Join my Hospitalogy Membership! If you’re a VP or Director working in strategy or corporate development at a hospital, health system or provider organization, you will get a lot of value out of my community as I purpose-build the content, fireside chats, and conversations for this group. Join for free today.

Today’s newsletter is a comprehensive overview of hospital Q4 and 2024 earnings season – what they’re thinking about, parallels and key themes from earnings calls, comparisons of how they performed in 2024, and 2025 outlook.

Finally, for any folks in Austin or at SXSW: don’t forget about my happy hour coming up this Tuesday in Austin with Lance Armstrong, Ben Freeberg, and more healthcare folks!

All are welcome – register here. Feel free to bring healthcare friends.

TL;DR – Public Hospital Operator Themes

- Volume & Utilization: All five reported stable-to-strong inpatient admission growth (2–4% range). Outpatient expansions—particularly ASC volumes—are a unifying theme, with Tenet’s USPI leading in specialty ASC expansions.

- Revenue & Payer Mix: Each benefited from commercial rate bumps (3–5%). Exchange enrollment continued pushing up commercial-like volumes, but caution remains on the policy front. Medicaid DPP or supplemental revenues created one-time lifts for CHS, Ardent, Tenet, HCA, and remain central to UHS’s programs.

- Expenses & Margin: Labor cost moderation helped all five expand or maintain margins. Physician fee inflation remains a watch item for CHS, Ardent, HCA. UHS had a notable malpractice reserve spike, while Tenet is seeing a big margin tailwind from its focus on ASCs.

- Capital Allocation: CHS, Tenet each sold multiple hospitals; Ardent and CHS plan more divestitures in 2025. HCA plans to invest heavily in ORGANIC bed expansions; Tenet to invest heavily into USPI growth.

- Guidance: Steady 2025 growth in volumes, revenue, and EBITDA across the board, with some inherent uncertainties around DPP approvals, potential site-neutral legislation, and exchange subsidy continuity.

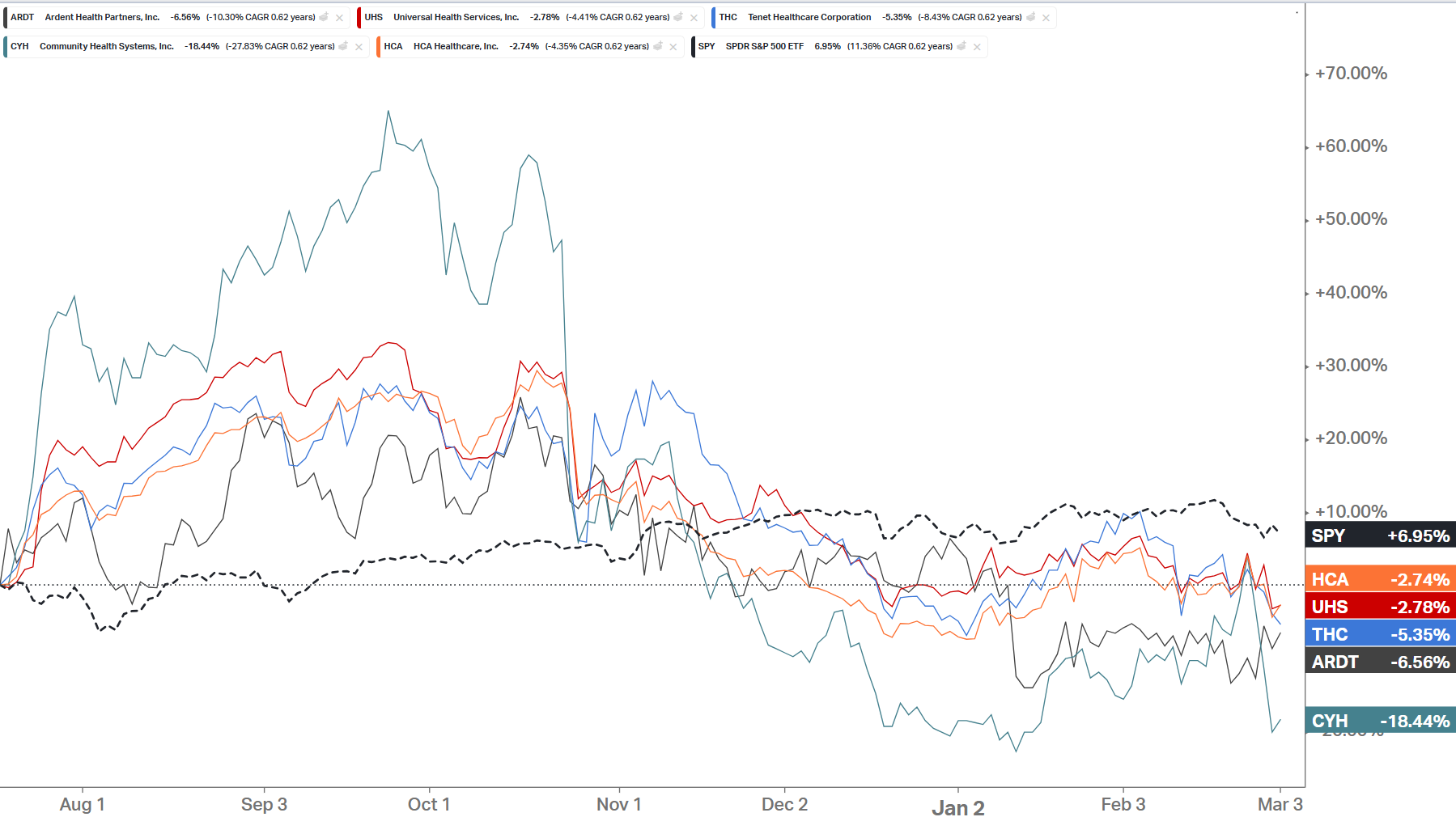

It’s clear we’re past peak hospital valuation which hit a high point in October. Keep in mind valuations are always forward looking:

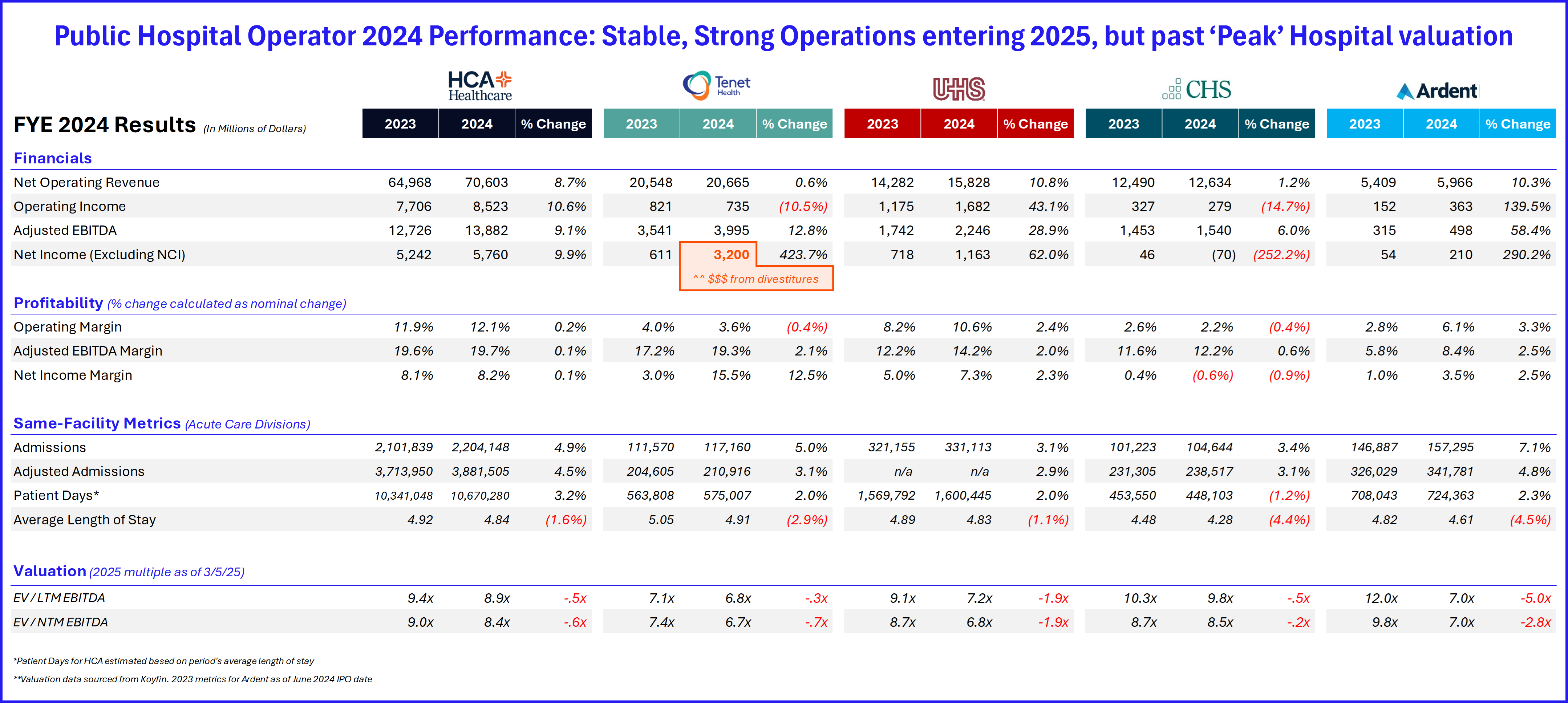

Key 2024 Comparative Results

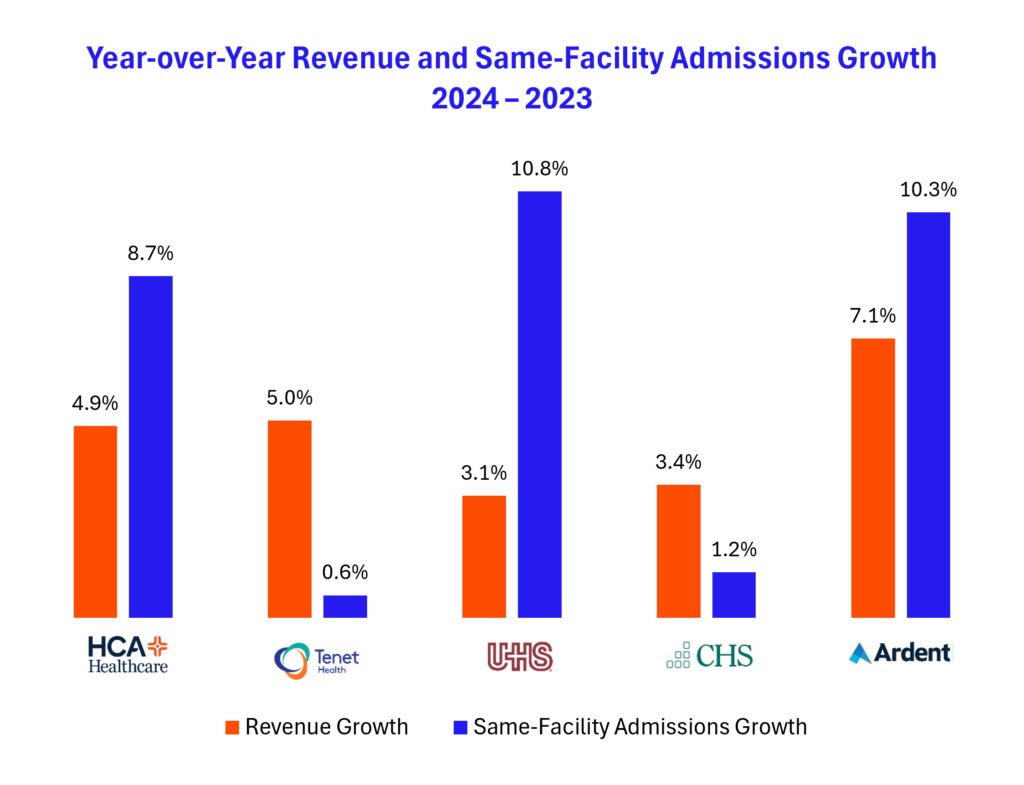

Across the board we saw strong performance for HCA, Tenet, UHS, and Ardent. CHS continues to trudge along behind the pack. Declining length of stay, strong same-store admissions, strong acuity, and rising exchange volumes in 2024 bolstered financial performance and contributed to nice recovery for most operators.

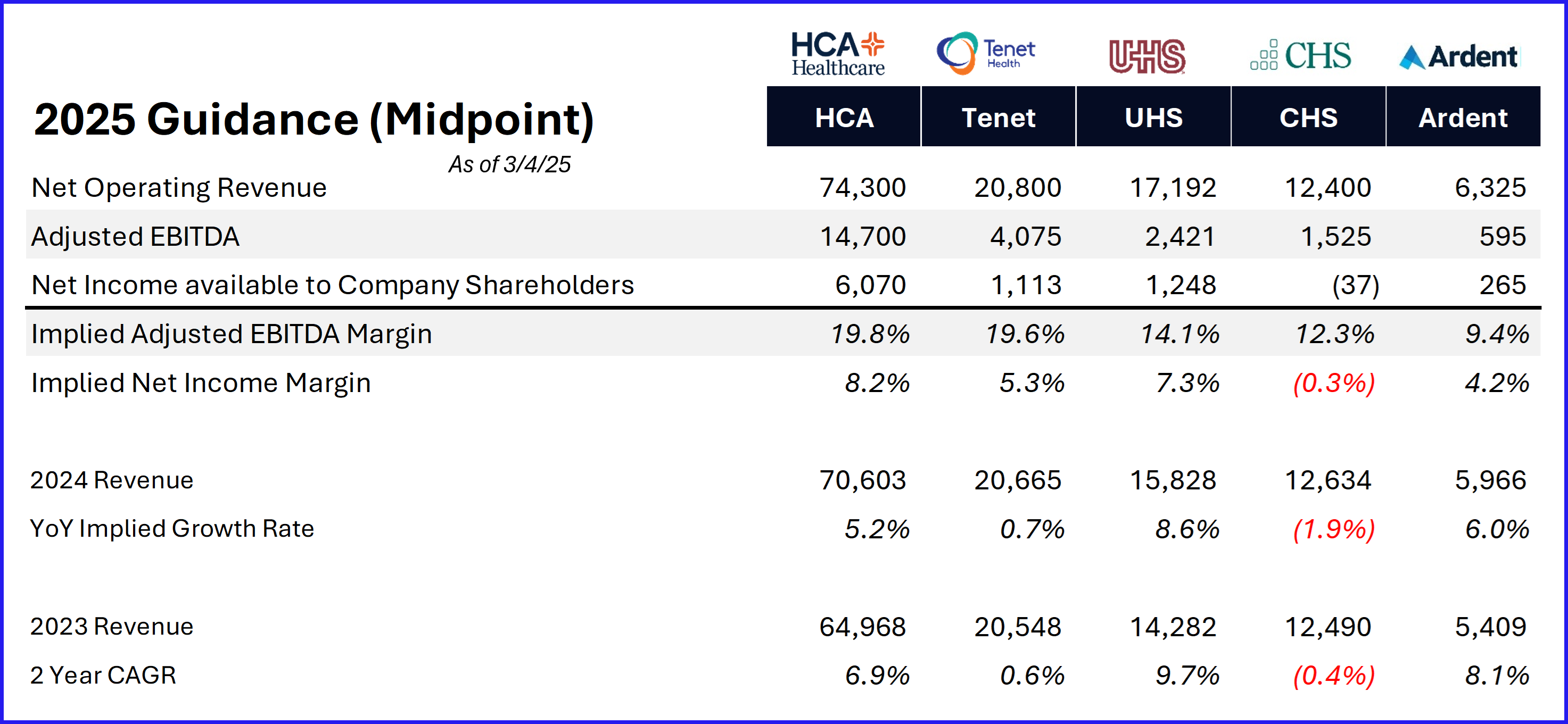

2025 Hospital Operators: Guidance Highlights

Major Themes Across All Five Public Hospital Operators

- Volume & Utilization

- Broadly Positive Inpatient Demand: Most operators reported growth in same-store admissions (ranging ~2–4%+). Elective procedures and higher-acuity surgical volumes (e.g., orthopedics, neurosurgery, cardiology) drove much of the incremental demand.

- Ambulatory & Outpatient Expansion: Every company highlighted strong or growing ASC volume. Ardent, CHS, Tenet, and HCA emphasized ambulatory expansions, while UHS likewise noted robust volumes in acute hospitals plus steady behavioral health admissions.

- Acuity & Mix: Several operators (Tenet, CHS, HCA) mentioned rising patient acuity or shifts toward higher-margin surgical lines. However, some noted mild softness in outpatient surgeries among lower-paying segments (e.g., Medicaid/uninsured).

- Revenue Growth & Payer Mix

- Mid-Single-Digit to Low-Double-Digit Growth: Revenue growth was generally in the 5–10% range, aided by rate increases, improving commercial mix, and in some cases state Medicaid supplemental payments.

- Medicaid Supplemental Programs: CHS, Ardent, Tenet, and HCA each recognized notable incremental revenue from various Directed Payment Programs (DPPs); UHS likewise benefits from state-specific programs. Many 2024 numbers included retroactive or catch-up payments. Looking ahead, these remain a swing factor in 2025 guidance.

- Commercial Rate Increases: Typical negotiated rate bumps ran ~3–5%. Higher inflation pressures over the past 18 months have led payers to offer slightly higher-than-historical increases.

- Expenses & Margin

- Generally Improving Labor Costs: All five reported a drop in premium (contract) labor spend from 2022–2023 peaks. Wage inflation is “stabilizing,” though still above pre-pandemic norms. In general contract labor is at a low point post-Covid among major public operators.

- Adjusted EBITDA Margin: Most showed margin improvement year over year. Tenet and Ardent reported some of the largest expansions (helped by divestitures and fast-growing ambulatory segments), CHS improved modestly, HCA held steady (+10 bps full year), UHS likewise saw expansions in both acute and behavioral.

- Physician Fees: Some (CHS, Ardent, HCA) noted continuing upward pressure on hospital-based physician fees in areas like anesthesia, radiology, or ER coverage—but at a moderating pace. Still a concern in today’s environment. Physician pay will continue to be a focal point

- Keep an eye on medical supplies cost with tariffs: Definitely potential here to see an uptick stemming from tariffs. Hospital operators today don’t seem too concerned and appear to have mitigation strategies in place for their procurement.

- Capital Allocation

- ASC & Outpatient Investments: Tenet (via USPI) remains the largest ASC operator; Ardent, CHS, HCA all investing in de novo outpatient sites, urgent care, and/or ASC expansions.

- Deleveraging & Divestitures: As I’ve mentioned before on Hospitalogy, and even among many nonprofit health systems, 2024 was a year of portfolio realignment. Both CHS and Tenet sold multiple hospitals in 2024; proceeds used to reduce debt. Ardent improved leverage to ~2.9×. CHS has plans for additional asset sales in 2025. UHS’s leverage remains comfortably below 3×; HCA uses robust free cash flow for share buybacks and expansions.

- Share Repurchases: Tenet and HCA are especially active (both in the $5–6B range in 2024). UHS also prioritizes buybacks (~$600M). CHS and Ardent have limited or no share repurchase activity, focusing on debt reduction.

- Outlook & Guidance (2025)

- Steady Volume Growth: Most project 2–3% (or slightly higher) inpatient admissions growth, along with continued expansions in ASC/outpatient.

- Revenue & EBITDA: Operators generally guide for mid-single to high-single-digit revenue growth, with incremental margin improvement from labor cost control and higher commercial rates. Many are excluding unapproved Medicaid DPP dollars from guidance, so actual results could exceed.

- Policy & Regulatory Watch: Potential site-neutral payment reforms, renewed or delayed Medicaid DPP approvals, and exchange subsidy uncertainties are common themes. No major immediate policy changes are fully baked in.

- Analyst Q&A – what are analysts thinking about?

- Top Questions: (1) the sustainability and magnitude of Medicaid DPP payments; (2) labor cost trajectory (contract labor, physician subsidies); (3) capital allocation priorities (ASCs vs. share buybacks vs. M&A); (4) volume guidance and service line mix shifts; (5) any impact from site-neutral proposals or future exchange subsidy changes.

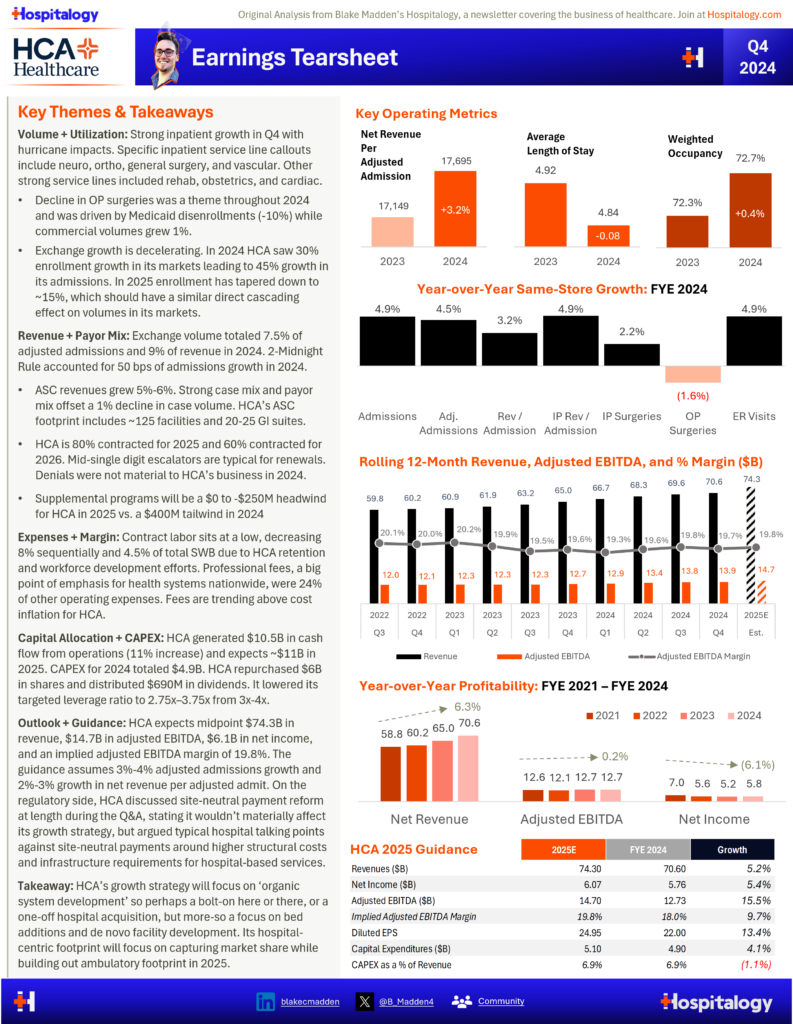

HCA Healthcare

A. Volume & Utilization

- Inpatient: +3% admissions in Q4. Inpatient surgeries +2.8%.

- Outpatient Surgeries: -1.3% volume, but net outpatient surgical revenue up due to favorable payer mix.

- ER Visits: +2.4%.

- Acuity: Trending higher thanks to specialized procedures (neuro, ortho, vascular).

B. Revenue Growth & Payer Mix

- Same-Facility Revenue: ~+6% in Q4. Net revenue per equivalent admission +2.9%.

- Commercial & MA: +9.2% admissions yoy.

- Exchange: 7.5% of admissions, 9% of revenue. Slowing growth vs. 2024.

- Medicaid Supplemental: $400M incremental benefit in 2024; expect flat to $250M decline in 2025.

C. Expenses & Margin

- Adjusted EBITDA Margin: Full-year up ~10 bps vs. 2023; Q4 margin -60 bps yoy on hurricane disruptions.

- Labor: Contract labor ~4.5–4.6% of total salaries/wages, down yoy. Wage inflation stable, improved retention.

- Professional Fees: ~24% of other OpEx. Radiology subsidies remain a smaller but persistent cost factor.

D. Capital Allocation

- Cash Flow: $10.5B in OCF (+11%).

- CapEx: $4.9B in 2024, guiding $5.0–$5.2B in 2025.

- Share Repurchases: $6B in 2024, new $10B authorization for 2025.

- Dividend: Increased from $0.66 to $0.72 quarterly.

- M&A: Mostly small “tuck-in” deals; an example is a hospital in New Hampshire.

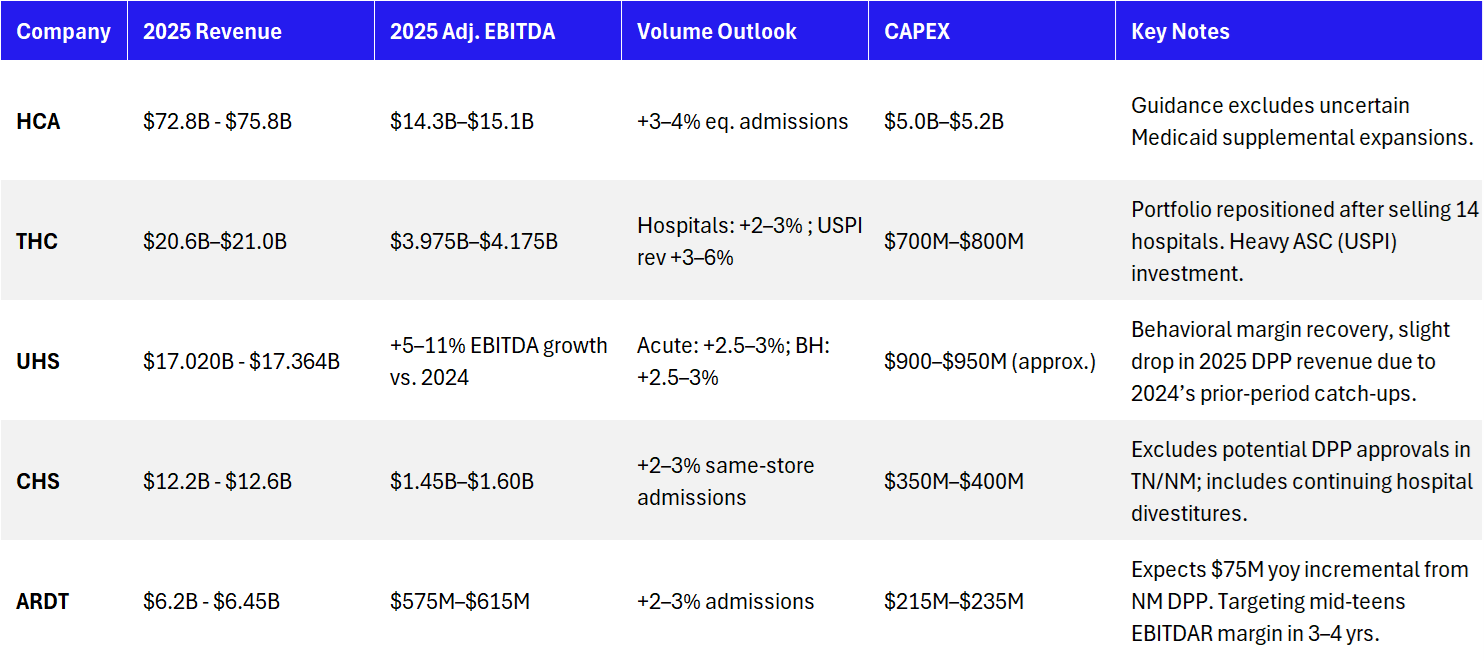

E. Outlook & Guidance (2025)

- Revenue: $72.8B–$75.8B

- Adjusted EBITDA: $14.3B–$15.1B

- Net Income: $5.85B–$6.29B

- Volume Growth: +3–4% eq. admissions.

- Margins: Expect stable yoy margin, with some risk from $0–$250M lower Medicaid supplemental.

- CapEx: $5.0–$5.2B, about half growth, half maintenance.

F. Analyst Q&A (HCA) – Tabular Summary

| Analyst | Question | Management Response | Key Details |

|---|---|---|---|

| Deutsche Bank (Pito Chickering) | Medicaid supplemental: Q4 vs. 2025 bridge. | $400M net boost in 2024; 2025 could be flat to -$250M yoy. | DPP approvals (TN, others) pending. |

| UBS (A.J. Rice) | Denials, commercial contracting for 2025–2026. | ~80% 2025 rates locked; stable denial environment. Pricing at high end of 3–5% range. | No major shift in denial patterns. |

| Leerink (Whit Mayo) | Operating initiatives: ER throughput, AI, LoS. | Emphasizing care coordination, cost mgmt. AI in early phases for both clinical and admin tasks. | HCA invests heavily in internal pipeline for nursing. |

| RBC (Ben Hendrix) | Exchange enrollment & possible subsidy changes. | 7.5% eq. admissions, 9% revenue. Slowing enrollment growth in 2025. HCA advocates to preserve subsidies. | Potential policy risk post-2025. |

| BofA (Joanna Gajuk) | Professional fees, hurricane repairs in Q4. | Radiology is a smaller portion. Hurricanes shaved 20–40 bps off Q4 volume. Little carryover into 2025. | Minimal net 2025 hurricane effect. |

| KeyBanc (Matt Gillmor) | Q1 2025 seasonality or unusual items. | Normal seasonality, no big quirks. Partial TN approval might come in Q2. | They exclude unapproved TN funds from guidance. |

| Wolfe (Justin Lake) | Site-neutral proposals? | HCA opposes. Hard to quantify without legislative specifics. No change in outpatient expansion plans. | Watching Congress closely. |

| Stephens (Scott Fidel) | Tariffs, supply chain cost. | ~70% supply locked in for 2025. No major tariff exposure so far. Immigration policy also uncertain. | Using HealthTrust GPO. |

| Nephron (Josh Raskin) | Labor trends, nurse supply. | Contract labor down to ~4.5%, wage inflation stable. HCA invests in nurse pipelines, seeing retention gains. | 2-midnight rule benefit tapered off in 2024. |

Tenet Healthcare

A. Volume & Utilization

- Hospital Admissions: +4.7% same-store.

- USPI (ASC) Volumes: +7.8% revenue growth at same-facilities, with robust expansion in total joints, orthopedics, and cardiology.

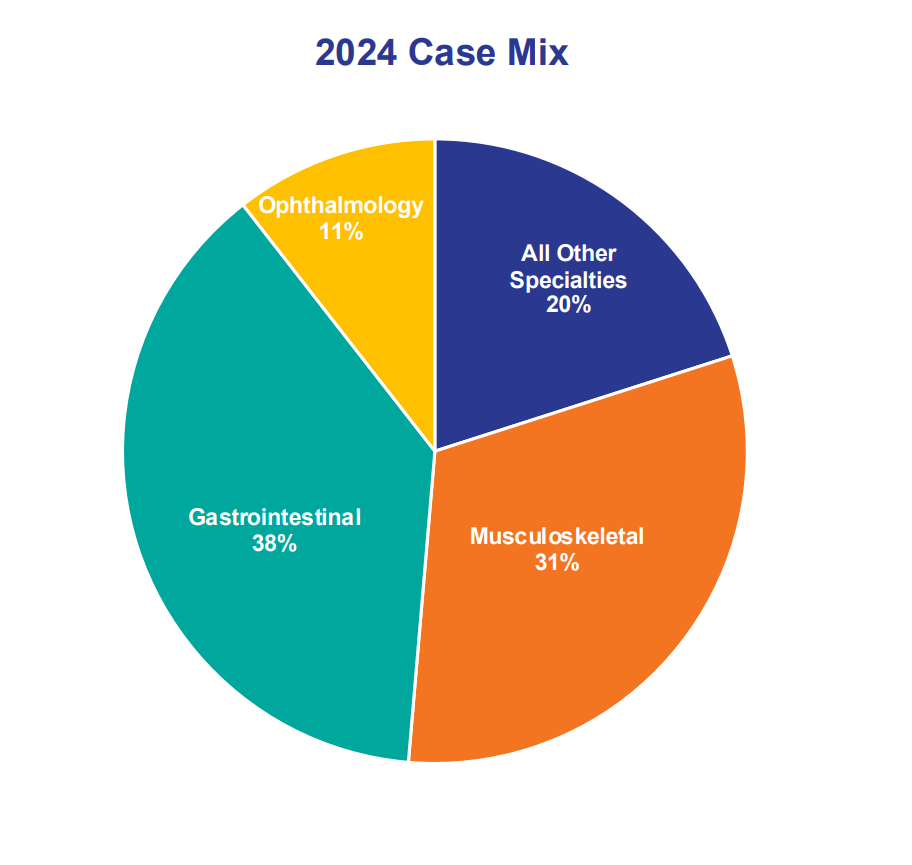

- Case Mix: More high-acuity outpatient procedures; ~19% growth in total joints at ASCs.

B. Revenue Growth & Payer Mix

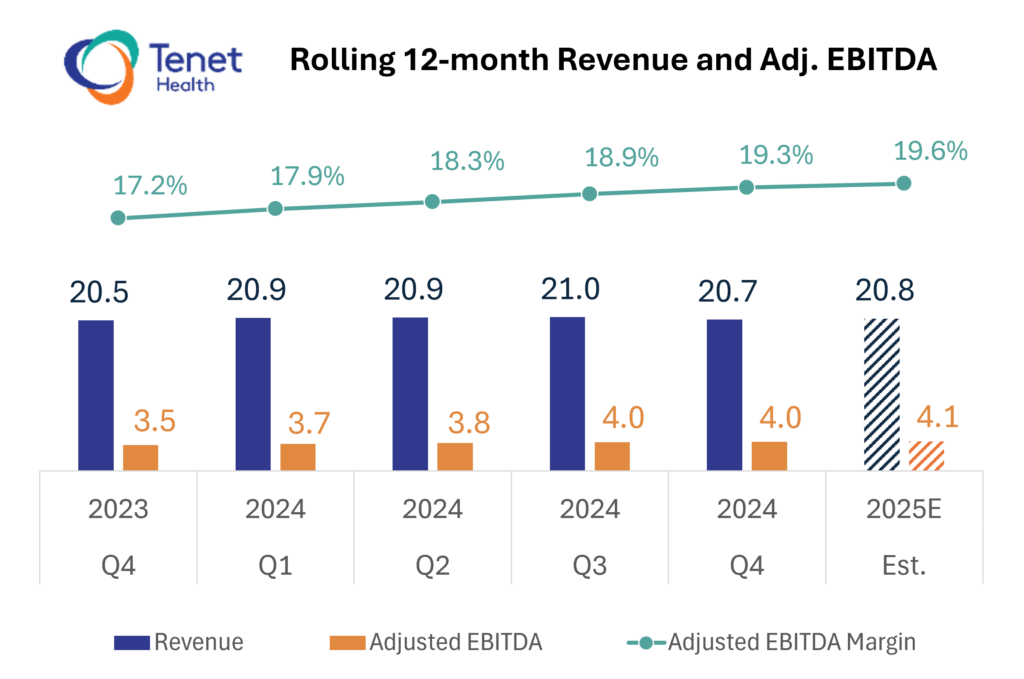

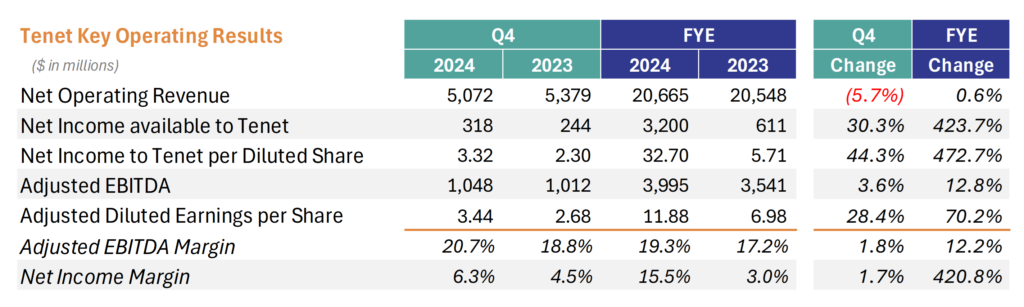

- Net Operating Revenue: $20.7B in 2024.

- Same-store hospital revenue per adjusted admission: +4.6%.

- Managed Care Rates: 3–5% range.

- Medicaid Supplemental: $1.16B recognized, expecting a similar scale in 2025.

C. Expenses & Margin

- Adjusted EBITDA Margin: 19.3% for full-year 2024 (+200 bps). Q4 at 20.7%.

- Hospital Segment: 13.6% margin (+90 bps).

- USPI Segment: $1.81B EBITDA (+17%), 40% margin.

- Labor: Contract labor down to ~2.1% of SWB; wage inflation stable.

D. Capital Allocation

- Divestitures: Sold 14 hospitals for ~$5B proceeds in 2024, significantly reshaping the portfolio.

- ASC Focus: Added ~70 ASCs in 2024 via M&A + de novo; $250M budget for more in 2025.

- Share Repurchases: $672M in 2024, planning more in 2025.

- CapEx: $700–$800M for 2025.

- Leverage: ~2.5× net debt/EBITDA, no major debt maturities soon.

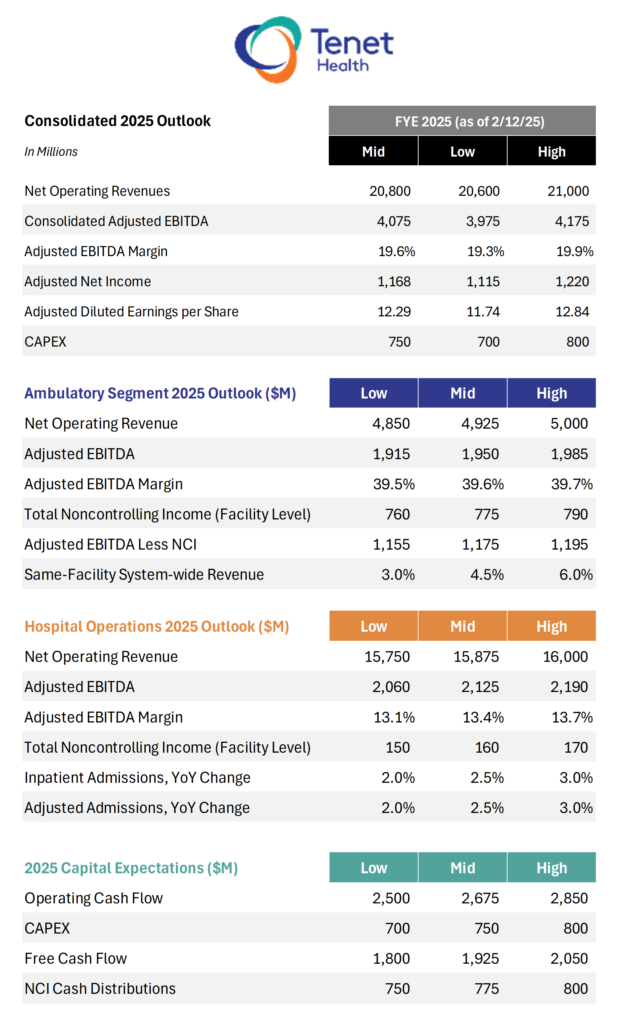

E. Outlook & Guidance (2025)

- Revenue: $20.6B–$21.0B (fewer hospitals post-divestiture).

- Adjusted EBITDA: $3.975B–$4.175B.

- Hospital Volumes: +2–3% adjusted admissions.

- USPI Same-Facility Revenue Growth: +3–6%.

- EBITDA Growth: 8.5% at USPI, ~5.7% in hospital segment (at midpoints).

F. Analyst Q&A (Tenet) – Tabular Summary

| Analyst | Question | Management Response | Key Nuances |

|---|---|---|---|

| 1. Volume vs. Pricing | Drivers of 7.8% USPI revenue growth? | Mix shift to higher-acuity (ortho, cardio) plus stable commercial rates. Lower-volume, high-reimb procedures. | Cardiovascular in ASCs is a slow but growing opportunity. |

| 2. Hospital Divestitures | How do proceeds reshape balance sheet or M&A capacity? | $5B from 14 hospitals. Used for deleveraging + fueling ASC expansions. Remainder for share buybacks. | Portfolio now more focused on key markets. |

| 3. Commercial rate environment | 3–5% typical? | Yes, inflation drove payers to accept somewhat higher than historical. | Still negotiating multi-year deals. |

| 4. Site-neutral proposals | Impact on USPI? | Tenet is generally “favorably positioned,” as USPI is mostly freestanding ASCs. No material near-term threat. | HOPDs, not part of USPI. |

| 5. AI or technology | Where are you investing? | OR scheduling, administrative tasks, supply chain. But no big singular AI product announcements. | Efficiency gains + cost mgmt. |

| 6. 2025 EBITDA guidance | Reconciliation from 2024? | ~ $114M from divested hospitals + $74M out-of-period Medicaid payments in 2024 not recurring. USPI continues ~8–9% growth yoy. | Normalizing after hospital sales. |

| 7. M&A | Big deals rumored (Surgery Partners)? | Disciplined approach. Not ruling out strategic transactions, but no definitive plan to chase large acquisitions. | Focus is on tucking in new geographies, de novo ASCs. |

| 8. Share repurchases | Pace in 2025? | “Active repurchasers,” especially at current multiples. No formal target but strong free cash flow to support. | Balancing with capital for USPI expansion. |

Universal Health Services (UHS)

A. Volume & Utilization

- Acute Care: +2.2% same-facility adjusted admissions in Q4.

- Behavioral Health: Steady demand + high-single-digit revenue growth, though slight year-end softness in child/adolescent.

- New Hospitals: West Henderson (Las Vegas) opened, Cedar Hill (D.C.) opening soon—some potential cannibalization but net volume growth.

B. Revenue Growth & Payer Mix

- Acute: +8.7% same-facility net revenue in Q4, driven by 2.2% volume + ~5% price.

- Behavioral: ~11% same-facility revenue growth in Q4. Pricing robust at 3–4% or more.

- Medicaid DPP: ~$1.016B in 2024 net of taxes; partial was catch-up from prior periods, so 2025 might see a slight net decline.

C. Expenses & Margin

- Labor Costs: Premium pay down from $153M peak (Q1’22) to ~$60M in Q4’24.

- Malpractice Reserve: $79M above plan for 2024. Management sees possible normalization in 2025.

- EBITDA & Margins: Mid-single-digit overall EBITDA growth in 2025 guidance. Acute margins improved ~13% in 2024, BH margins returning to pre-COVID levels.

D. Capital Allocation

- CapEx: $944M in 2024; building new hospitals, EHR expansions in BH.

- Share Buybacks: ~$599M in 2024, plan to continue $600–$800M range.

- No Large M&A: Focusing on expansions (acute + BH) and moderate outpatient growth.

E. Outlook & Guidance (2025)

- EBITDA: +5–11% growth vs. 2024, partly driven by lower malpractice costs.

- Behavioral: 2.5–3% volume growth, ~3–4% price = mid-to-high single-digit revenue growth.

- Acute: 2.5–3% adjusted admission growth, ~2.5–3% price.

- Supplemental Programs: Slight net decline from 2024’s prior-period catch-up.

- Margin: Additional expansions expected in both acute & BH segments.

F. Analyst Q&A (UHS) – Tabular Summary

| Analyst Topic | Context | Management Response |

|---|---|---|

| Various (Steve Filton, CFO, responding) | 2025 EBITDA drivers vs. 2024, large range | Core volume + stable pricing + lower premium labor + smaller malpractice accrual. Range widened due to potential DPP variance. |

| Asked about Behavioral volumes | Late Dec softness in adolescent. Rebounded in Jan. Expect 2.5–3% full-year BH volume growth. | Holiday effect + weather lumps. |

| Site-neutral or DPP policy risk? | Low near-term risk. States rely heavily on these programs. Bipartisan support. | Watchful but not alarmed. |

| Share Repurchases | $600–$800M typical. Comfortable at ~2.8–3.0× net debt/EBITDA. Will consider incremental leverage if needed. | They have a history of consistent buybacks. |

| Malpractice vs. future reserves | Booked $79M more in 2024. Hopes no further big reserve hikes for 2025. Actuarial approach. | This is a big “variable.” |

| CapEx & new hospitals | ~ $900–$950M range. West Henderson (Vegas) + Cedar Hill (D.C.) to be EBITDA-positive in 2025. | Some local cannibalization risk. |

Community Health Systems (CHS)

TL;DR – Main Themes

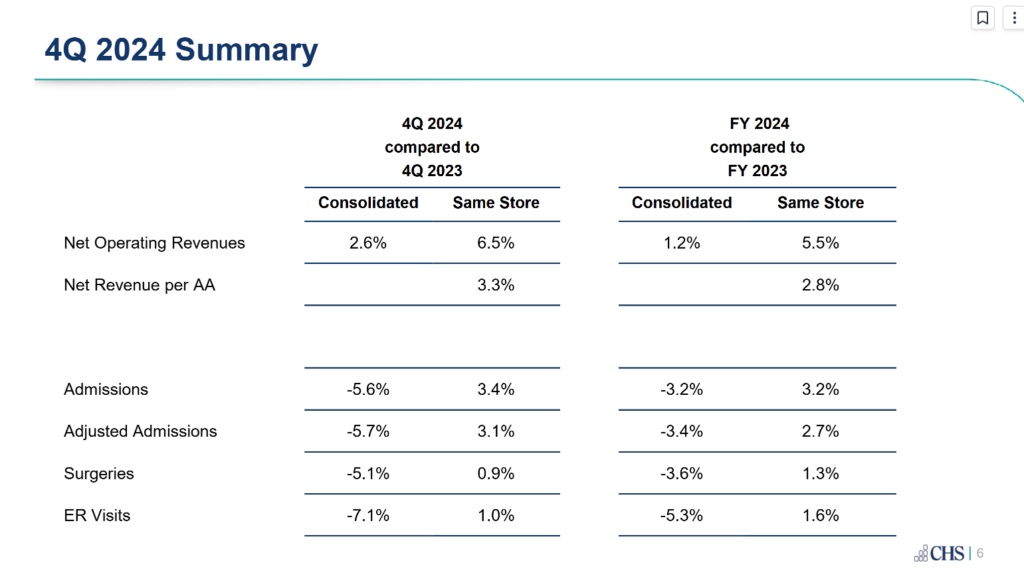

- Volume Growth & Strong Demand: CHS saw record same-store volume levels, with same-store admissions up 3.2%, adjusted admissions up 2.7%, and same-store surgeries up 1.3% for the full year.

- ASC & Outpatient Growth: CHS continues expanding ambulatory services, with same-store ASC cases up 14% YoY and urgent care expansion via acquisitions.

- Expense Management & Margin Expansion: Contract labor costs down 36% YoY, supplies expense down 50 bps. However, medical specialist fees surged 12% YoY, impacting margins.

- Portfolio Optimization & Debt Reduction: Announced divestitures expected to generate $1B+ in proceeds, supporting deleveraging from 7.9x to 7.4x net debt/EBITDA.

- Medicaid Supplemental Payments & Regulatory Risks: CHS benefited from $40M in unanticipated Medicaid DPP funds in Q4, but guidance excludes potential 2025 DPP approval for Tennessee & New Mexico.

- Capital Allocation Strategy: $350M-$400M in CapEx for 2025, focusing on hospital expansions, ASC growth, and freestanding EDs.

- 2025 Guidance & Growth Expectations: $12.2B-$12.6B revenue, $1.450B-$1.600B adjusted EBITDA, and $600M-$700M operating cash flow, with mid-single-digit revenue growth expected.

A. Volume & Utilization

- Same-store admissions: +3.2% YoY.

- Same-store adjusted admissions: +2.7% YoY.

- Same-store surgeries: +1.3% YoY.

- Same-store ASC cases: +14% YoY.

- Freestanding ED expansion: Now at 19 locations. 10 new urgent care clinics in Tucson, AZ and 2 new freestanding EDs.

- Acuity: Continued moderate rise, especially in cardiac and surgical lines.

- Other Factors: Some modest hurricane disruptions in certain Florida markets.

B. Revenue Growth & Payer Mix

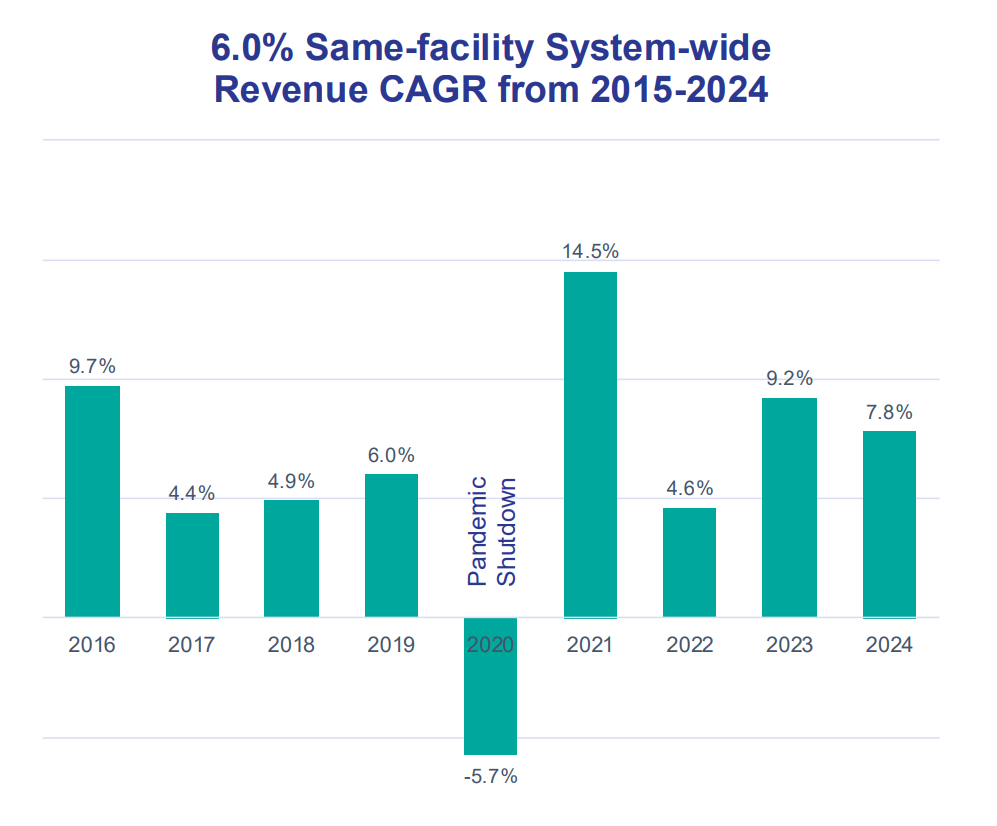

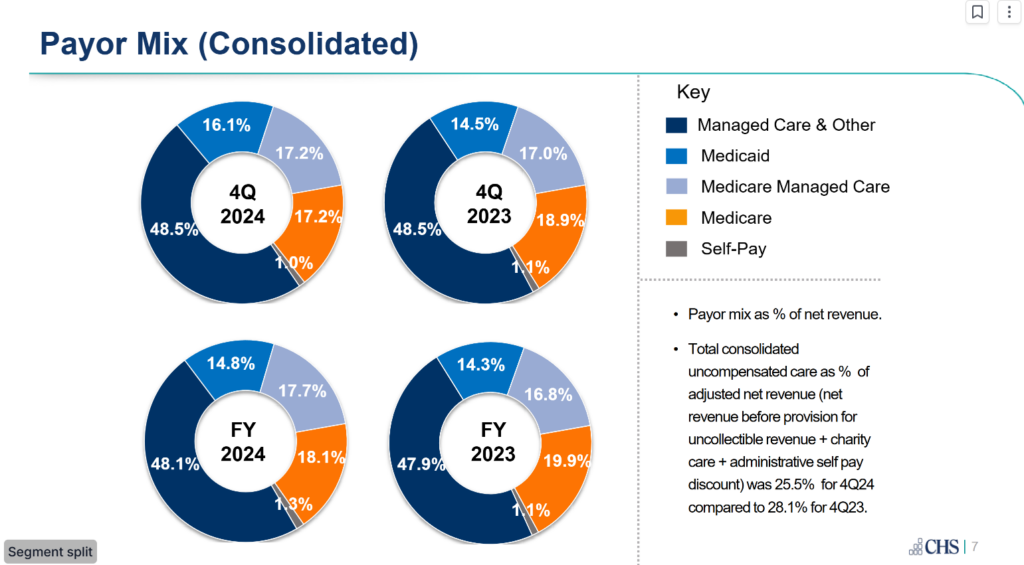

- Same-store net revenue: +6.5% in Q4, ~+5.5% full-year 2024.

- Net revenue per adjusted admission: +3.3% in Q4, reflecting rate growth and Medicaid supplemental funds (~$40M in Q4 from DPP).

- Payer mix: Some improvement in commercial proportion, plus higher exchange volumes.

- Medicaid DPP: Unanticipated $40M recognized Q4 2024 from NM. Future approvals in Tennessee remain outside guidance.

- Same-store net revenue up 6.5% YoY in Q4.

- Net revenue per adjusted admission up 3.3%, driven by rate growth and Medicaid supplemental payments.

- Mid-single-digit revenue growth expected in 2025.

C. Expenses & Margin

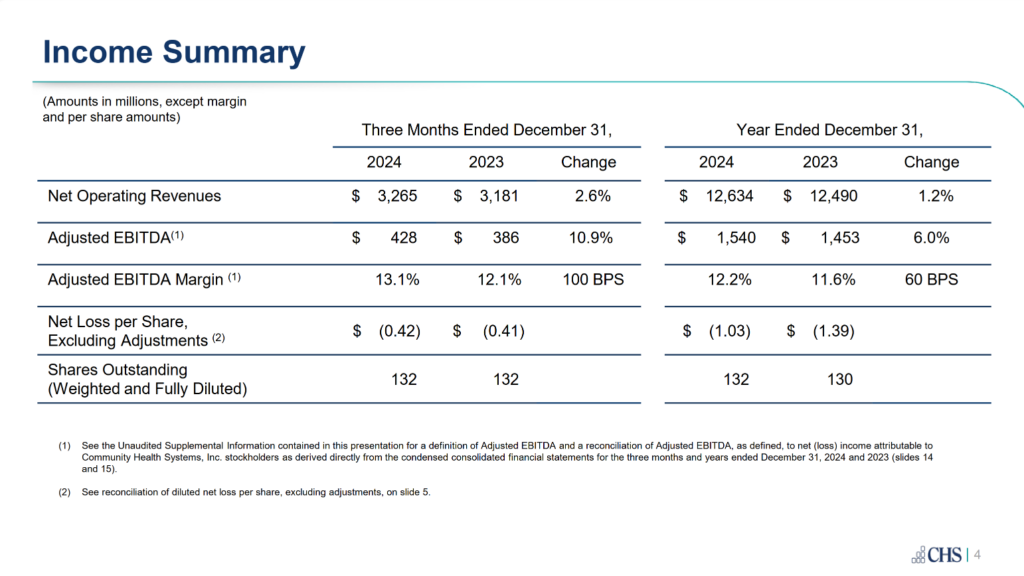

- Adjusted EBITDA margin: Adjusted EBITDA margin up 100 bps YoY to 13.1% in Q4 (vs. 12.1%). Overall, up 6% YoY ($1.54B in 2024 vs. $1.45B in 2023).

- Labor: Contract labor spend down 36% YoY. ($170M in 2024 vs. $265M in 2023)

- Medical Specialist Fees: Up 12% YoY in Q4 (biggest expense pressure point; anesthesia singled out as a cost pressure).

- Supplies: ~15.5% of revenue, a ~50 bps improvement.

- ERP implementation expected to drive $40M-$60M in cost savings in 2025.

D. Capital Allocation

- Divestitures: Ongoing portfolio optimization, with >$1B potential proceeds in 2025. $550M in expected proceeds from announced hospital divestitures in Florida and North Carolina.

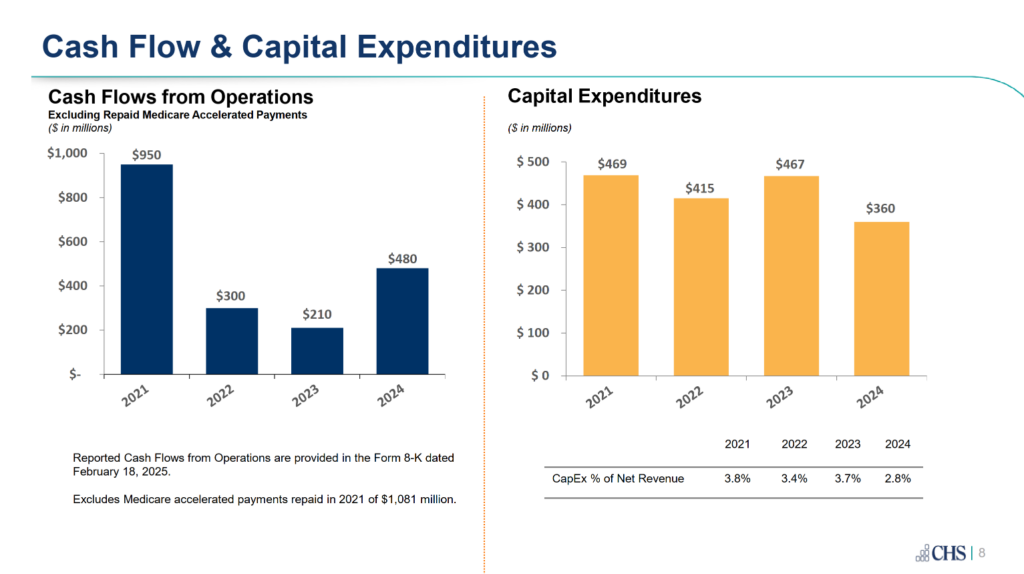

- Capex: ~$350–$400M planned for 2025, focusing on expansions, ASC/freestanding EDs, technology (ERP system).

- Debt Reduction: Targeting net debt/EBITDA in 7.4× range.

- AI/Tech: Mentioned ERP for supply chain/labor efficiency; no major AI details.

- ASC and freestanding ED expansion remains a focus.

E. Outlook & Guidance (2025)

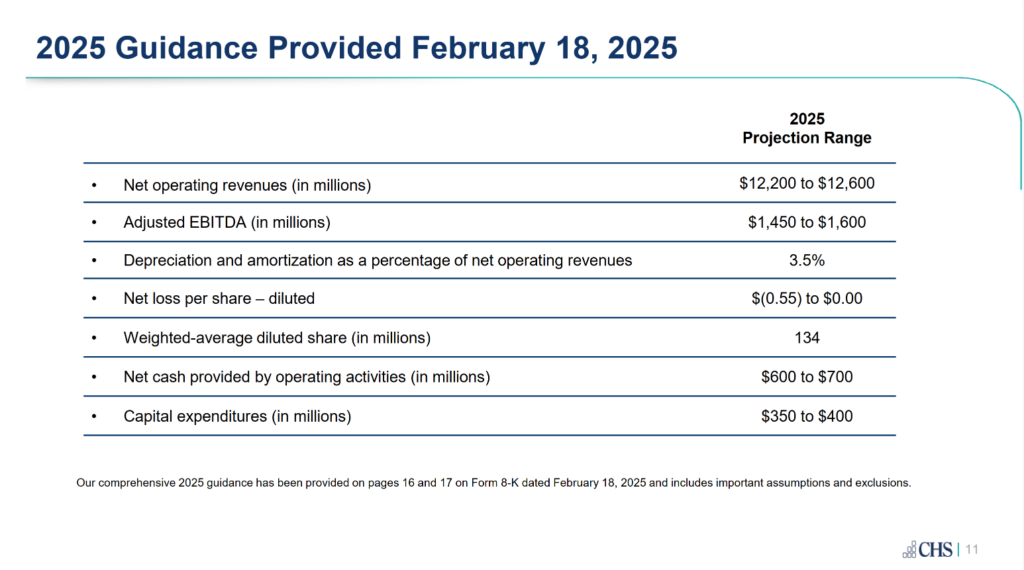

- Revenue: $12.2B–$12.6B

- Adjusted EBITDA: $1.45B–$1.60B

- Operating Cash Flow: $600M–$700M

- Same-store volume growth expected at 2%-3%; modest margin expansion.

- Exclusions: Potential DPP approvals in NM/TN not assumed; additional unannounced divestitures also excluded. Guidance excludes potential $100M-$125M boost from Medicaid DPP approvals.

- Payer mix improvements & commercial rate increases expected.

- ERP-driven cost savings expected to offset inflation.

F. Analyst Q&A Summary

| Analyst | Question | Management Response |

|---|---|---|

| Jefferies (Brian Tanquilut) | 2025 EBITDA bridge & impact of divestitures | $100M reduction due to DPP & divestitures, $75M-$100M in organic growth. |

| Jefferies (Brian Tanquilut) | Future divestitures & growth plans | Still evaluating further divestitures, expanding ASCs, freestanding EDs, and behavioral health. |

| UBS (A.J. Rice) | Margin expansion & medical specialist fees | Aiming for mid-teens EBITDA margin, specialist fees remain a headwind but stabilizing. |

| RBC (Ben Hendrix) | Medicaid DPP programs | $40M from New Mexico was expected, Tennessee approval expected soon. |

| Barclays (Andrew Mok) | Operating cash flow improvements | $70M-$75M expected from tax refund, ERP implementation should boost cash flow. |

| Wells Fargo (Stephen Baxter) | Hurricane impact on Q4 volumes | $10M impact in Q4, no ongoing impact as assets being divested. |

| Nephron Research (Josh Raskin) | Competitive landscape for ASCs & hospital divestitures | ASC expansion continues, divestitures expected to further reduce leverage. |

Final Takeaways

- Overall, poor showing from CHS compared to investor expectations and management commentary around a potential turnaround. The hospital operator can’t seem to get out of its own way.

- CHS posted strong volume growth, with record same-store admissions and ASC expansion.

- Revenue growth of 5.5% YoY was driven by volume & payer mix improvements.

- Cost control efforts helped improve margins, but rising medical specialist fees remain a challenge.

- Significant deleveraging efforts underway, with $1B+ in potential asset sales.

- Medicaid supplemental payments boosted Q4 results, but 2025 guidance excludes potential DPP revenue.

- ERP implementation expected to drive $40M-$60M in cost savings.

- Mid-single-digit revenue growth expected in 2025, with continued ASC & outpatient expansion.

Ardent Health

A. Volume & Utilization

- Admissions: +11.5% YoY in Q4 (partially easy comp from prior cybersecurity incident). Full-year adjusted admissions +4.8%.

- Service Lines: Cardiology, neurology, general medicine strong. Surgeries +6.3% in Q4.

- Acuity: Stable to slightly rising as low-acuity shifts to ambulatory.

B. Revenue Growth & Payer Mix

- Total Revenue: +19% in Q4, +10% full year.

- Net Revenue/Adj. Admission: +3.4% in 2024.

- Commercial Mix: ~43.6%, up ~100 bps. Medicaid fell ~90 bps.

- DPP Programs: Big tailwind from NM retroactive approval ($94M revenue / $65M EBITDA in Q4).

C. Expenses & Margin

- EBITDAR Margin: +240 bps to 12.5% for 2024.

- Adj. EBITDA: +58% YoY.

- Labor: Contract labor down from 4.3% of SWB to 3.6%. Physician subsidy costs still high but moderating.

D. Capital Allocation

- Liquidity: $557M cash, 2.9× net leverage.

- CapEx: $188M in 2024, guiding $215–$235M for 2025.

- M&A: Acquired NextCare urgent cares (NM, OK). Urgent care is a strategic growth area. Also looking at ASCs, imaging centers, etc.

- No Share Buybacks discussed; focus on expansions + deleveraging.

E. Outlook & Guidance (2025)

- Revenue: $6.2–$6.45B (+6% at midpoint).

- Adj. EBITDA: $575–$615M (~19% growth).

- Adj. Admissions Growth: +2–3%.

- NPSR per Adj. Admission: +2.1–4.4%.

- Capex: $215–$235M.

- Margin: Aims for mid-teens EBITDAR over 3–4 years.

F. Analyst Q&A (Ardent) – Tabular Summary

| Analyst | Question | Management Response | Key Points |

|---|---|---|---|

| Leerink (Whit Mayo) | NM DPP recognition? 2–3% volume guide rationale? | $65M EBITDA from NM DPP if timely. Volume comps high in Q4’24 due to prior cyber event. 2–3% is normal baseline. | Retroactive DPP can cause quarterly lumps. |

| Mizuho (Ann Hynes) | Hospital-based physician fees? Margin expansion drivers? | Physician subsidies remain a headwind but not as severe as 2023. Ongoing labor & supply chain efficiencies for 100–200 bps margin improvement. | Target mid-teens EBITDAR in 3–4 yrs. |

| Stephens (Scott Fidel) | JV pipeline, 2025 OCF & CapEx seasonality? | JV negotiations active, no slowdown. OCF around high-$400M. CapEx slightly back-end weighted, but less skew than 2024. | Potential academic JV deals. |

| RBC (Ben Hendrix) | More urgent-care acquisitions? | Pipeline robust; urgent care remains top priority, also ASCs/imaging. Physician fee growth ~ same as 2024. | 18 NextCare clinics newly acquired. |

| BofA (Joanna Gajuk) | Volume comps from cyber, site-neutral reform? | Q4’24 yoy boosted by easy comps. Site-neutral impact would be small (~$10M or less). | Cyber incident depressed Q4’23. |

| Morgan Stanley (Craig Hettenbach) | DPP renewals, acuity trends? | DPPs widely supported; sees minimal risk. Acuity up from service-line optimization. | Potential new DPP expansions in OK, NM. |

| KeyBanc (Matt Gillmor) | LoS improvement from AI (BioButton)? DPP timing in 2025? | Early results show reduced mortality, readmissions. If DPP is delayed, revenue lumps later but same full-year total. | AI in pilot phases. |

| JPMorgan (Ben Rossi) | NPSR/adj. admission wide range? Exchange plans? | 2.1–4.4% range accounts for payer mix shifts. Exchanges ~3.6% of revenue, rates near Medicare. Still a small but growing slice. | Pricing improvements remain ~4% in commercial. |