For all folks attending ViVE – Join me at the official Hospitalogy meetup with Navina. We’ll have a conversation around the state of value-based care today and then network with a great group of folks. Register here!

Today I’m diving into Tenet’s Q4 after they reported earnings earlier this week. Hopefully it’s helpful to you and your organizations given Tenet’s heavy focus on building out USPI – its ambulatory division.

Join my Hospitalogy Membership! If you’re a VP or Director working in strategy or corporate development at a hospital, health system or provider organization, you will get a lot of value out of my community as I purpose-build the content, fireside chats, and conversations for this group. Join for free today.

TL;DR

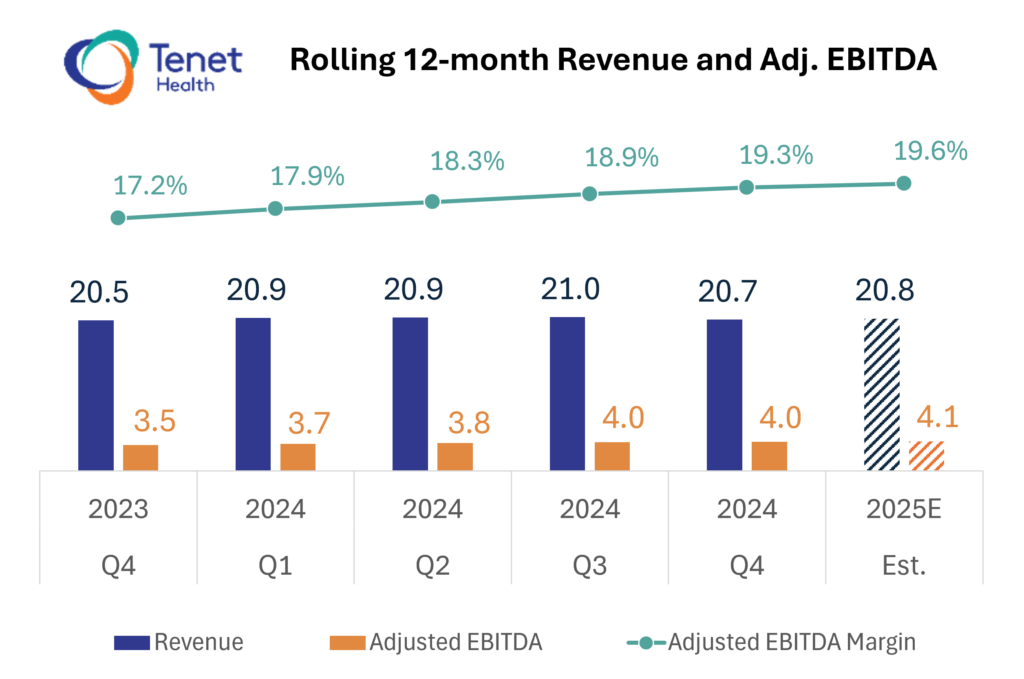

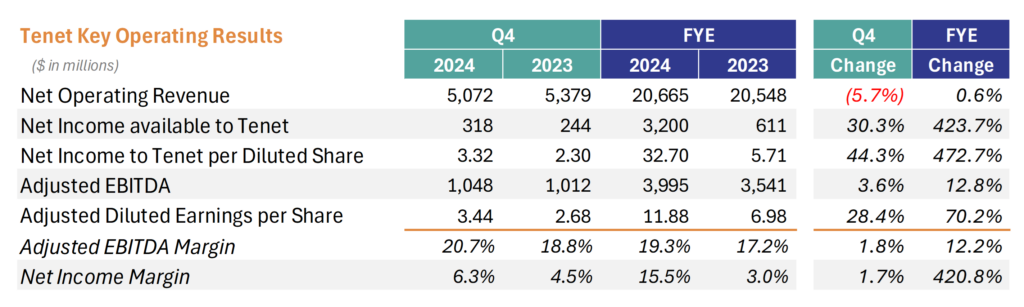

- Tenet had a strong 2024, exceeding expectations across all key metrics in a year of intense hospital divestiture and portfolio realignment around USPI and core markets. Tenet reported $20.7 billion in net operating revenues and $4.0 billion in adjusted EBITDA, a 13% YoY increase, with margin expansion of 200 bps to 19.3%.

- Margins expanded due to cost discipline, particularly in contract labor. Both hospital and ambulatory businesses saw strong volume and revenue per case growth, driven by higher acuity procedures and a favorable payor mix.

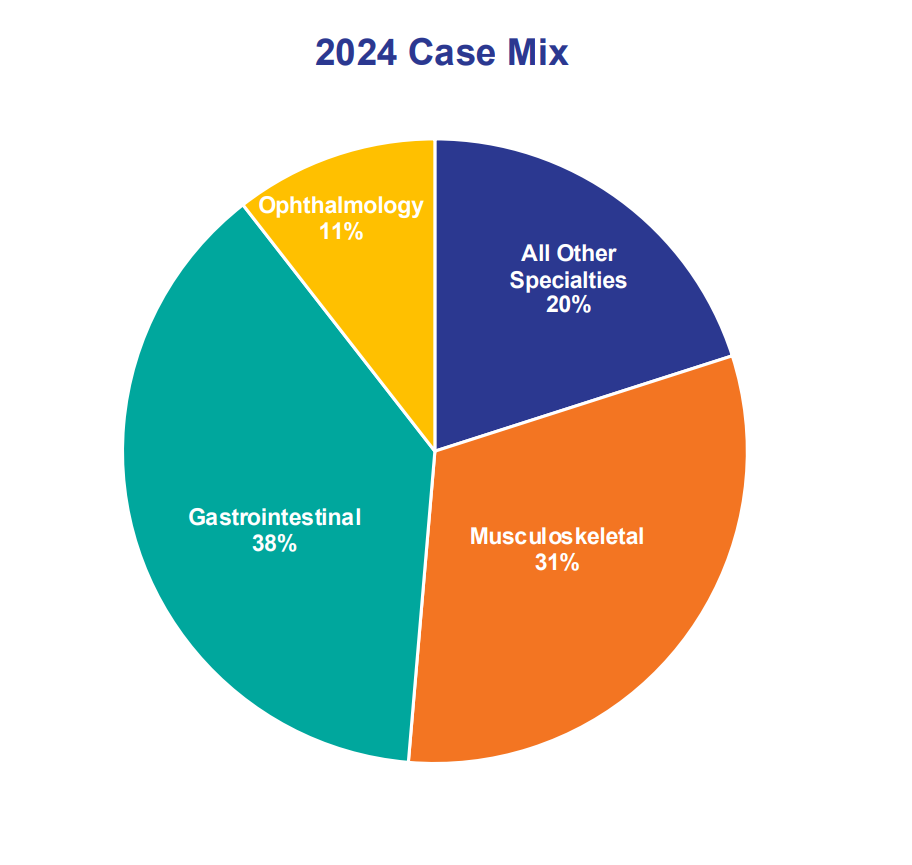

- USPI remains Tenet’s core growth engine, with high-acuity cases (total joints, orthopedics, cardiology) driving profitability. 10-12 de novo’s planned for 2025 and $250M+ allocated for M&A.

- Hospitals showed stability and the acute care segment will maintain a focus on efficiency – ‘Medicare profitability.’ Tenet sold 14 hospitals in 2024 for $5B in gross proceeds, and portfolio realignment was a big theme for them last year. They’ll focus on high acuity service lines in 2025.

- Commercial rates enterprise wide are increasing 3% to 5% for Tenet.

- Capital allocation remains balanced, prioritizing ASCs, strategic M&A, and share repurchases.

- Tenet feels insulated from any potential changes to site neutral payments given USPI’s ASC positioning (freestanding, not HOPD rates). Further, Tenet feels USPI isn’t impacted by any potential Medicaid cuts enacted by the Trump admin given their ASCs maintain a low Medicaid mix.

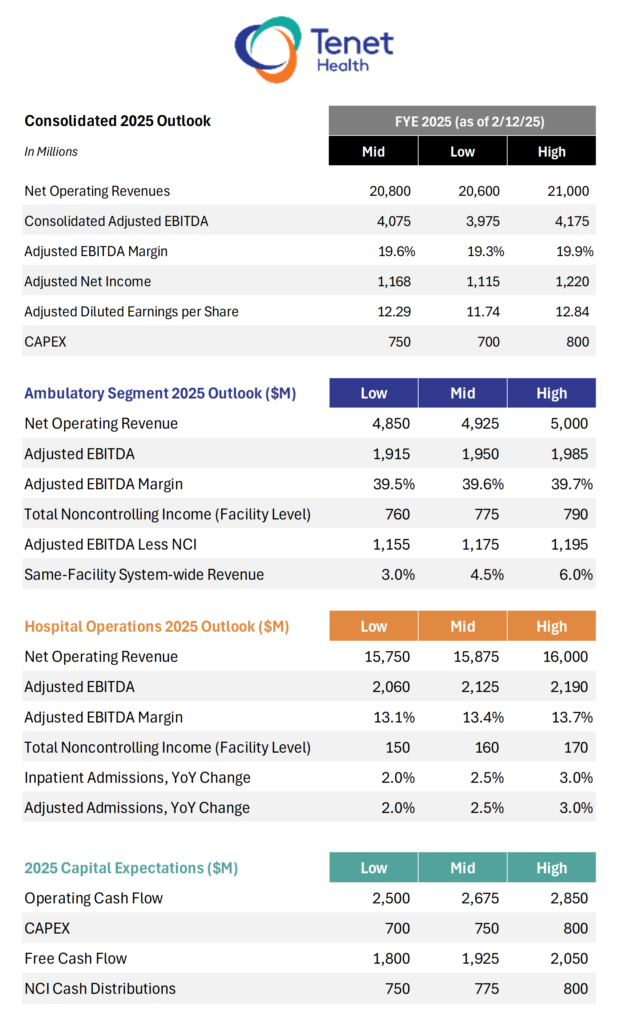

- In 2025 Tenet expects $20.6B – $21.0B in revenue and $3.975B – $4.175B in adjusted EBITDA, with hospital adjusted admissions growth of 2%-3% and USPI same-facility revenue growth of 3%-6%.

Volume & Utilization

- Hospital admissions up 4.7% YoY (same-store basis).

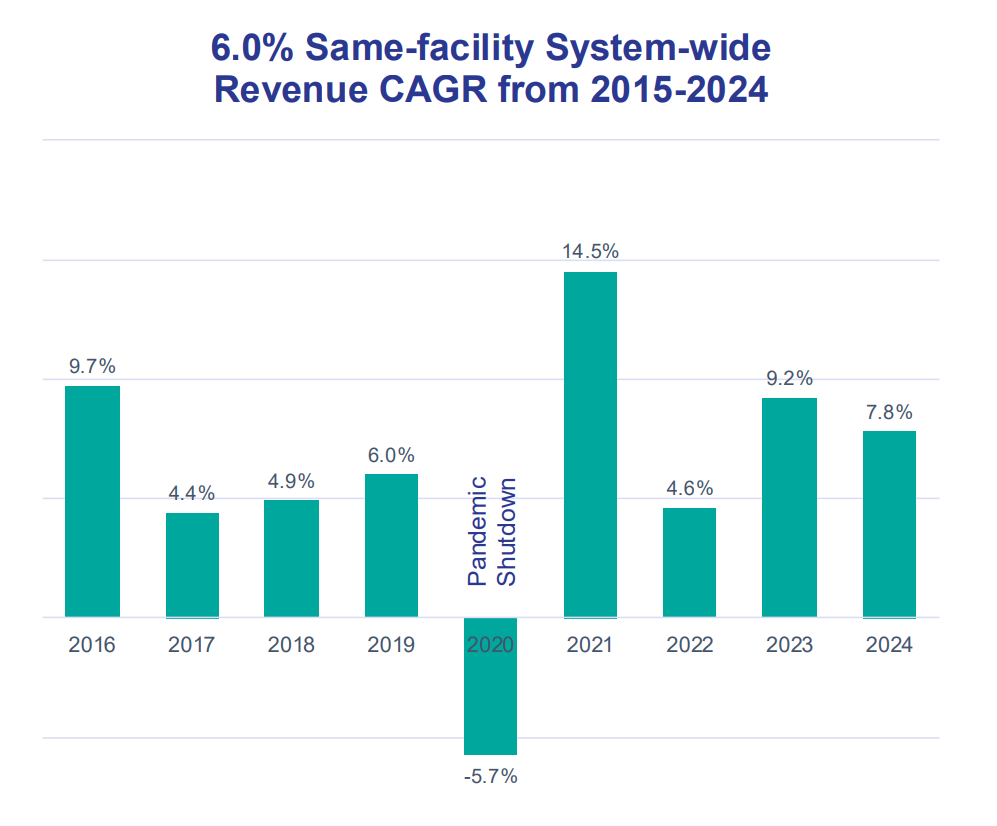

- USPI same-facility revenues up 7.8%, driven by high-acuity cases.

- ASC case mix involved more total joint cases (hip/knee, and the expansion into shoulders)

- USPI is reducing its exposure to high-volume, low reimbursement procedures or pushing those out to OBLs

- Interestingly Tenet management noted the continued opportunity in ortho and cardiology procedures, but emphasized that cardiology would be more of a slow burn given patient safety considerations, payor willingness and comfort, capex and equipment required, and physician partner availability vs. inpatient settings.

- Total joint replacements in ASCs up 19% YoY.

- Orthopedics (joint replacements), cardiology, and high-acuity outpatient procedures were key drivers of volume.

- USPI EBITDA growth of 17% YoY ($1.81B EBITDA, 40% margin).

- Hospital segment adjusted EBITDA: $2.185B (+9% YoY) despite hospital divestitures.

2. Revenue Growth & Payer Mix

- Same-store revenue per adjusted admission up 4.6% YoY.

- Managed care rate increases in the 3%-5% range, with some at the high end due to inflationary pressures.

- Exchange admissions continued to grow, though not at 40%-50% rates seen in 2024. ACA exchange volumes were a big tailwind in 2024. This dynamic will taper off in 2025, and unknowns around expanded subsidy expirations will call into question this payor mix improvement in 2026 and beyond.

- USPI pricing and payer mix improvements drove revenue per case growth.

- $1.16B generated in Medicaid supplemental payments; similar number expected for 2025.

3. Expenses & Margin Trends

- Adjusted EBITDA margin expanded ~200 bps YoY to 19.3%.

- Q4 margin at 20.7% (vs. 18.7% in Q4 2023).

- Contract labor expense down from 2.8% to 2.1% of salary, wages & benefits (SWB). Similarly to HCA, contract labor is at or near an all-time low. Hospitals seem to be really focusing efforts on not only recruitment, but retention.

- Total SWB expense as % of revenue dropped to 41.3% (from 43% a year ago).

- Medical supply costs rose to 18.3% of revenue (+100bps YoY), and Tenet management was quick to note during Q&A that this cost increase stemmed from higher acuity procedures and not supply chain issues (with tariffs and shortages being somewhat of a concern).

- Hospital adjusted EBITDA margin improved to 13.6% (+90bps YoY).

4. Capital Allocation & M&A

- $1.1B in cash flow generated

- Significant balance sheet deleveraging: Tenet generated $5B in gross proceeds from the sale of 14 hospitals over the course of 2024

- Tenet added nearly 70 ASCs to its portfolio in 2024 across M&A and de novo development. They were asked about…certain assets available on the market (Surgery Partners will likely be taken private by Bain). Management didn’t give much other than to say they’d take a ‘disciplined approach’ to M&A. But with the amount Tenet raised from hospital divestitures and with no debt due for a while…seems like a good a time as any to make another splash!

- Notably, Tenet declined to comment on working with any new or existing health system partners on the 10-12 de novo’s planned for 2025. This commentary likely speaks to the fact that health systems have more options than ever when it comes to partners in the space, and maybe they prefer flexibility in their own models and buildouts rather than USPI’s playbook.

- $250M annual budget for USPI M&A, 10-12 de novo ASCs expected in 2025.

- $672M in share repurchases during 2024, with plans to be ‘active repurchasers of our shares’ in 2025 ‘particularly at our current valuation multiples.’ = Tenet thinks they’re undervalued.

- $700M-$800M in capital expenditures planned for 2025.

- No major debt repayments due for a few years, maintaining 2.5x leverage ratio (3.2x when excluding noncontrolling interests).

5. 2025 Outlook & Guidance

- Total Topline Revenue: $20.6B – $21.0B (note this figure with 14 fewer hospitals).

- Tenet also expects a $35M revenue boost from the Tennessee Medicaid program.

- Adjusted EBITDA Range: $3.975B – $4.175B. On a normalized basis, Tenet expects adjusted EBITDA to grow 8.5% at USPI and 5.7% for hospital ops at the respective midpoints.

- Normalizations to 2025 guidance: $114M of adjusted EBITDA from divested facilities in 2024 will not reoccur, along with $74M in out-of-period supplemental Medicaid payments from Texas and Michigan.

- Growth: Guidance assumes the following volume growth metrics:

- Hospital adjusted admissions growth of 2%-3%.

- USPI same-facility revenue growth of 3%-6%

- $1.05B – $1.25B in post-NCI free cash flow expected, $700M to $800M in capital expenditures, and $750M – $800M in NCI distributions.

Key Management Quotes

- Site neutrality commentary: our ASCs operate with freestanding ASC rates which insulates that important part of our business from potential changes in site neutrality rules.

- On the outpatient migration and opportunity in cardiology procedures: the opportunity in a wide variety of cardiovascular procedures is there. I’ve always been clear that I think that, that opportunity will proceed more slowly than people anticipate because of important patient safety considerations and payer mix considerations and also the CapEx required to build a cardiac center is very different than building other types of ASCs given the equipment that you have to have in there. So the upfront investment for the physician partners and other things is much higher with potentially lower margin assets. And so from economic reasons and patient safety reasons, I think this market will evolve, but I think it will evolve slower than people like to think.

- On building de novo’s vs acquiring: consistent with our move into more high acuity ambulatory surgical work, de novos also represent a significant value shift in markets, right? Because usually what you’re doing is you’re building from the ground up, you’re moving things into a lower-cost setting it’s value for the consumers and payers in the markets to be focused on de novos in addition to everything else that we may be doing to grow the portfolio and expand the high acuity services. So that — it’s part of our value strategy.

- On de novo’s as more attractive, higher return on capital: The building costs are low. It’s a shorter time frame once the partnership is syndicated, there’s work upfront in syndicating the partnership that takes time, but that’s not a capital-intensive activity. Look, I think at the start of this, Pito pointed out one of the big changes in the organization around the generation of free cash flow. We also focus on measuring and following our overall return on invested capital within the organization. And obviously, the more we shift into this ambulatory segment, the more that gets better.

- On Tenet’s portfolio sales: This was an important year for Tenet as we transformed our portfolio businesses through the multiple — high multiple sales of 14 hospitals and related operations, generating $5 billion in gross proceeds and enabling significant balance sheet deleveraging.

- On capital allocation strategy: First, we’ll prioritize capital investments to grow USPI through M&A. Second, we expect to continue to invest in key hospital growth opportunities, including our focus on higher acuity service offerings. Third, we will evaluate opportunities to retire and/or refinance debt. And finally, we’ll have a balanced approach to share repurchases, depending on market conditions and other investment opportunities.

- On 2025 volume expectations: I mean the coverage environment looks good. The employment environment looks good. Demographics, both in terms of areas where, at least our portfolio is now positioned relative to where it was, has attractive demographics. And as we’ve noted, we’ve had opportunity to expand capacity and take on that capacity without excessive cost to do so, and we’re doing it in a deliberate way.

- On a continued focus on higher acuity cases: And part of what we’re signaling for ’25 is it’s definitely our plan to continue the shift to higher acuity procedures. I started to point out some of the factors driving that in terms of the revenue intensity of some of these cases, how efficiently we’re able to do them in our operating rooms now and generate margin, how we are scaling those programs into more centers. We now have robots in almost 150 of our programs around the country. This is the direction in which we’re taking the organization.

- On commercial rate escalators: we are continuing to see commercial rates increases in the 3% to 5% range and some of the contracts have been at or slightly above the high end of that range as respect to the inflationary pressures that you’ve mentioned. So I think the overall situation there is pretty consistent.

- On demand patterns in Tenet markets: the majority of that [breakdown between market growth and capacity] is the market level demand that we’re seeing versus the selective markets in which there’s still capacity that we’re bringing online. But it is a contributor, which is why I called it out before. We haven’t quantified what that looks like between the 2 numbers, but it is both and the majority of it is market-based demand across the Board. Some of this is also related to the service line choices which have highlighted, the things that we’re doing that are taking care of people with multiple chronic illnesses that continue to grow in prevalence are continuing to create more demand than perhaps certain types of lower acuity work, which may be coming out of hospitals in our environment.

- On cost savings initiatives and how centralization has played a key role: Our global business center has contributed significantly to our cost savings. If you think about the last 4, 5 years, the journey we’ve been on, of course, there’s obvious unit cost savings that you see on an immediate basis. But there’s a lot of cash flow that goes into actually restructuring and building and scaling that enterprise. And what might have started with kind of commodity work in certain areas of finance, or accounts receivable has expanded to 10, 12 different service lines that we are now running effectively in the global business center clinical areas, clinical analytics physician credentialing a variety of things. And that’s an important part of our efficiency agenda as we look forward as well.