Ascension Turnaround Takeaway #1: M&A has Improved the Nonprofit’s Financial Trajectory

Ascension is on a soul-searching journey. Just look at all of the recent activity from the national hospital operator:

- June 2025: Acquires AmSurg for $3.9B (announced)

- April 2025: Acquires remaining 80% of Cedar Park Regional Medical Center from CHS

- March 2025: Sold 4 hospitals and associated assets to Beacon Health System

- March 2025: Divested certain senior living facility assets to various purchasers

- March 2025: Sold Presence Care Transformation Corporation to Prime Healthcare – 9 hospitals, 4 senior living facilities, and associated assets.

- November 2024: Ascension sells St. Vincent’s Health System to UAB Health

- October 2024: Ascension contributes Ascension Michigan membership interest into a noncontrolling stake in Henry Ford Health System

- August 2024: Sold 3 hospitals and associated footprint to MyMichigan Health, exiting northern Michigan market.

- July 2024: Sold 9 hospitals and associated footprint to Prime Healthcare, Prime’s largest acquisition to-date and reflecting Ascension’s further retreat from Chicago/Illinois market.

- June 2024: Sold St. Vincent’s Health System in Alabama to UAB for ~$450M.

- June 2024: Ascension Personalized Care (its ACA plan) exited Texas

- May 2024: Ascension experiences system-wide cybersecurity incident.

- March 2024: Sold certain Ascension Health senior care assets to Villa Investment Partners

- February 2024: Transitioned Ascension Pittsburg to Mercy

- February 2024: Transitioned Our Lady of Lourdes Memorial Hospital to The Guthrie Clinic

- February 2024: Nationwide Change Healthcare cyber attack

- December 2023: Formed JV with Lifepoint Health to jointly own Highpoint Health System consisting of 3 hospitals & assets in Tennessee.

- November 2023: Divested its 50% stake in Network Health to Froedtert Health giving Froedtert full ownership

- October 2023: Formed a joint venture with Henry Ford Health System and contributed all Ascension southeast and mid Michigan hospitals to the JV. Ascension gets ownership % in HFHS.

- October 2023: Sold Providence Hospital in Alabama to the University of South Alabama Health Care Authority.

After getting through that laundry list of deals, you can see Ascension has been one of the more active members of the hospital M&A clan.

Adding to the above M&A activity, Ascension also dealt with 2 cybersecurity incidents in 2024 – one being the Change Healthcare issue, then an isolated event tied to Ascension in mid 2024.

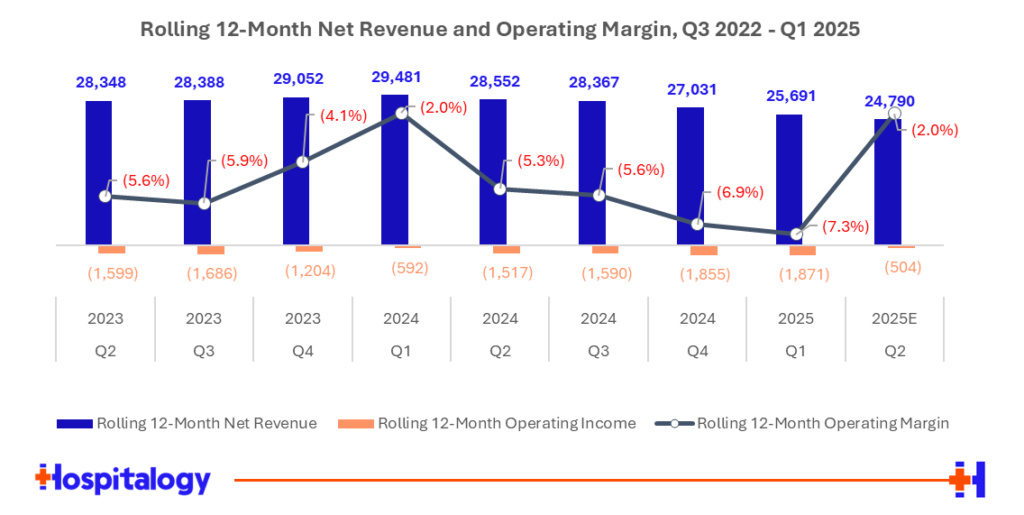

In the first three months of 2025 alone, Ascension sold an additional 13 hospitals and acquired one. So using hospital divestitures as a proxy for revenue decline, we should continue to see the health system’s expense profile improve as it closes out its fiscal 2025 and moves out of unattractive markets:

So what does this all translate into over time?

Improving payor mix, better expense profile, and slowly expanding margins.

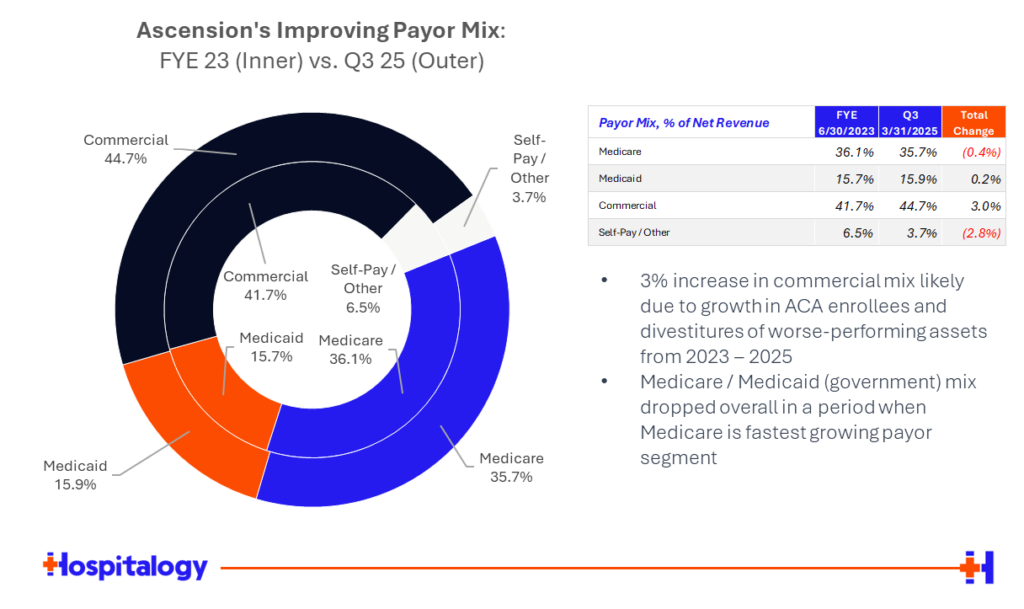

Turnaround Takeaway #2: Improving Payor Mix

Similar to other nationally scaled health systems, Ascension saw an uptick in commercial (employer sponsored) mix from 2023 to 2025. Without having explicit, intimate knowledge of what’s happening in Ascension markets, I would also make a reasonably educated guess that divestitures of poorly performing assets also compounded this effect by moving off of government heavy mixes. That obviously brings into question whether those divested hospitals have found a sustainable spot in their respective communities.

Ascension also noted a slight uptick in case acuity, and a 1.4% increase in net revenue per adjusted discharge on a same-facility basis as payor negotiations have yielded larger increases.

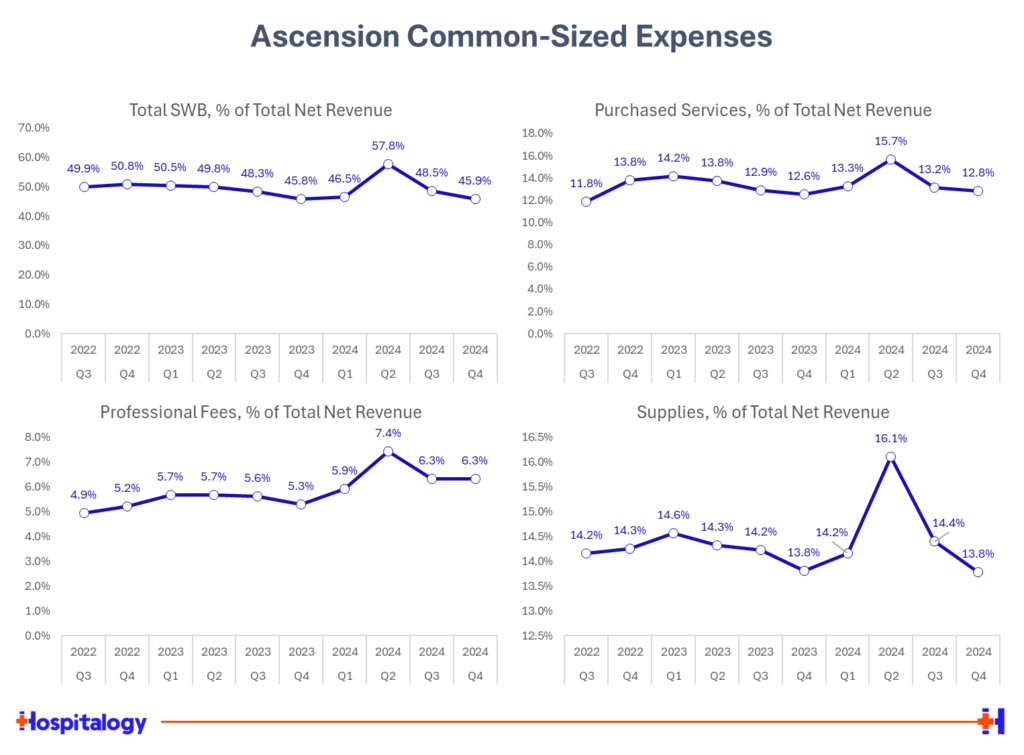

Turnaround Takeaway #3: Better Expense Profile

If you ignore that really ugly calendar year Q2 (being the cyber attacks) Ascension seems to have gained some leverage over its expenses in recent quarters. On a per patient day basis, most expenses are flat over the past few quarters. SWB in particular hit a low and on a same-facility basis dropped 0.7% as a result of Ascension labor efficiency initiatives, workforce stabilization, and higher retention (90 day rate of 88.3%) leading to lower contract labor costs and lower benefits costs.

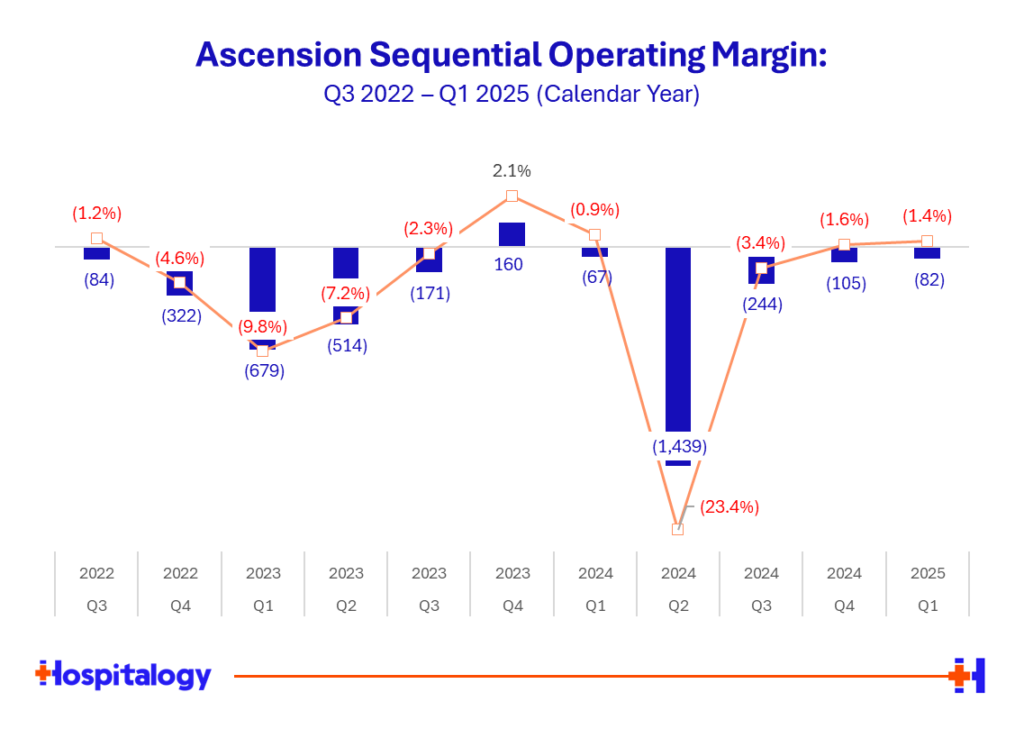

All of this leading to an …somewhat improving operating margin, with some noise in there stemming from a tumultuous second quarter (on a calendar year basis):

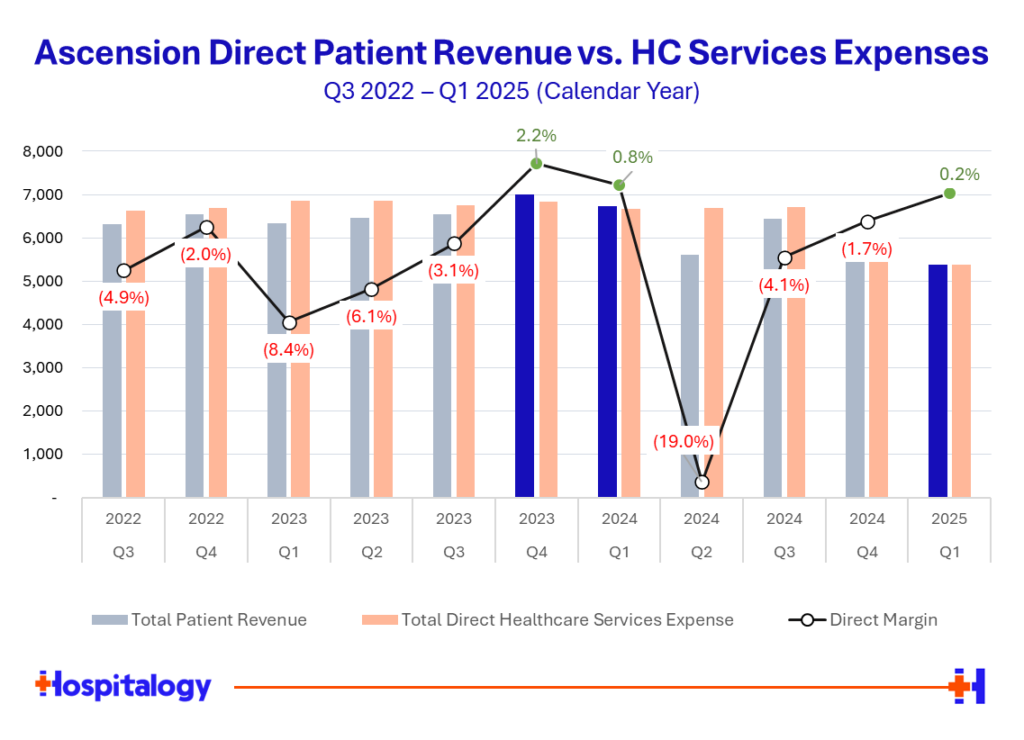

Turnaround Takeaway #4: Positive Services Margin

Something that certain nonprofit systems do that I wish the public operators would is breaking out their revenues by segment – inpatient, ambulatory, long-term care, etc. They also break out their expenses by those attributable to direct patient care versus admin / overhead. So you can see in the below graphic, when comparing net patient revenue to attributed patient expense (so excluding other operating revenue), Ascension is pretty much break-even, but trending in the right direction most recently:

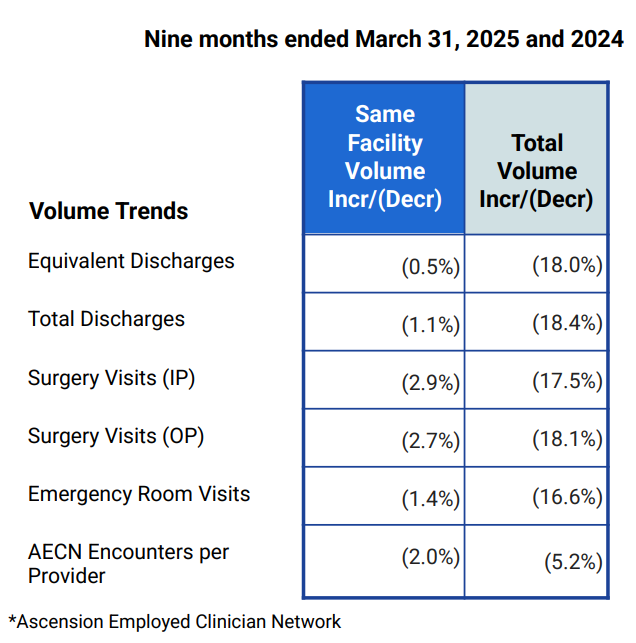

From a volume perspective, on a same-store basis, Ascension noted its volume fell 0.5% compared to the same 9-month prior period, given the variety of disruptions Ascension faced in 2024. I’d expect much stronger numbers next year on an easy comp as these procedural volumes get rescheduled or push outpatient, and you can see that effect in the Q3 numbers on a standalone basis: “Ascension’s same facility volumes for key indicators for Q3 FY25 YTD have generally increased 6-7% on a per-day basis as compared to the comparable per-day volumes during Q4 24 (quarter impacted by the cybersecurity attack). Note that it’s important to analyze Ascension volumes on a same-facility basis given the many divestitures.

Turnaround Takeaway #5: AmSurg, and Liftoff – Achieving Health System Transformation?

Look at where Ascension is making strategic ACQUISITIONS – purchase prices aside (if that information ever comes to light): a hospital in Austin, Texas (where Ascension already has a decent footprint and a strong demographic profile) and outpatient ambulatory care – 250 ASCs across 24 states as Ascension experiences outmigration of volumes and wants to reorient its growth strategy while diversifying its book.

- This transformative acquisition will add more than 250 ambulatory surgery centers across 34 states to Ascension’s network, significantly expanding its ability to deliver care in community-based settings, upon closing of the transaction. These centers specialize in gastroenterology, ophthalmology, orthopedics and other services that are increasingly sought after by patients looking for convenient, lower-cost alternatives to traditional inpatient care.

Surgery Partners is currently valued around $8B on the public markets with a revenue multiple around 2.5x. Using this as a proxy and with almost $1B in revenue in late 2022, you could guess AmSurg’s revenue today sits around $1.5B.

After 2025, Ascension will operate a MUCH larger outpatient revenue footprint and profile as it diversifies beyond the four walls of the hospitals and we should see the outpatient revenue base outstrip inpatient revenues soon thereafter.

Ascension has found some initial success with its Ascension Rx initiative as well, noting the following in its fiscal Q3 update:

Join the thousands of healthcare professionals who read Hospitalogy

Subscribe to get expert analysis on healthcare M&A, strategy, finance, and markets.

No spam. Unsubscribe any time.

- In addition to optimizing our acute care assets focused on patients with more complex needs, we continue to invest in accelerating growth through our ancillary services and ambulatory networks. An example is the growth of Ascension Rx, building upon our existing retail pharmacies through growth of specialty pharmacy and a nationwide mail order distribution center. Additional investments are also being made in our ambulatory surgery centers (ASCs), imaging and outpatient physical therapy sites that enhance Ascension’s footprint of service offerings and provide greater access and convenience to consumers.

Finally, in related news, Surgery Partners rejected Bain’s take-private offer and it makes perfect sense with large ASC platforms in scarce supply and as hot commodities.

Quick Notables

Collaborations, launches, and other tidbits to keep on your radar.

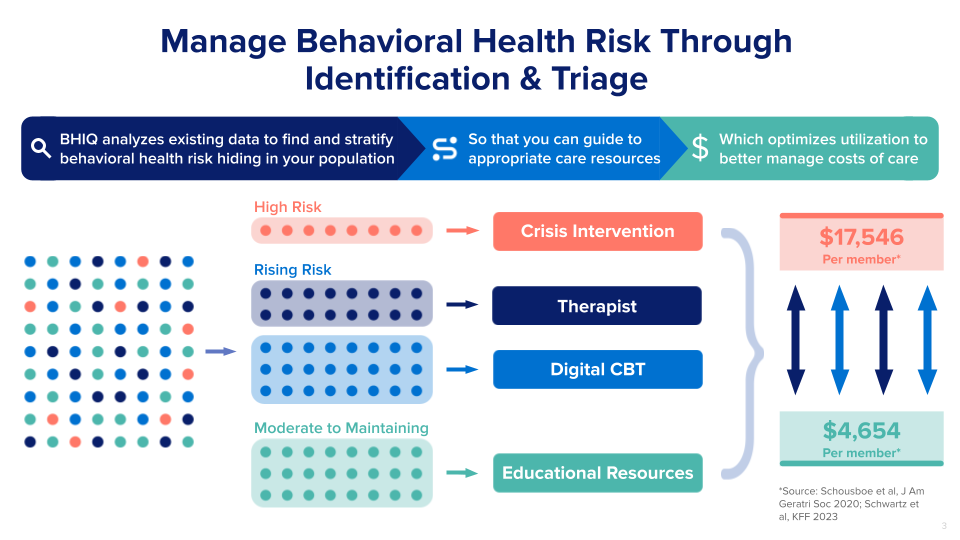

- NeuroFlow announced the release of its BHIQ solution, an AI-driven platform aggregating behavioral-health data and risk scores for clinicians. The NeuroFlow team was kind enough to share a graphic with me breaking down the new platform and how it helps health plans and health systems create better risk management strategies for behavioral populations by identifying and stratifying behavioral health risk:

- HealthVerity and MedeLoop partner to fuse RWE data with AI analytics for faster, deeper study insights.

- DispatchHealth and Medically Home complete their merger, creating a national home-based complex-care platform, and the overall company valuation took a hit in the process given the consolidation.

- OneOncology and START Center partner to expand San Antonio cancer services.

- Longevity Health extends its partnership with Humana to serve Medicare Advantage members.

- Net Health acquires Limber Health to embed AI-powered therapy management into its rehab software.

- McKesson completes acquisition of Core Ventures, expanding its digital-health investment portfolio.

- Hello Heart guarantees employers at least 5% cost savings on cardiovascular benefits under its new performance guarantee.

- Cairns Health commercially releases Luna, an AI companion for senior and home care.

- Amavita unveils a multi-million-dollar CV ASC in Kendall, FL.

- Quantum Health signs agreement to acquire Embold Health, broadening its patient-navigation suite.

- Healthie launches Dev Assist, AI-native tooling for rapid app development.

- Corify Care announces AI collaboration with Mayo Clinic to enhance arrhythmia care.

- Tempus One debuts in-EHR guidelines integration for evidence-based care.

- Spruce Point issues a strong-sell report on Tempus AI, citing overvaluation.

- Clarify Health sale draws bids from Barclays, KKR and SoftBank in a $1.2 B auction.

- Jane Software hits a $1.8B valuation after TCV leads a $500 M round.