GLP-1s are on track to be one of the most profitable drug classes of all time – and everyone wants in on the action.

With the growing conversation around obesity, there’s also a controversy bubbling under the surface ready to overflow.

No, I’m not talking about my terrible pasta making skills (how do you keep it from bubbling over?? I leave the starch making to my wife). I’m referring to Hims – and other DTC telehealth offerings – leveraging a loophole to sell GLP-1 medications directly to consumers. Or rather, versions of GLP-1s via compound pharmacies. It’s a thriving parallel marketplace. Call it the Underworld of Healthcare.

Here’s how it works. As long as a drug is in shortage, it can be made off-label via compound pharmacies. A compound pharmacy purchases the active ingredients themselves create their own ‘compounded’ versions of GLP-1s.

Hims just held its Q2 earnings call, and we’ll center the bulk of the conversation and controversy around them given the public availability of information along with the amount of discussion GLP-1s generated during the Q&A.

Hims would tell you its business case is simple: GLP-1 demand vastly outpaces supply, and it wants to offer weight loss solutions and expanded access to GLP-1 medications to its subscribers. Hims would also tell you its compounding environments are tested on behalf of patients. Investors and analysts have called out Hims’ compounding operation as a differentiator and competitive advantage in the DTC telehealth space. But issues can arise – e.g., impurities, immunogenicity – to cause concern.

So ultimately, the issue boils (Aha! My pasta theme continues) down to the consumer. The burning question is whether Hims customers are made aware, understand, and are willing to take on risks with an off-label product, even if it is delivered via slick marketing and a consumer-friendly interface.

For Hims, the growth strategy is a no-brainer. As a DTC telehealth player, you have to be involved in the market even if the GLP-1 boost functions as a short-term cash grab. GLP-1s hold massive demand with a total market size estimated to exceed $100B+ by 2030. At the bare minimum, significant, asymmetric upside exists in the immediate short term in the following forms:

- Cheaper subscriber acquisition stemming from the hype and a leading DTC brand name (marketing expenses as a % of revenue dropped 5% to 46% through strong retention, brand recognition, and lower-cost acquisition channels);

- Lower churn – obesity-focused subscribers are on-platform with longer-term commitments (i.e., it takes multiple months to get to the right dosage or see side effects – how convenient!)

- Short-term revenue and cash-flow generation to reinvest into other aspects of the business;

- Downstream ability to cross-sell obesity subscribers into other verticals; and

- An outside, existential chance you win patent/IP disputes over Big Pharma to continue offering slightly different GLP-1s to consumers long-term (or some sort of other sustainable workaround).

For now, in the midst of the shortage, we’re seeing this obesity play going exactly as expected. For context, Hims launched its comprehensive weight loss portfolio in December 2023 and complemented this offering in May 2024 by announcing GLP-1 access for Hims customers – oral medication kits first for $79/month and then compounded GLP-1 injections for $199/month.

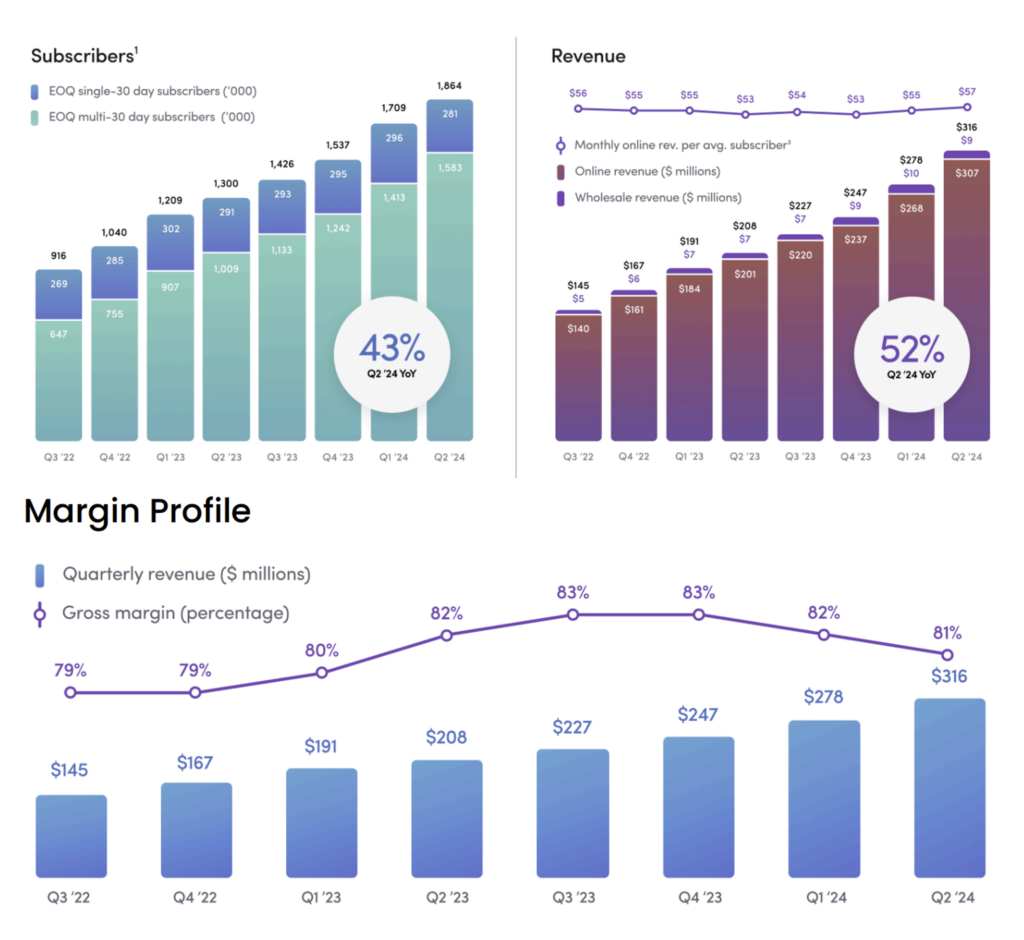

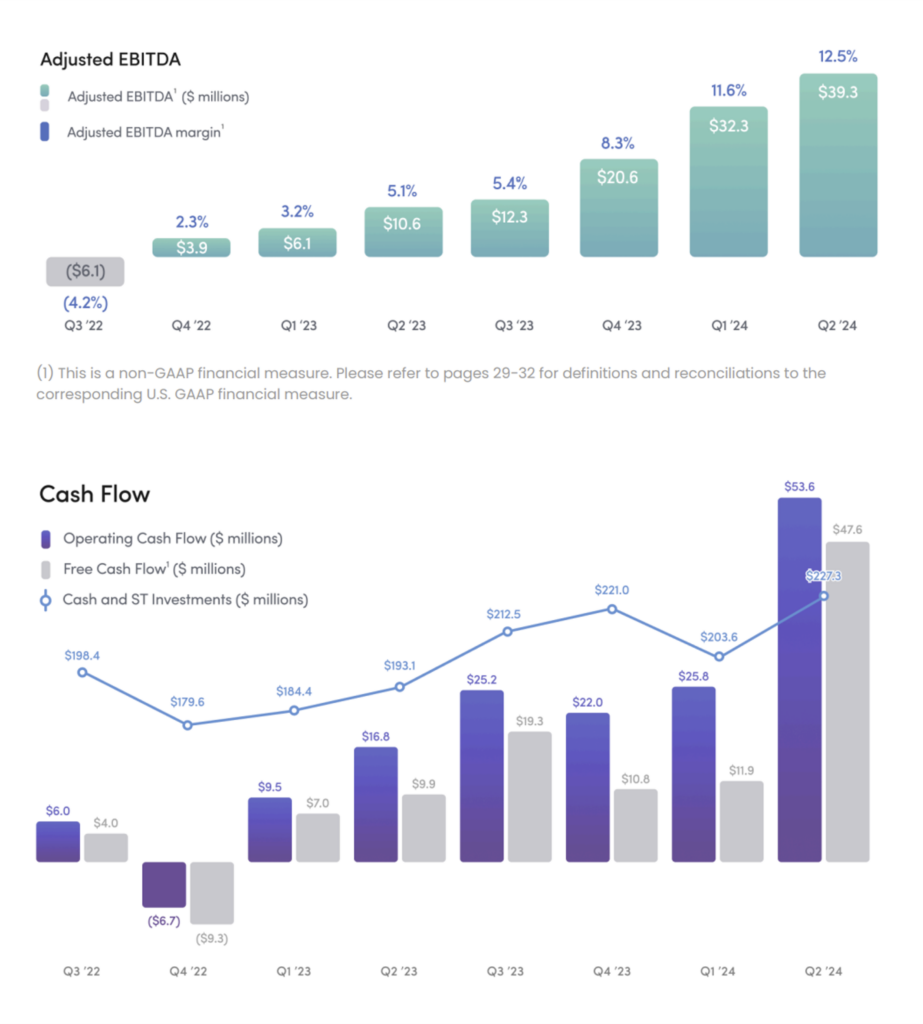

After 7 months, the offering is generating $100M in run-rate revenue across 100k incremental subscribers. Hims is active with its GLP-1 offering in 30 states.

So all in all, Hims & Hers is performing well so far in 2024 – even when removing the hyper-scaling obesity segment. The Hims company narrative is intact and growing. And I want to reiterate this point within the context of my overall write-up here: DTC telehealth is a good thing for consumers. Those who subscribe enjoy using the product, and they stay on-platform. It’s consumer friendly for many low-acuity uses.

About that whole Shortage thing…

The interesting dynamic at play here is…Hims doesn’t share investor concerns around the massive business risk associated with compounding GLP-1s during a shortage and capitalizing on a technicality.

Hims seems to think it has found some sort of precedent – some of Mike’s Secret Stuff – to work around existing patent protections and continue to grow the obesity segment in the event the shortage ends. In fact, I found the tone of the answers below to be somewhat dismissive, nonchalant, and confident as it pertains to the durability of Hims’ obesity segment and fantastic growth the business is experiencing, obviously stemming from short-term hype.

And per commentary from Eli Lilly leadership, whose ads you probably saw 100,000 times during Olympics coverage, the tirzepatide GLP-1 shortage is coming to an end ‘very soon.’

There are 50+ mentions of obesity and weight in Hims & Hers’ Q2 call. From the Q2 earnings call Q&A, here are some remarks from leadership answering questions around durability of obesity segment and GLP-1s:

Answer #1

Join the thousands of healthcare professionals who read Hospitalogy

Subscribe to get expert analysis on healthcare M&A, strategy, finance, and markets.

No spam. Unsubscribe any time.

“…But in addition to the oral compound, the branded medications, the personalized GLP-1 doses, which augment the commercially available dosages for patients that need it as well as off-patent GLP-1s like liraglutide, I think we believe the combination of that portfolio, allows customers and providers a really robust range of offerings that we think is very durable. I think this will exist and expand beyond the shortage dynamics. I think there’s really established precedent with regard to the compounding exception, which allows for this level of personalization that we’ve spoken about for patients that need it. And I would expect that the clinical necessity of that will be really clear with these medications as people know, there are real side effects. There are really no one-size-fits-all dynamic. But we think there’s a really robust platform that extends well beyond the shortage across a number of these avenues.”

Answer #2

“…The short answer is that the compounded exemption, it’s relatively clear, and there’s been decades of established precedent with regard to what qualifies as personalized. And this often is a form factor as you outlined or it could be dosing dynamics of a patient is not getting the outcome that they’re hoping for, are they experiencing side effects that are intolerable. So these types of customizations are relatively well established and I think the clinical necessity of compounding and the clinical necessity of personalizing medication is really well established, right? This is not overwhelmingly the case. But in many ways, the personalized dosages on [ augment ] what is commercially available. And so I think our personalization dosages that exist on the platform today are offering fantastic high-touch care to patients that otherwise really wouldn’t be able to experience the benefits of GLP-1. And I would expect in the future in a post shortage world, this also continues to exist for patients as an access point.”

Answer #3

I think at a high level, you should expect some degree of fluidity right over the next couple of years, just given I think there’s going to be not only a changing market dynamic with the current medication that are on shortage. But I think there’s also probably going to be 5 or 10 new medications that come to market in the next few years, just given if you look at the clinical studies and the FDA pipeline. So I think you’re looking at 5 to 10 years of innovation, all kind of expanding off of the initial GLP-1 learning and that first medication out there with liraglutide now coming off time. So I think what you can expect is some fluidity without question, where I think we get a lot of confidence is that there’s a really broad set of offerings under the hood that we believe in combination results in a really durable business line. As we talked about, the oral compounds that we have launched, that is — that in and about itself is the fastest growing specialty we’ve ever launched on the platform, achieving north of $100 million run rate just in 6 or 7 months. We expect huge evolutions in that platform and expansion of offerings there that patients really do love and are having great outcomes. And then on the injectable side, I think there’s going to be, without question, a long horizon of on and off availability, just given the demand.

Answer #4

“…The compounding titration end dose customization exists and operates regardless of shortage. This is an exemption for which we operate the entire business under and have for the last 6 or 7 years. And there’s really an established precedent where everybody in market really respect the clinical need of personalization and realizes that often these personalized dosages augment what is commercially available and are not directly cannibalizing large pharma. So when you think about very few, if any examples, where large pharma comes after legitimate clinically necessary compounding and what we’re seeing on our platform is that for these medications, that clinical customization is definitely needed for some patients. And we believe in combination with the rest of the portfolio, that will be included and available to patients over a long period of time.

So here are some takeaways on the longevity of the obesity platform:

- Even without GLP-1 craze they grew the business (profitably?) to a $100M run-rate in 7 months with oral weight loss medications alone

- We will see a flood of new GLP-1 medications enter the market and the situation will move quickly and be ‘fluid’ – including the introduction of oral compounds that may lead to other use-cases for Hims

- There is some sort of precedent that compounding certain elements like end-dosage or side effect mitigation is considered clinically necessary and therefore defensible

- Hims & Hers will also offer brand-name GLP-1s on platform, maybe alluding to expectations of reduction in out of pocket cost over time, or an increase in supply

My unsolicited thoughts for Hims would be to take advantage of this huge surge in cash and invest it into the sustainable, growing parts of the business. It does sound like Hims is going down this path, with lots of language during Q2 on educating consumers around Hims capabilities across multiple dimensions.

The Compounding Controversy

Pharma isn’t satisfied with these answers, and they’re worried about liability and cannibalization stemming from counterfeit or ‘black market’ usage of off-label GLP-1s.

Along with trademark issues and misleading marketing, Lilly, Novo Nordisk & their suite of lawyers are not fans of compounding either. The drugmakers would say compounded drugs are not FDA-approved, marketed with misleading or dangerous information, and therefore unsafe for consumers – and there is precedent for this given the 2012 nationwide fungal meningitis outbreak stemming from compounding drug facilities. Straight from the FDA’s website:

- Compounded drugs should only be used in patients whose medical needs cannot be met by an FDA-approved drug. Unnecessary use of compounded drugs may expose patients to potentially serious health risks. For example, poor compounding practices can result in serious drug quality problems, such as contamination or a drug that contains too much or too little active ingredient. This can lead to serious patient injury and death.

With the above FDA statement in mind, there is some regulation in compounding – but less than the typical drug manufacturing process. Hims produces compounded medications through a partnership with a 503B facility. These 503B facilities have slightly stricter regulations around process control. For instance, 503B facilities have to submit batches for testing and stability along with a self-regulated quality department. 503B facilities are licensed by the FDA, but the drugs they produce are not FDA-approved. You can imagine the confusion this distinction might create.

Lilly also published an open letter on June 20 warnings about off-label use, inappropriate use, misleading advertisements, dangers associated with compound medication, and more.

- “Lilly is the only lawful supplier of FDA-approved tirzepatide medicines—Mounjaro® and Zepbound®—and does not provide tirzepatide (the active ingredient in Mounjaro® and Zepbound®) to compounding pharmacies, med-spas, wellness centers, online retailers, or other manufacturers. Lilly does not know where compounding pharmacies or other sellers are obtaining the tirzepatide active ingredient they are selling.

- “Lilly will continue to pursue legal remedies against those who falsely claim their products are Mounjaro, Zepbound, or “FDA-approved” tirzepatide, including certain med-spas, wellness centers, online retailers, and compounding pharmacies.”

Simply put, the Big Pharma lobby is strong, the lawyers are ready and waiting, and we’re talking about the most commercialize-able drug in history. The stakes are high, fam.

TL;DR

We’re seeing several tidal, cataclysmic forces at play shaping the obesity market:

- America has an obesity problem.

- The conversation around obesity is shifting toward one of a chronic disease rather than a lifestyle choice.

- Study after study proves the efficacy of GLP-1s across countless indications with some concern around long-term side effects and weight regain.

- Patients hold overwhelming demand for GLP-1s, but access (supply + list price cost) creates constraints

- Employers and payors are grappling with benefit design and coverage access qualifications for GLP-1s (e.g., limiting to diabetes patients);

- Eli Lilly and Novo Nordisk want to control the supply and maximize their drugs’ economic potential while on patent, balancing both by providing rebates.

- It’s very unusual to see the extended shortage of a multi-billion dollar drug, leading to the funky dynamics we’re seeing

- DTC telehealth players (and in-person med spas, other wellness facilities) want to maximize their economics by expanding access to acquire/grow subscriber bases. A parallel marketplace has formed for off-label weight loss medications. Players like Hims, Ro, and others are generating revenue off a technicality in regulation. They are temporarily providing access to compounded GLP-1s – non-FDA-approved versions of the weight loss drugs – while on shortage. The longer the shortage, the more willing patients are more to engage in ‘riskier’ access options. But the practice of providing compounded GLP-1s is not sustainable, even if Hims and others try to fight it by creating ‘different enough’ drugs under the compounding process.

- This parallel marketplace has led to off-label drug usage, misleading marketing, counterfeit brand name drugs with high levels of bacteria or other impurities, and general concern for patient safety. Nobody knows what the heck is in compounded drugs from these no-name telehealth operators. In May, Australia banned compounded GLP-1s citing safety concerns.

- Until the GLP-1 shortage ends, drugmakers will have to balance commercial impact of this parallel marketplace against legal costs of winning trademark infringement, and larger drug patent / IP disputes. I.e., is the juice worth the squeeze?

- Direct-to-consumer offerings like Hims, Ro, and others are riding the obesity hype wave to acquire customers with the promise of cheap GLP-1 access. What they do with the cash in the short term will define their future business success.