SF friends! Come visit me on Wed 9/11 for HealthTech Hang’s happy hour.

I am cohosting with Harry Goldberg from HealthTech Hang and Ben Kromnick from Mercury.

It’s been a while since I have been in the Bay Area, and I would love to say hello!

The first 20 folks to register get a free ticket with coupon code HOSPITALOGYVIP

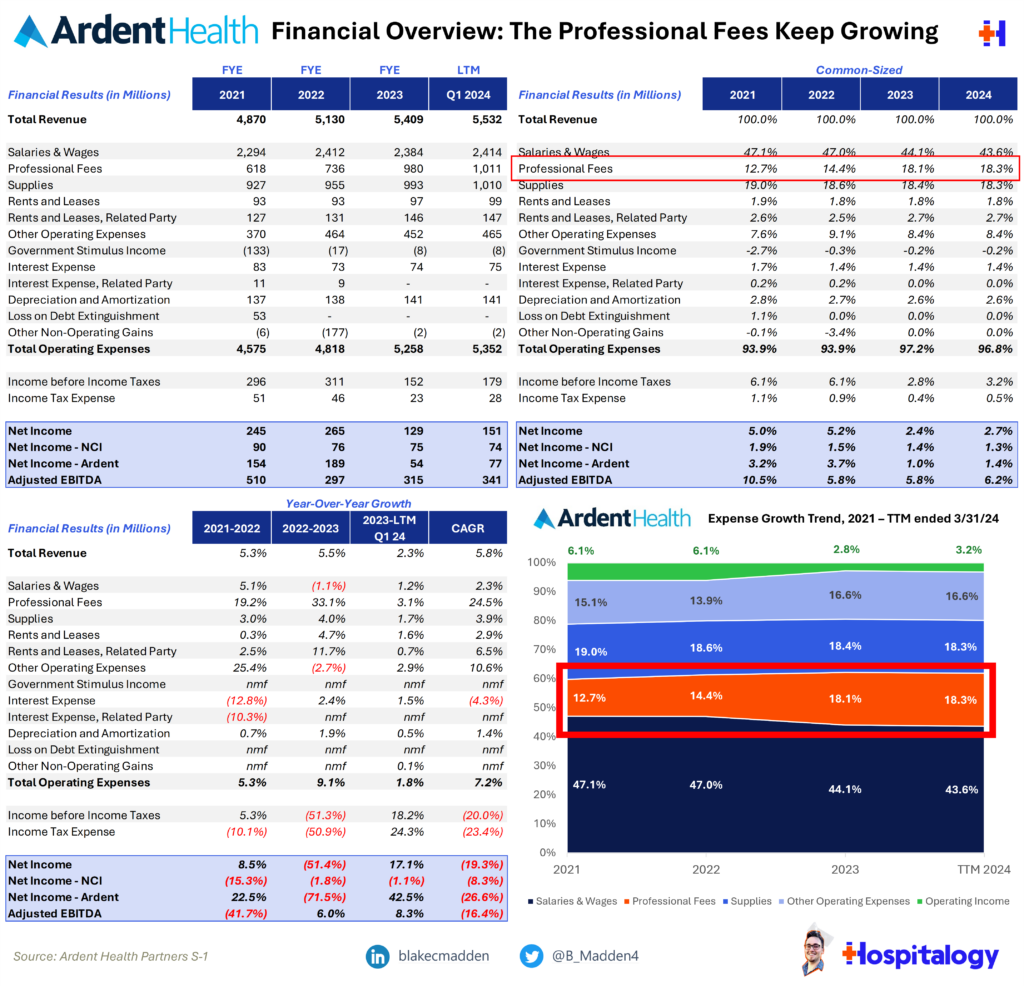

Ardent Health Hits the Public Markets

After expecting to price its IPO in the $20-$22 share range and raising just south of $300M net of fees, Ardent Health instead raised $192M at a $16 share price in its debut on the public markets.

While Ardent has held its weight so far on the public markets (trading up 12% to north of $17/share), the relatively muted debut leaves me wondering what the investor appetite is like for upcoming IPOs. There are a few different factors at play here, including lack of large scale exits / M&A, potential interest rate cuts on the horizon, oh…and of course, that whole Presidential election thing.

Ardent as a health system is a really interesting company, and one I’ll be looking forward to covering. The operator holds a joint venture first strategy (18 of 30 hospitals are JV’d) and targets mid-sized MSAs. To date, Ardent operates in 8 regional markets, all of which have under 2 million in total population, through 30 acute care hospitals in 6 states – Texas, Oklahoma, New Mexico, New Jersey, Idaho, and Kansas. Other notable parts of Ardent’s footprint includes 200 sites of care, 1,700 affiliated / employed physicians and clinicians, and 80 contracts with value/quality components across multiple ACOs and 220k covered lives.

The $192M raised will go toward paying down debt, working capital, funding ever-growing professional fees, expanding into new markets, and building out ambulatory networks in existing markets.

Financially, Ardent generated $5.5B in the trailing twelve months ended March 31, 2024. Revenue wise, its size puts the health system on par with the likes of BayCare and the newly formed Endeavor Health.

Read the S-1 linked here for the full lowdown. For everyone else, you can pass along this Thursday’s Hospitalogy as I’ll be diving deep!

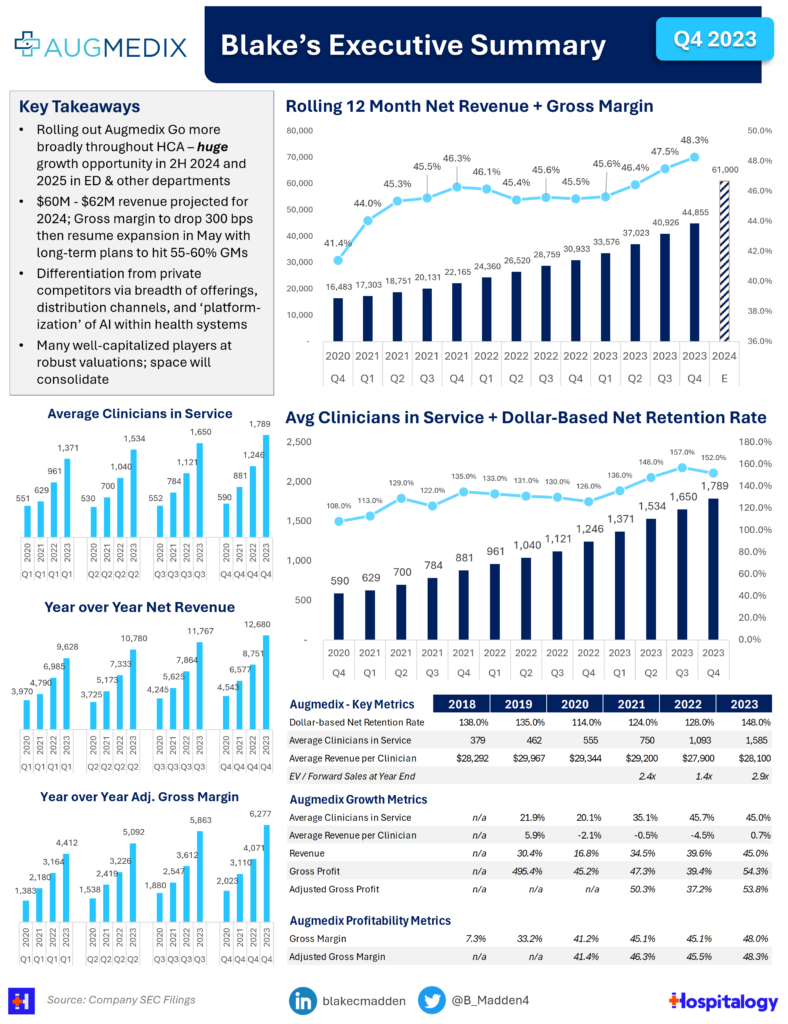

Commure Acquires Augmedix in First Move to Consolidate AI Scribe Space

The other big story that caught my eye this week was some consolidation in the AI scribe space, and a notable move for Commure. The digital health tech platform player is acquiring ambient documentation and AI scribe player Augmedix for $2.35 / share – a 169% premium to the stock’s 30-day volume weighted average price (VWAP, for you savvy investors).

At an implied enterprise value of ~$122M and Augmedix’s forward revenue guidance of ~$54M, the implied revenue multiple here is … does a quick excel calc … around 2.2x.

I’m a bit sad. I enjoyed following Augmedix as a public company, and the growth story was there with its recent marquee partnership announcement with HCA along with holding several notable enterprise customers. As you can see above, Augmedix had solid retention numbers as clinicians in service grew steadily quarter-over-quarter.

But overall, it’s a good deal for all sides. Augmedix had some promising operating results but was dealing with a few issues:

- Business model transformation – Augmedix operates a trained workforce in Bangladesh used in its human-centric outsourced medical scribe products, but unfortunately this business segment was getting cannibalized by lower cost, software-light AI products (hospitals were choosing Augmedix Go over higher dollar offerings)

- The so-called AI scribe space is a crowded one. Augmedix competed directly with Nuance on enterprise while Abridge is making quick, impressive headway into the realm notching several partnerships in recent memory (and launching some other interesting stuff like scribe-specific products for nurses). Meanwhile, Ambience, Nabla, Suki & others are increasingly involved with recent capital raises or differentiated growth strategies (e.g., Suki with FQHCs). Sharks are swimming, and blood is in the water.

- Between business transformation and path to profitability, Augmedix had some balance sheet issues & its stock price had deteriorated big-time over the past year.

In short, in the private markets Augmedix is a great acquisition and complement to Commure’s suite of offerings. In late 2023, Commure merged with Athelas and was last valued at $6B with fresh funding from General Catalyst. It has plenty of capital privately at its disposal and significant runway.

Join the thousands of healthcare professionals who read Hospitalogy

Subscribe to get expert analysis on healthcare M&A, strategy, finance, and markets.

No spam. Unsubscribe any time.

Along with the capital and tech, Commure acquires existing relationships with 20 or so of the largest health systems, including CommonSpirit and most notably, HCA where Augmedix is piloting its AI-focused solution in the ED setting. Commure already holds existing relationships with HCA, so this move is sure to deepen the relationship.

The tech platform can also offer a more robust suite of products to enterprise customers (health systems), and this is the direction the healthcare world is heading, meaning Commure – now combined with Augmedix – holds a much more compelling and efficient go-to-market strategy than standalone Augmedix could likely ever achieve. For that reason, you should expect to see more consolidation in this and adjacent spaces.

I’m hoping to have conversations with both Ian Shakil from Augmedix and Tanay Tandon from Commure in the near future, so potentially more updates to come!

Surgery Partners up for Sale?

Backed by Bain, independent ASC management company Surgery Partners is rumored to be up for sale, as reported by Bloomberg.

Potential suitors include USPI (Tenet, who just by the way, found itself with a lump of cash after selling off several hospitals) and Optum-owned subsidiary SCA – with an outside chance at HCA after its newly formed subsidiary Surgery Ventures went online. I’m also curious to see where AMSURG ends up. I’d heard rumors of sales interest there as well after its split from Envision, but the firm may forge its own path. The ASC management space will continue to see interest for the foreseeable future, so pay attention!

The Weekly Executive Summary

Notable moves, policies, and strategies from around healthcare.

This value-based care overview from Town Hall Ventures’ Andy Slavitt and Andie Steinberg is a must read on implications for new Medicare proposals on the horizon.

Select Medical is soon to spin off Concentra and will own 80% of the spun off occupational medicine player. Concentra has exchanged hands a few times over the years. In Q2, Concentra generated $478M in revenue and operating income of $84M – a nice, steady business. The firm will offer 22.5 million shares between $23 and $26/share, expecting to raise $500M+. More info and analysis to come! S-1 here.

Beckers had a helpful summary of health system joint ventures and where the puck is going – outpatient surgery, of course, in the limelight.

Health systems continue to eye a ‘multi-region’ model.

Read this overview from Kaufman Hall’s Lisa Goldstein on the potential for GLP-1s to up-end the hospital industry. These are questions health system leaders – and the healthcare industry at large – will grapple with over time.

Rock Health’s 1H 2024 funding update. Early stage deals – particularly Series A – are in. At an annualized rate, 2024 funding will exceed 2019 and 2023 levels. Bullish.

TowerBrook Capital Partners and Clayton, Dubilier & Rice are considering a rival bid for publicly traded revenue cycle player R1 RCM in competition with the current take-private offer from New Mountain Capital. A potential buyout would come at a hefty price tag and would comprise one of the larger take-private’s in recent memory at $5.6B+

Elevance is warning about rising acuity and utilization in Medicaid. Meanwhile, Astrana Health continues to stay busy commercially as it announced a partnership with Elevance’s Anthem Blue Cross in California.

Read this overview from Stat to catch up quick on Kamala Harris’ healthcare policies.

The U.S. fertility rate falls to a record low, implying that millennials and Gen Z are gonna have to pick up that Medicare bill even more!

Change Healthcare is getting sued.

Tenet is facing issues with its Desert Healthcare District lease agreement.

Can JnJ’s ketamine drug treat depression? It thinks so.