If you’ve missed my recent Hospitalogy emails and announcements, I recently revamped my community offering – including new pricing tiers and better benefits. I’m gathering a great group of folks working in health system strategy, corporate development and similar functions.

If you’re a VP or Director working at a health system or provider organization, you will get a lot of value out of the community as the content, fireside chats, and conversations all revolve around what’s affecting you in and around your day-to-day.

It’s free to apply to and check out – only pay if you want to (though it’s a great value!). Apply to join here!

Drug Distributors continue Vertical Integration Strategy as Cencora, Cardinal make Big Bets

Deals among PE-backed physician practice management players and strategic buyers (drug distributors in this case) are heating up.

On November 6, Cencora bought Retina Consultants of America (RCA) for $4.6B (an 85% stake and $500M in incentive payments).

- RCA serves 300+ retina specialists in 23 states and sees 2 million patient visits annually.

- Interestingly RCA specializes in clinical trials in research, which Cencora is sure to have an invested (literally) interest in.

- Through eventually owning both OneOncology and RCA, Cencora will look to build out a more integrated management services organization (an MSO, as our industry so fondly loves its acronym) to house its services subsidiary.

Also this week, today Cardinal Health did its best to one-up its competitor by announcing it’s acquiring GI Alliance, valuing GI Alliance at $3.9B (a 71% stake).

- From the presser, GI Alliance (GIA) affiliates with 900+ physicians, and notably, its doctors hold a sizable amount of its equity so…potentially a big payday for its owner physicians as its PE sponsor owned around 15% of GIA. GIA has been highly acquisitive as most PE-backed players are, with a focus on the east coast and northeast regions.

- Other than that, GIA is large with 345 locations in 20 states, 135 ASCs, 165 hospital networks, and 95 infusion centers.

- GIA supports a complete continuum of gastroenterology care furnished by its member practices, with significant depth in anesthesiology, pathology, infusion, radiology and clinical research.

Cardinal Health also recently bought Integrated Oncology Network for $1.1B and is playing catch up with other distributors looking to acquire community oncology and related physician practice management assets to capture downstream specialty drug spend.

Bigger Picture: Why the massive acquisitions in ophthalmology and GI? At a high level, these specialties act as a wedge into accessing downstream specialty drug spend – and preserving / growing that specialty drug distribution margin for the McKesson’s, Cencora’s, and Cardinal Health’s of the world.

It’s vertical integration at its finest, as specialty drug spend will continue to grow and preserving this margin is top of mind. Owning the care delivery component unlocks and preserves this opportunity to double dip into both practice MSO earnings and specialty drug spend, and McKesson is well in front of other distributors (for now) with its US Oncology Network.

These moves are also a big win for private equity, as this deal now marks two exited investments sold to strategic players in the healthcare services world. The timing RIGHT after the election is pretty telling. While these discussions likely took place a while before the election, like I mentioned in my election summary, you should expect to see a continued thawing out of the M&A markets in a more business friendly political environment, and more sales to strategic players given they’re more likely to justify the frothier valuations on assets amalgamated (sorry, I saw the opportunity to use this word and I took it) during low interest rate environments.

If you want to understand the full picture of vertical integration in both oncology, the players involved, and why these distributors want to buy into these scaled physician practice management companies, I wrote a deep dive for my community here.

More on HATCo and Summa Health

HATCo signed a definitive agreement to acquire Summa Health with the following provisions:

- $485M purchase price (to be used to pay down debt, AKA HATCo is paying itself to reduce its new debt load); $350M in capital funding over 5 years; and $200M earmarked for ‘strategic and transformative investments and to drive innovation’ over 7 years. So total cash outlay over 7 years will be at minimum north of $1 billion.

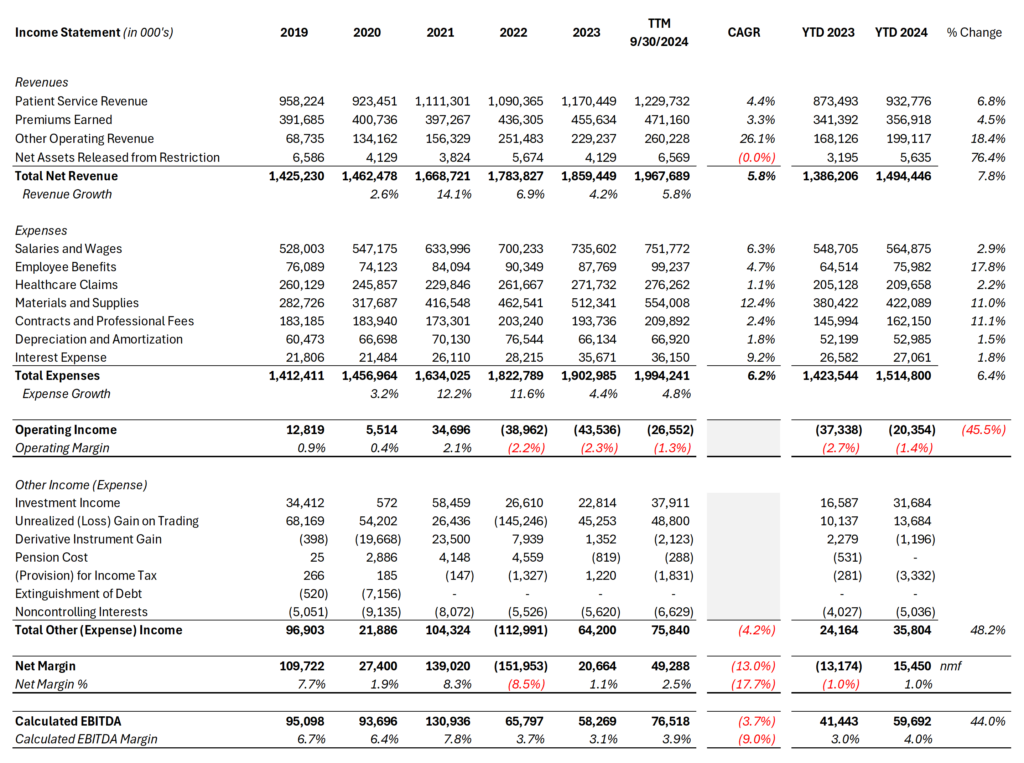

Here is Summa Health’s latest financials as of the trailing twelve month period ended September 30, 2024. Summa Health generated $1.97B in revenue and a calculated EBITDA figure of $76.5M (3.9%). The graphic below this one shows Summa Health’s common-sized (% of revenue) income statement and the nonprofit (well, now for-profit) system has bounced around -2% operating margin the past couple of years.

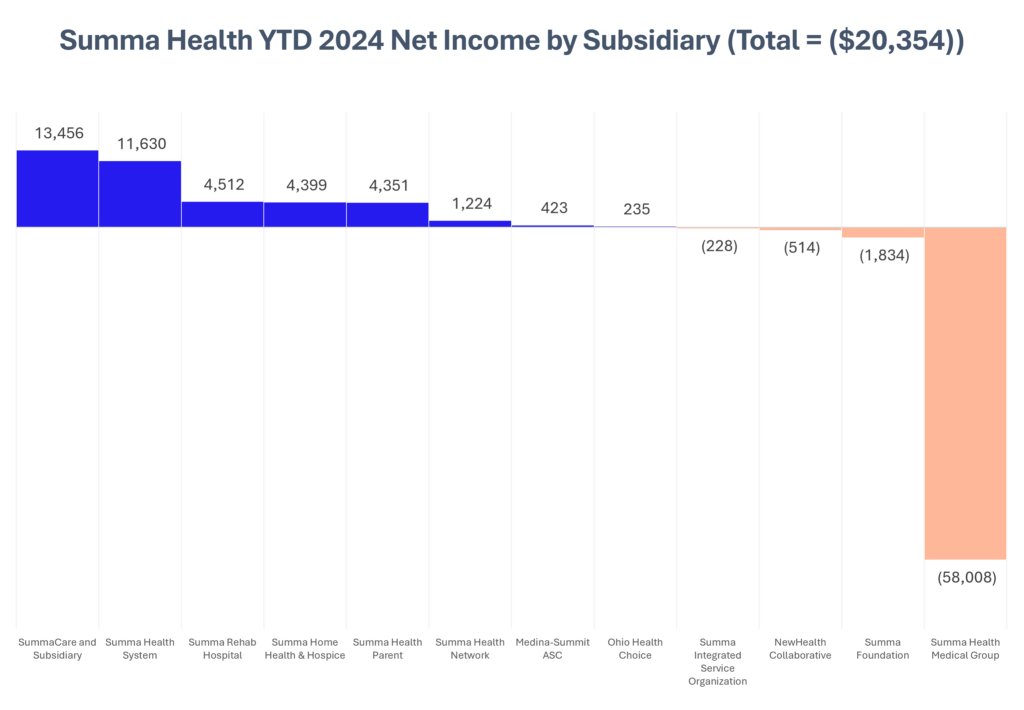

Not every nonprofit health system breaks down its profitability by segment, but pretty crazy to see hospital economics laid out in front of you: subsidized medical group losses to bring in downstream referrals and health plan member growth.

A while back Michael Stratton and I did a dive on HATCo and their potential strategy for Summa. You can read it here.

The Weekly Executive Summary

Notable moves, policies, and strategies from around healthcare.

Join the thousands of healthcare professionals who read Hospitalogy

Subscribe to get expert analysis on healthcare M&A, strategy, finance, and markets.

No spam. Unsubscribe any time.

Oracle announced a rollout of its next-generation EHR.

- Oracle is also rumored to be in the mix for Veradigm (previously known as Allscripts) acquisition along with McKesson and Thoma Bravo (after acquiring NextGen Healthcare last year)

CVS appoints former CEO of ChenMed and UnitedHealthcare exec Steve Nelson as head of Aetna.

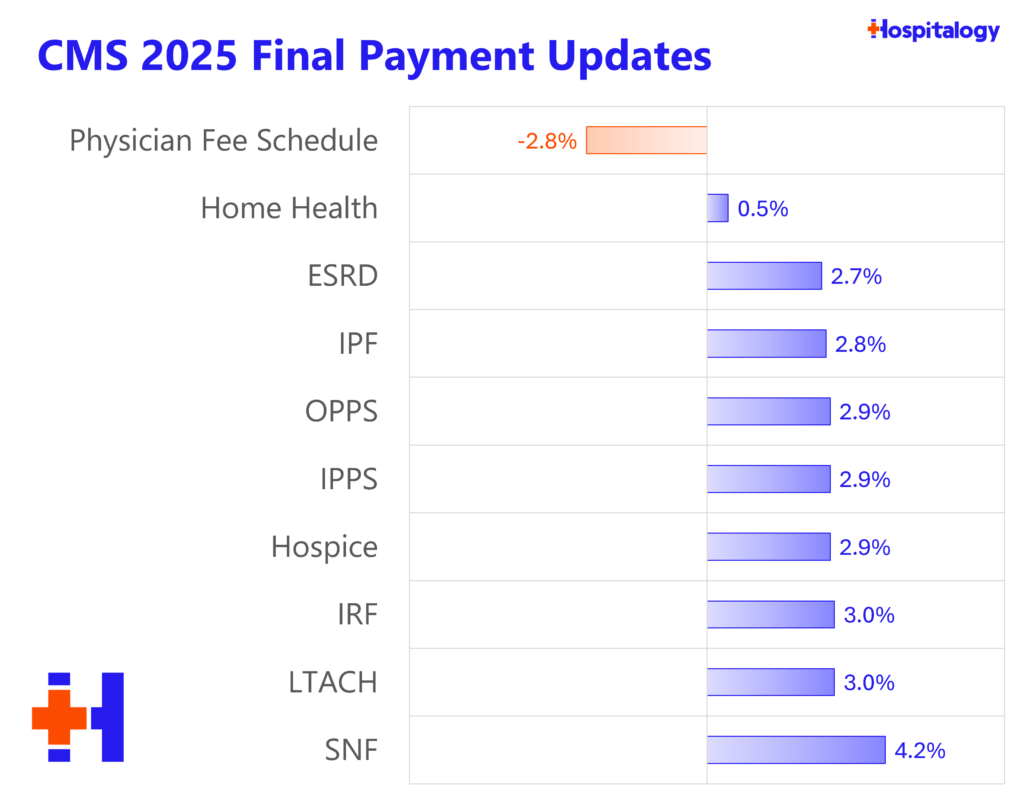

CMS is pushing out all of its final rules, announcing OPPS and others this month. As a whole, here are the final payment updates for fee for service in 2025:

- OPPS: +2.9%

- MPFS: -2.8% (as MedPAC and others call for Congress to link physician payment updates to inflation)

- IPPS: +2.9% (+3.0% for LTACH)

- ESRD: +2.7%; $6.6B to 7,700 dialysis facilities

- IRF: +3.0%

- IPF: +2.8%

- SNF: +4.2%

- Home Health: +0.5%

- Hospice: +2.9%

RadNet, a traditional diagnostic imaging player, is making huge moves into AI as it notches its first customer to DeepHealth OS, its AI-enabled platform for radiology.

Cigmana was officially put to rest this week…oh what could have been.

Veradigm sale rumors have been circulating all year and it looks like we’re closer to an end as McKesson, Oracle, and Thoma Bravo (bought NextGen Healthcare last year) are all rumored to be finalists to acquire the company formerly known as Allscripts.

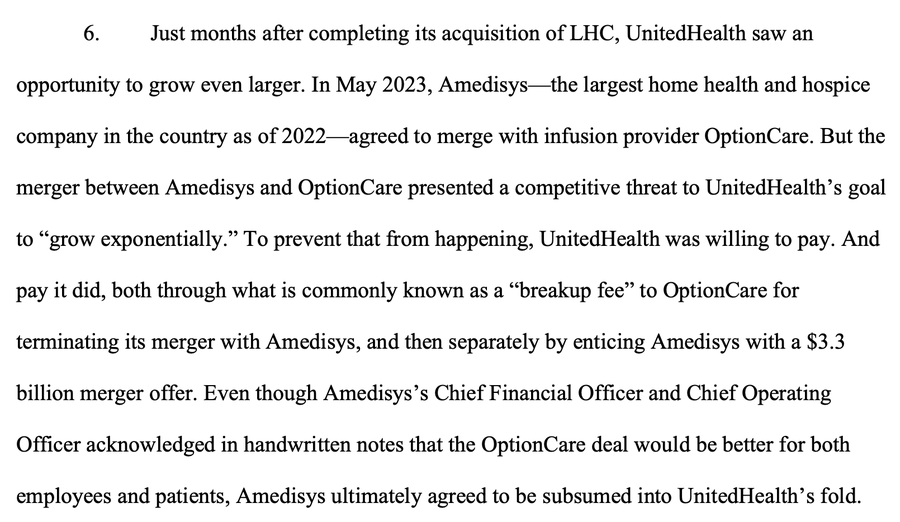

DOJ officially sues to block the Amedisys-Optum $3.3B deal…announced mid 2023. If successful, it’d set a huge precedent in proving out harm in vertical mergers between payors and providers of care – which to this point has proven impossible.

23AndMe cuts its workforce by 40% as its hellacious year continues.

Kaufman Hall published its monthly Hospital and quarterly Physician Flash Reports today:

Hospital Highlights:

- Acuity seems to be rising as length of stay and IP revenues are up

- September was a month of stability for hospitals

- While labor markets are still tight, other expenses (purchased services, supplies, etc.) were high in September

Physician Highlights:

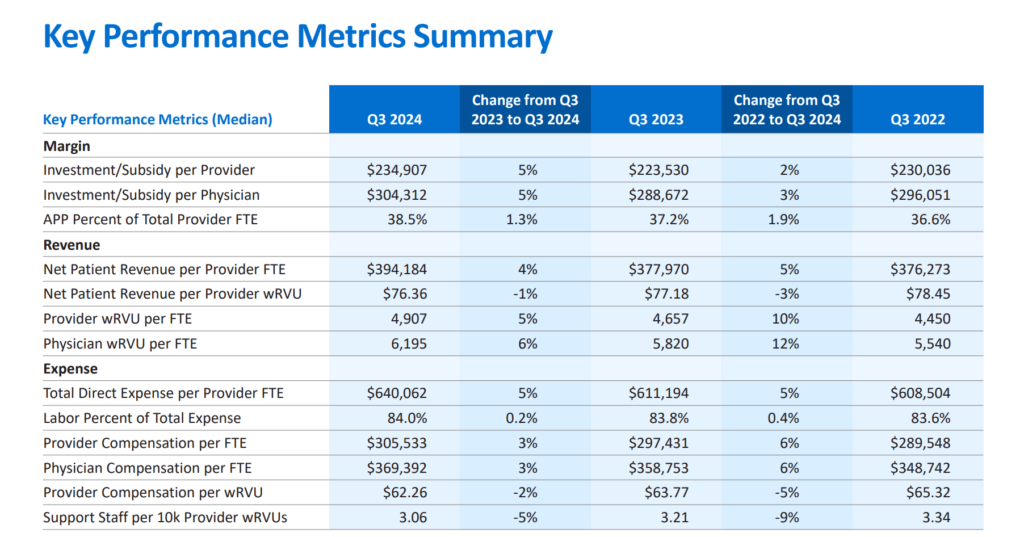

- Kaufman Hall is calling the physician employment subsidy model popular with hospitals BROKEN…pretty crazy stuff.

- Average subsidy per physician topped $300k for the first time ever

- Direct expense per provider FTE grew 5% year over year to $640k

- wRVUs per provider FTE grew 6% year over year

CMS published ACO REACH results on November 8. ‘In PY 2023, REACH ACOs generated approximately $1.643 billion in gross savings, representing approximately a 5.8% gross savings rate relative to the retrospective adjusted PY benchmarks. Net savings to CMS were $694.6 million (2.6%), and the net savings to ACOs were $948.4 million (3.4%) compared to model benchmarks. This is an increase from the $371.5 million in net savings to CMS and the $484.1 million in net savings to ACOs in PY 2022.’

Partnership Pulse

Collaborations, launches, and other tidbits to keep on your radar.

- Noom & Waltz Health: Noom and Waltz Health collaborate on a new GLP-1 management program.

- Talkspace & Wisdo Health: Talkspace joins forces with Wisdo Health to combat loneliness in older adults.

- ŌURA & Essence Healthcare: ŌURA partners with Essence Healthcare to elevate health for seniors through wearable technology.

- Providence & Compassus JV: Providence and Compassus form a joint venture to offer home health care services.

- HealthJoy & Mark Cuban’s Company: HealthJoy partners with Mark Cuban Cost Plus Drug Company to enhance access to affordable prescriptions.

- Arbital & Quartet Health: Arbital Health and Quartet Health team up to expand value-based care for severe mental illness.

- Cleveland Clinic & Amazon: Cleveland Clinic and Amazon One Medical collaborate to improve coordinated care access in Cleveland.

- Blue Shield & Salesforce: Blue Shield of California and Salesforce make prior authorization as simple as using a credit card.

- Walgreens Expands Services: Walgreens expands virtual healthcare services to 30 states, including lab testing and STD treatments.

- ShiftMed & Cottage Hospital: ShiftMed partners with Cottage Hospital to enhance workforce flexibility.

- Brook & Linus Health: Brook and Linus Health collaborate to provide cognitive care assessments.

- Medicare Savings Program: The Medicare Shared Savings Program continues to deliver meaningful savings and high-quality care.

- Ayble Health & Cleveland Clinic: Ayble Health and Cleveland Clinic partner to offer GI patients virtual behavioral health and nutrition counseling.

- AdventHealth & Walmart: AdventHealth opens a clinic inside a Walmart location in Corbin.

- Rula Health & Amazon: Rula Health teams with Amazon Health to expand virtual mental healthcare access.

- GE & RadNet Collaboration: GE HealthCare and RadNet collaborate on AI-powered imaging systems.

- Oracle & Meharry Medical College: Oracle partners with Meharry Medical College to establish an innovation hub and wellness center in Nashville.

Hospitalogy Top Reads & Resources

My favorite healthcare essays from the week

Some perspectives on fresh folks in Congress:

- Senate Democrats’ Health Focus: Incoming Senate Democrats set health priorities focused on expanding access and tackling healthcare costs.

- GOP Senators’ Health Stance: New GOP senators take a conservative approach on health policy, with an emphasis on cost reduction and regulatory reform.

Young vs. Older Doctors: Young doctors seek work-life balance, while older doctors argue it conflicts with traditional job expectations.

Henry Ford CFO on Ascension JV: Henry Ford Health’s CFO discusses the expanded joint venture with Ascension Michigan and its financial impact.