition, the two couldn’t believe the obstacles that patients faced when paying for healthcare services and the lack of connection among financial products. After 3 years at the EHR, the two founders left with a new hunch: “Let’s make healthcare benefits a hell of a lot easier to use.”

So that’s how the founders pitched First Dollar: Design benefits so that people use them, and offer an all-in-one platform to manage health benefits.

To date, First Dollar has raised $19 million. In January it raised $14 million led by Blue Venture Fund, Next Coast Ventures, and Meridian Street Capital among notable angel investors.

Overview of the Health Benefits Market and Terms to Know

Before getting into how First Dollar solves pain points for health benefits admins, let’s dive into the key terms to know in the health benefits & payments space. There are two main segments here and a whole lot of acronym soup:

Consumer-directed benefits (CDBs): CDBs are primarily tax-advantaged benefits that employers offer. The following are healthcare-related CDBs in the space:

- Health Savings Account (HSA): A literal god-tier benefit, HSAs are a triple tax advantaged retirement account, meaning that you can contribute limited pre-tax dollars to an HSA account, spend that money guilt-and-penalty-free on qualified healthcare purchases (not premiums though), invest dollars tax-free, and the HSA gets expanded use once you hit 65. The only caveat is that in order to qualify for an HSA, you must have a high deductible health plan. Which really isn’t that hard these days am I right?

- Flexible Spending Account (FSA): Kind of like the HSA’s step cousin, an FSA is also a tax-advantaged healthcare account you can contribute limited pre-tax dollars to in order to cover healthcare costs. The only problem is that these funds are “use it or lose it” by the end of the year. Stressful if you don’t have someone like First Dollar watching your back.

- Health Reimbursement Arrangement (HRA): Fun fact: I used an HRA when my dumb self got hit in the face with a softball and I needed to have nose surgery. HRAs are set up by employers to allow their employees to cover medical expenses. So in the case of my bent-sideways nose, my deductible was $6,000 but I was only responsible for the first $1,500 til the employer HRA kicked in for me.

- Lifestyle spending account: These are after-tax funds that employers can offer for a variety of ‘lifestyle’ related things, including professional development, continuing education, fitness/gym, pet care, work from home costs, and more.

Supplemental benefits: Supplemental benefits in health plans include pharmacy benefits but also directed spend programs. Directed Spend programs are a way for health plans to give members funds for designated expenses. They have many different names or examples, like members getting Healthy Grocery cards that allow them to buy fresh produce, or members using separate cards for access to transportation to the doctor’s office. Some specific examples:

- Health rewards

- Over-the-counter drugs

- Prescription drug benefits

- Grocery stipends

Current State of the Health Benefits Market: Growing, but Disconnected

Like a lot of areas in healthcare and finance, the healthcare benefits and payments space is in a state of tech transformation. New entrants like First Dollar are offering consumer-focused, tech-enabled products, while incumbent providers cling to market share with legacy products. Right now, incumbents dominate the market. Two incumbent providers hold 50%+ market share in benefits administration, with one legacy firm working with over 50% of Fortune 1000 companies.

The health benefits market is in secular growth on both the consumer-directed market and the supplemental benefit side. HSAs, HRAs, and FSAs are growing like wildfire as a result of the prevalence of high-deductible health plans. Since HSAs and FSAs are pre-tax dollars, the financial vehicle can basically be used to pay for healthcare services at 30ish% off.

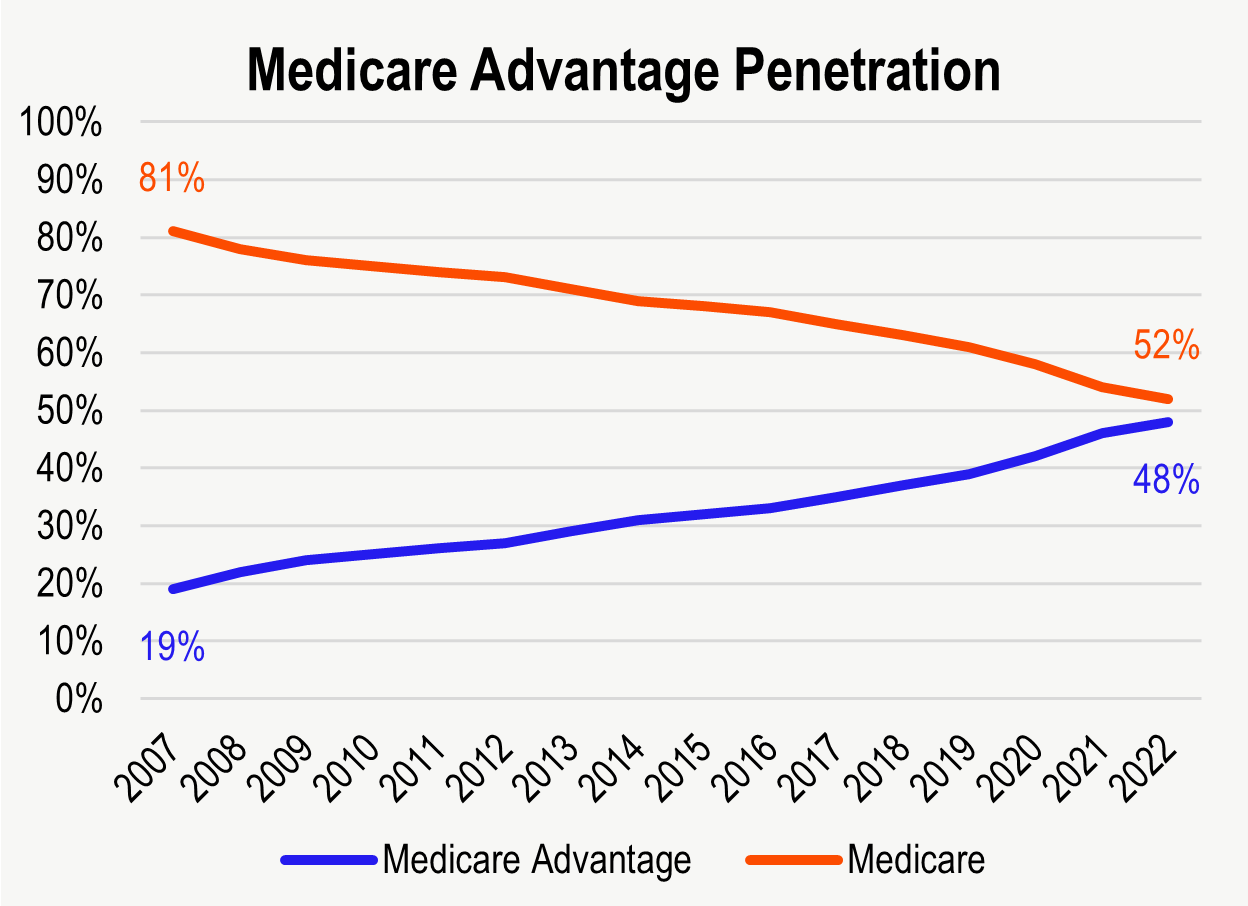

Likewise, I think we’re all familiar with how much growth Medicare Advantage has seen over the past decade. Medicare Advantage reached 48 million beneficiaries this year and will soon overtake traditional Medicare plans.

Yet at the same time, Medicare Advantage plans are becoming increasingly commoditized. As a result, the supplemental benefits that plans offer are growing quickly and will be key differentiating factors now and into the foreseeable future. More and more ‘non-traditional’ healthcare players are getting involved in supplemental benefits to deliver rewards like grocery stipends (Walmart Health + Optum).

But despite significant growth in on both the consumer directed and supplemental side, there were glaring problems Colin and Jason observed among legacy providers when conducting initial market research:

Colin and Jason noticed that healthcare benefits behaved like uncoordinated commodities. For instance, when interviewing executives, First Dollar’s team heard statements like “We have a hodgepodge of legacy solutions supporting our benefits. We have 4 vendors, 4 cards, 4 portals, and benefits live outside the primary member experience.” The disconnect in offerings often resulted in member frustration:

- Benefits were hard to understand, increasing the need for customer support and driving a low Net Promoter Score (NPS) for providers;

- Even worse, members weren’t using their benefits. The First Dollar team gave me an eye-opening statistic that a whopping 50% of benefit dollars in financial vehicles like FSAs are forfeited each year. Forfeited. Gone. Poof.

On the administrative side, things weren’t much better. Plan Administrators (TPAs) found the pool of product offerings at the time difficult to navigate with few consumer-centric offerings, especially in more nuanced, “non-simple-path” cases.

Through legacy offerings, TPAs and other health plan administrators didn’t have visibility into benefit failures and couldn’t control their data or customize the platform experience.

For my benefits administrators fam out there – let me know if any of these pain points sound all too familiar:

- “In a commoditized benefit market, we struggle to offer a competitive,differentiated benefits solution.”

- “We don’t have any visibility into CIP failures. Legacy solutions fail to offer self-service tools to manage core banking functions like KYC, settlement, and reconciliation that impact service quality and cause significant delays.”

- “Doing overfunded corrections is a painful, manual process. Legacy solutions have hidden and expensive change orders when attempting to adapt to our unique business and customer service model.”

- “To add beneficiaries they need to log in to the legacy solution’s UI. Legacy solutions offer limited APIs or widgets to more deeply integrate into our customer portal where we offer other products, like COBRA, IRAs, and 401Ks.”

I’ll bet they do. And you’re falling behind by sticking with legacy solutions.

Now that we’ve talked about the current state of the health benefits space, let’s dive into how First Dollar addresses these problems.

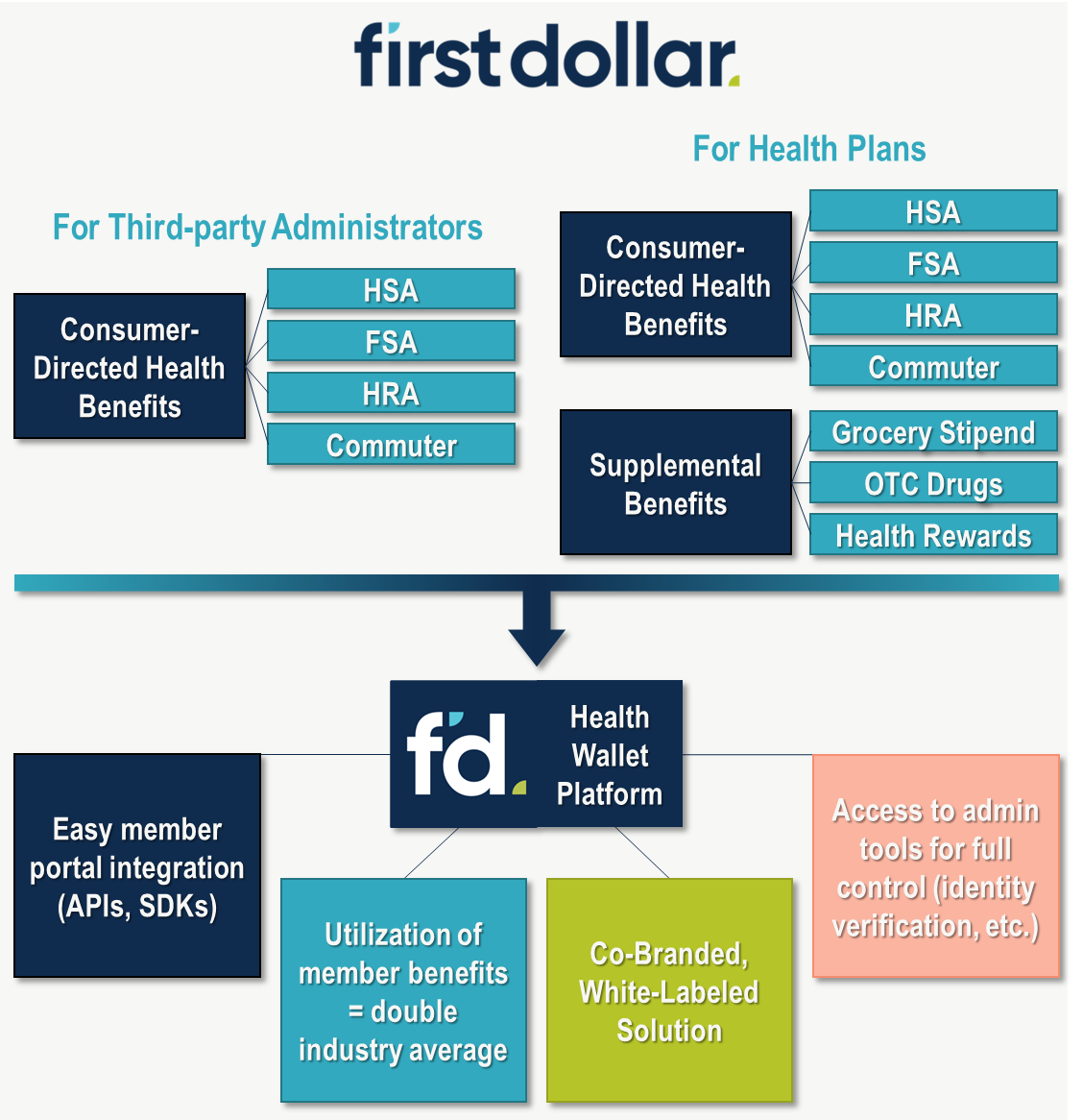

First Dollar’s Customers and Value Prop

First Dollar’s customers are any company that administers health benefits or is looking to connect/integrate health benefits into their own platform. These partners include:

- Health plans;

- Third-Party Administrators (TPAs) and Professional Employer organizations (PEOs);

- HR software and benefit platform vendors; and

- Financial institutions

First Dollar develops its SaaS product as a wholesale offering to TPAs, health plans, and financial institutions. Those entities then either (1) repackage First Dollar’s infrastructure into their own white-labeled product (or co-branded) or (2) embed the First Dollar offering into their existing platform via widgets or First Dollar’s API. At that point, First Dollar’s customers then turn around and sell the complete package to employers, tacking on a markup. First Dollar makes money by charging its partners for account servicing and payment processing.

The below is a nice visual of First Dollar’s customers, needs and ways First Dollar solves them:

So how is First Dollar Built Different?

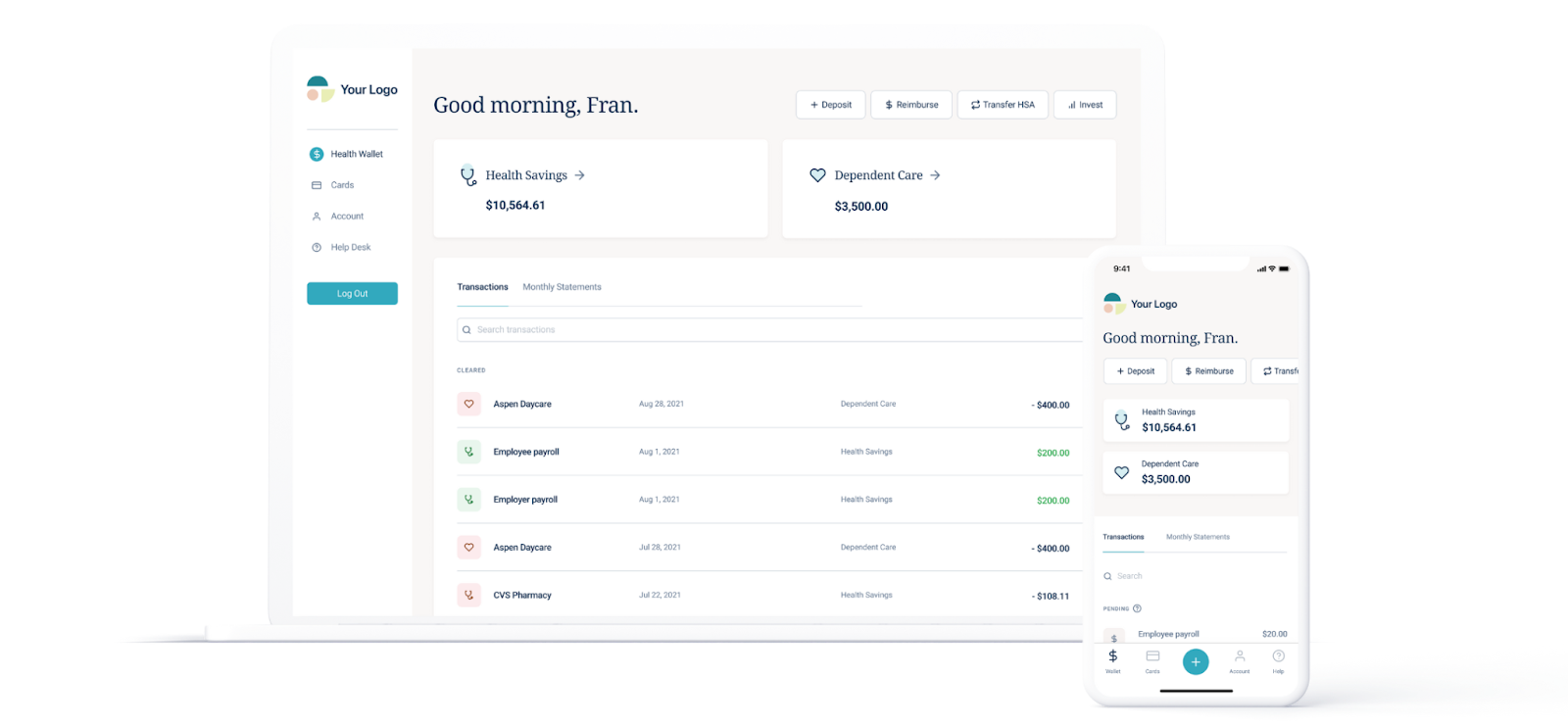

Here’s First Dollar’s secret stuff: Health Wallet. It’s like Michael Jordan’s water, but for health benefit administrators.

Health Wallet is First Dollar’s answer to all of the pain points they’ve heard from customers in health benefits. Here’s a quick rundown of what they’ve built:

- One Platform for all Benefits: Employers are inundated with point solutions. Rather than disjointed, glued together benefits portals across several providers, Health Wallet works through one single platform. Administrators get to work with a single partner rather than 5.

- Integration: First Dollar offers flexible APIs, widgets (SDKs), and is card agnostic. They don’t care what card you use (but they have one); they don’t care about whether they’re included in the branding.

- Feedback: Health Wallet provides better visibility into key performance metrics including failures involving things like funding and remediation issues. The team listens and iterates on customer pain points.

- Admin Control: Health Wallet gives benefit administrators complete plan design and control. Administrators own their own data and experience including key control features like identity verification (which is a huge problem for banks when working with HSAs and identifying customers). Easier control = fewer humans needed to manage customer service lines and resolve issues = cost savings.

- Design: The First Dollar team invests heavily into their design, making thoughtful design decisions based on feedback from end users and plan administrators. That design focus also trickles down to the consumer, finding ways to save consumers money on drug spend, health rewards for completing certain goals, consolidating all benefits into one card, and offering bilingual services.

- Usage Optimization: Get this – First Dollar actually wants you to use your benefits. Low benefits utilization tends to stem not from bad intentions, but from poor product design and lack of feedback on users. First Dollar holds industry expertise on nuanced problems that TPAs and administrators face daily, and that expertise will continue to grow as their team collects data, adds more admin features, and increases end user satisfaction. As its benefits database grows, partners will be able to continually iterate on their offerings in order to lower costs further and boost engagement. Higher satisfaction = increased usage = direct pull-through to revenue – in some cases, a 3x ROI.

So what does this all translate into for TPAs and health plans? Cost savings. Higher satisfaction. More usage of benefits. Competitive offerings. More revenue. Happy HSA users amiright. And shout out to the HRA too – I’d still have a crooked nose (no, I won’t show you the pic).

It’s not all about identifying the problem in healthcare – that’s the easy part. The hard part is convincing benefit administrators that they need to move on! So far, Health Wallet’s capabilities and results speak for themselves and they’ve received high satisfaction scores from customers. While it’s not a definitive metric, it’s notable to point out that First Dollar’s latest NPS of 71 and customer satisfaction metric of 92 are well above industry averages.

Beyond the fluffy nice-for-presentations metrics, First Dollar has also seen a 36% increase in benefits utilization for members using its Health Wallet platform with 75.42% overall benefit utilization for claimed accounts (meaning any user who logged in within the past month). High engagement, high usage. Like I’ve mentioned, that increases revenue.

Blake’s Take

First Dollar checks all of the boxes on paper: they’re a scalable SaaS infrastructure product positioned in a large, growing market in an area of healthcare and fintech with obvious need for tech transformation and platform connectivity. Consumers are demanding more intuitive health benefits products – the HSA is extremely popular – and employers will have to address that need.

Consumers are also still learning about the incredible capabilities of health benefit financial products: “Based on our experience, consumers are still learning about HSAs and other similar tax-advantaged healthcare savings arrangements. The willingness of consumers to increase their use of technology platforms to manage their healthcare saving and spending tax advantaged benefits will impact our operating results.” – Incumbent competitor

To add to the consumerization trend, healthcare payments are getting smarter and easier:

- Revenue cycle managers are enhancing connectivity on-platform between payors and providers, integrating HSAs and FSAs into patient portals.

- Costs are becoming more transparent and patients will more easily understand what they owe for services at the point-of-sale.

- Healthcare is less and less affordable as deductibles rise.

All of these trends point to rising demand for health benefits. And First Dollar is well-positioned for growth as a human-centric infrastructure layer in the space, with Health Wallet designed to address major day-to-day pain points for both its customers and end users.

The HSA will continue to expand in scope through regulatory change. I’d expect to see the health financial vehicle change over the coming years, perhaps even evolving into a health freedom account to cover even more aspects of healthcare costs like premiums or direct primary care subscriptions.

While aiming to break into incumbent market share, First Dollar will also need to watch its back to maintain its differentiation from new venture-backed competitive threats, a never-ending challenge!

What’s ahead for First Dollar

Although a long potential runway is in front of them, there are still plenty of questions First Dollar will have to answer. Execution and communication of their value prop to benefits administrators will be key, and hopefully this post helps with that! I’ll be interested to hear how the First Dollar team takes on the challenge over the coming years.

If First Dollar continues to find success, the sky’s the limit. First Dollar’s long-term bet is to build the spending tools for consumers to ultimately power up to 50% of health benefits in the U.S. But their ambitions don’t stop there. They want to become the rails powering all of healthcare spending + payments in general.

Time will tell!

That’s it for this week! Join 14,000+ executives and investors from leading healthcare organizations including HCA, Optum, and Tenet, nonprofit health systems including Providence, Ascension, and Atrium, as well as leading digital health firms like Tia, Carbon Health, and Aledade by subscribing here!