Hospital Q1 2025 Earnings Themes: Key Takeaways and Scorecard

Expanding margins, rising acuity, favorable payor mix from exchange volumes, decreased length of stay (impacted a bit by flu season), a low point in the labor market, operating expense leverage, strong utilization and same-store volumes, murky tariff and policy on Capitol Hill, supplemental payments flux, and more updates happened this quarter from the for-profit hospital crop.

Here’s what you need to know.

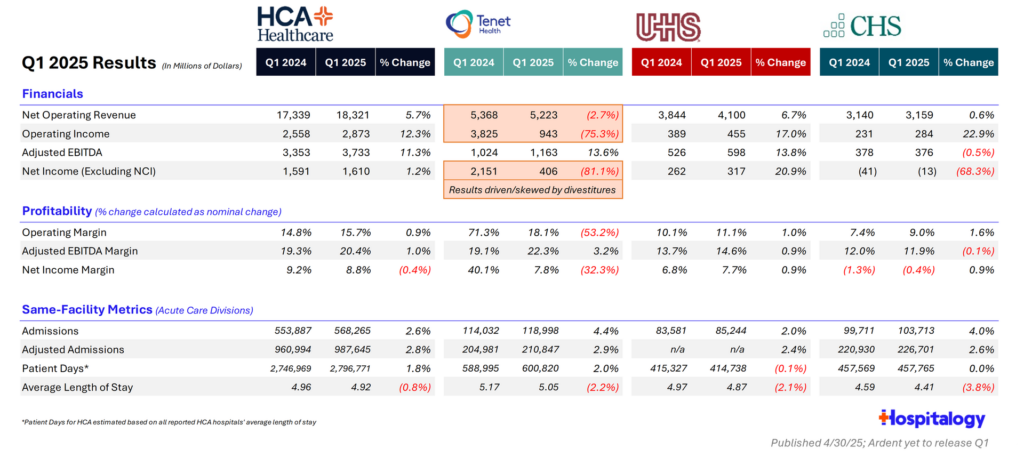

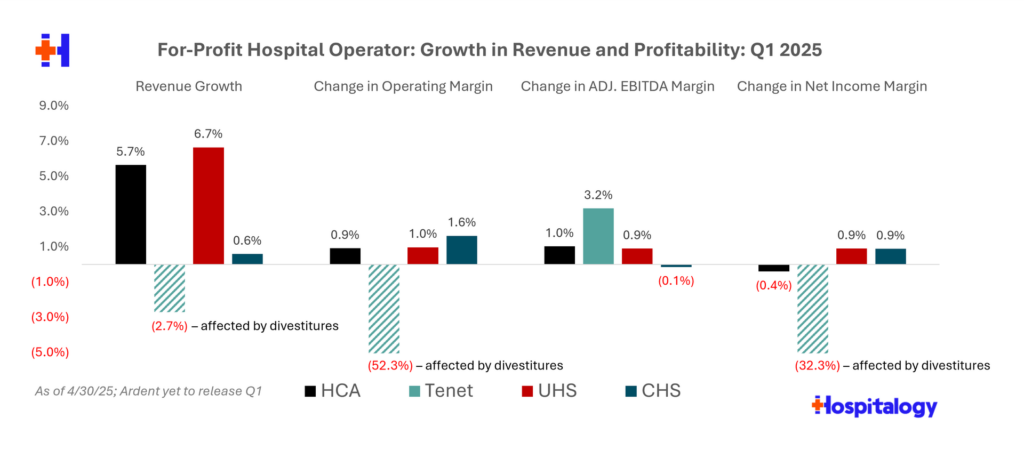

HCA remains the volume bell-whether. Broad market-share gains, more inpatient growth than they can build for, and a strong ambulatory outlook to boot keeps HCA in the driver’s seat along with favorable payor mix, better ED throughput/LOS management, and rising acuity in HCA hospitals. Tariff exposure is currently minimal.

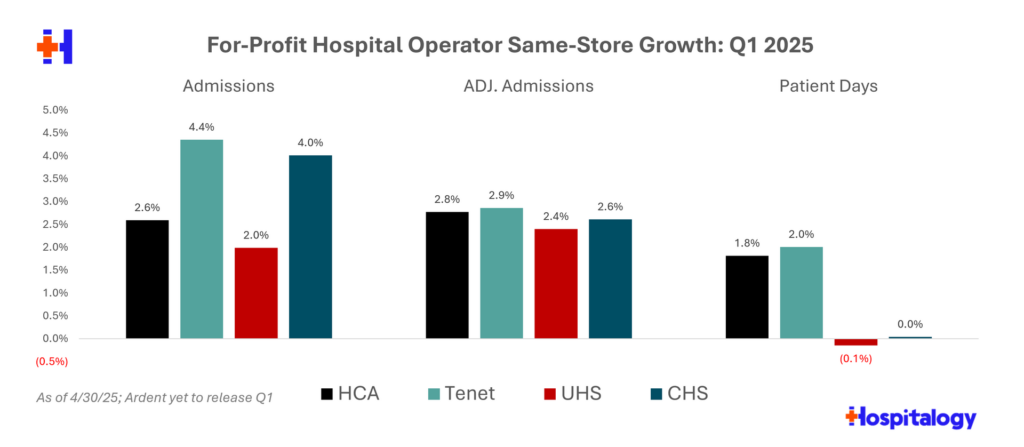

Tenet also crushed Q1. USPI is firing on all cylinders, adding 6 new centers and a partnership in Midland, Texas. It’s delivering the best incremental margin thanks to USPI mix shift (12% growth in total joint, with huge rise in revenue per case growth!!) and labor cost containment. Adjusted EBITDA margin grew 320 bps to 22.3%!!! The hospital portfolio grew admits 4.4% on a same-store basis. Its leverage is historically low at 3.1x; ASC pipeline healthy; likely guidance lift once Tennessee DPP clears.

UHS showed acute-care strength behavioral health volumes lagged from weather and Leap year effect. Still, reimbursement came in incredibly strong at 5.8% growth in Q1 with favorable contracts from managed Medicaid partners. New-build hospitals are ahead of plan, which will matter more in 2H once Medicaid cash timing normalizes.

CHS is the turnaround laggard. Volume green-shoots exist, but payor mix drag and its debt load (what’s new) with leverage > 7× keep equity optionality high. Continued execution on its (evergreen) divestiture plan and cost savings are critical catalysts.

Margins Expand in Q1…

…Driven by Strong Broad-Based Volume Growth

For-Profit Hospital Operator Key Themes from Q1:

Utilization Trends: Demand for higher-acuity service lines (cardiac, ortho, trauma) stayed firm; flu raised Q1 medical volumes across the board.

Favorable Labor Market: Each operator posted significant leverage over its salaries and benefits. Huge theme for most of 2024 and now here in 2025. Wage inflation has cooled; contract labor comprises less than 5% of cost for all operators. Recruiting momentum and internal nursing schools were highlighted as key contributors when in reality there’s probably a bit more going on under the hood, maybe with the economy, maybe with post-pandemic trends. I would love folks who are closer to labor environment to chime in here with more nuanced takes on what you think is going on. Still, kudos to these players for working on retention and nursing opportunities. But having SWB at something like 44% for HCA and 40.6% Tenet is wild. That is massive expense leverage.

Tariffs, Cost Containment: Analysts and execs are honed in on the rapidly evolving supply-chain environment as tariff rhetoric grows. When asking all four how the operators are hedging potential China tariffs, teams responded largely with locking in fixed price contracting and shifting to domestic sourcing.

Supplemental Payments Noise: Timing noise everywhere as state and federal policies are a wildcard – Tennessee being a big catalyst for HCA. HCA saw an $80M benefit in Q1; Tenet is still expecting $35M from Tennessee (not yet approved); UHS was paid in April from Nevada, still waiting on DC & TN; CHS awaiting NM & TN (~$100-125M upside).

The Last Year of Exchange Growth: ACA volumes continue as a significant revenue mix tailwind. Tenet exchange admits +35 % YoY (7 % of revenue). HCA 22 % growth. UHS +20 %. CHS < 6 % of revenue but growing.

Capital Allocation and M&A Focus on Ambulatory, De-novo Inpatient Buildout: General use of capital for hospitals includes 1) Growth cap-ex, 2) ASC or tuck-in M&A, 3) De-leverage or buyback. HCA & Tenet both heavy repurchasers. Tenet earmarks $250M for USPI annually and constantly notes a ‘robust pipeline’ (which there is). CHS can’t get out of its own debt sludge and is funneling asset-sale proceeds to offload. UHS continues share repurchase even while building new hospitals. Also, HCA and Tenet continue to stay deleveraged (AKA, ebitda to total debt ratios) at a historically low level for these players.

Guidance and Outlook Fogged by Policy Outlook: Interestingly, despite the pretty strong Q1 with all things considered, management teams didn’t raise guidance. This decision speaks to the fluidity of the uncertain policy situation, because hospitals only have so many levers to pull. There’s only so much you can do if the Trump Admin cuts Medicaid reimbursement, services, ACA subsidies, implements site neutral reform, heightens and intensifies tariffs, and more. Still, if current patterns hold you should expect to see mid-year guidance increases especially given how big Tenet crushed Q1.

Policy Sensitivity:

- China-source supplies and effects of tariffs; ability for hospitals to mitigate change in supply chain / costs

- Medicaid flux

- Supplemental payments and whether the Trump Administration addresses them

- Exchange volumes headed into 2026

- Medicare Advantage penetration rates in local markets, denials

Other Hot Buttons this Quarter: With how low the contract labor environment seems to be, and with for-profit players exhibiting their strength over that portion of the income statement, analysts questioned the sustainability of keeping SWB this low. I’m inclined to agree and have to think the pendulum…at some point…swings back to a more normalized spot. But the question is…maybe this labor environment is the new normal for the hospital operators who are able to stay ahead from a position of strength. In general analyst Q’s centered around margin sustainability, contract-labor durability, Medicaid DPP timing, tariff exposure, the exchange subsidy cliff, how long the total-joint runway is for ambulatory growth (USPI), behavioral volume cadence (UHS), and pacing of CAPEX.

Join my Hospitalogy Membership! If you’re a VP or Director working in strategy or corporate development at a hospital, health system or provider organization, you will get a lot of value out of my community as I purpose-build the content, fireside chats, and conversations for this group. Join for free today.