Hospitalogists,

This essay continues my ongoing series on interviewing health system leadership.

After chatting with Baylor’s Pete McCanna, I talked to Fairview Health Services’ James Hereford (his LinkedIn here) a couple weeks ago and really enjoyed my conversation.

This essay is a breakdown of our conversation along with some Q&A at the end. We talked all things Fairview and the turnaround the health system has experienced over the past couple of years, including consumerization, revenue diversification, local market dynamics, the potential impact of ICHRA, and Fairview’s strength in pharmacy – including its new pharmacy business launched in late 2024 – Fairview Pharmacy Solutions.

Let’s dive in!

Oh and don’t forget – for more conversations revolving around health system strategy, leadership, and finance and for those working in hospitals, health systems and provider organizations, apply to join my curated Hospitalogy community here!

Topics covered during my discussion with James Hereford, President and CEO of Fairview Health Services

- Health system transformation; consumerization

- Revenue diversification – Fairview Pharmacy Solutions, Acadia 144-bed joint venture

- 340B and specialty pharmacy growth

- Capacity management – ED capacity buildout, observation unit micro hospitals to alleviate bed capacity

- Expense management and turnaround activity, outsourcing

- Local market dynamics around physician alignment; physician employment dynamics “we don’t need to own everything in healthcare”

- Large independent physician groups in Minneapolis around key service lines forces Fairview to “play ball”

- Low unemployment means competitive employment market; employers less focused on drilling down on cost of benefits because they’re more focused on retention and competitive benefits offerings to their employees

- Entrance of for-profit insurers within the past 5 years (UHC, Aetna) has introduced more payor competition, which is good for Fairview

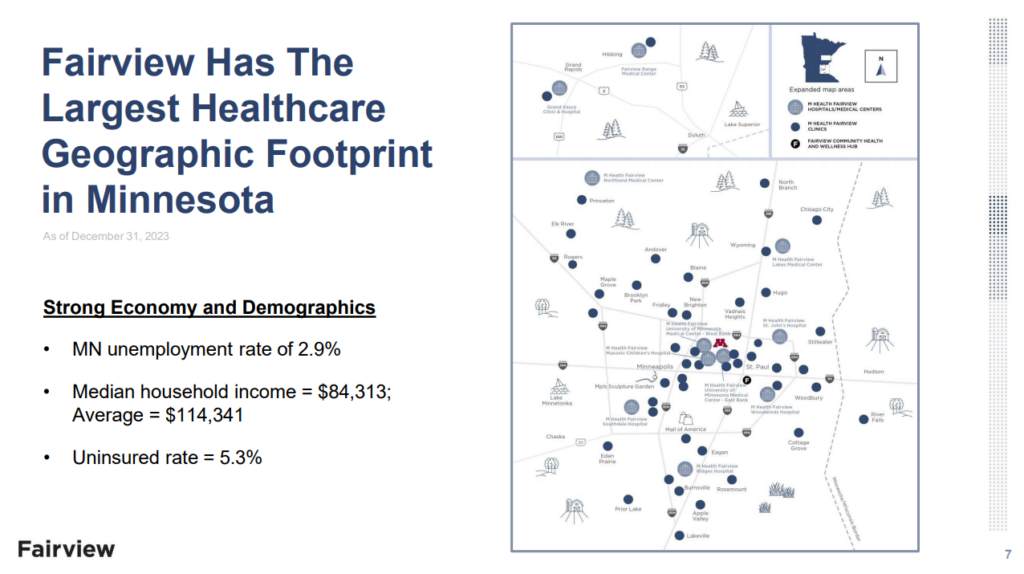

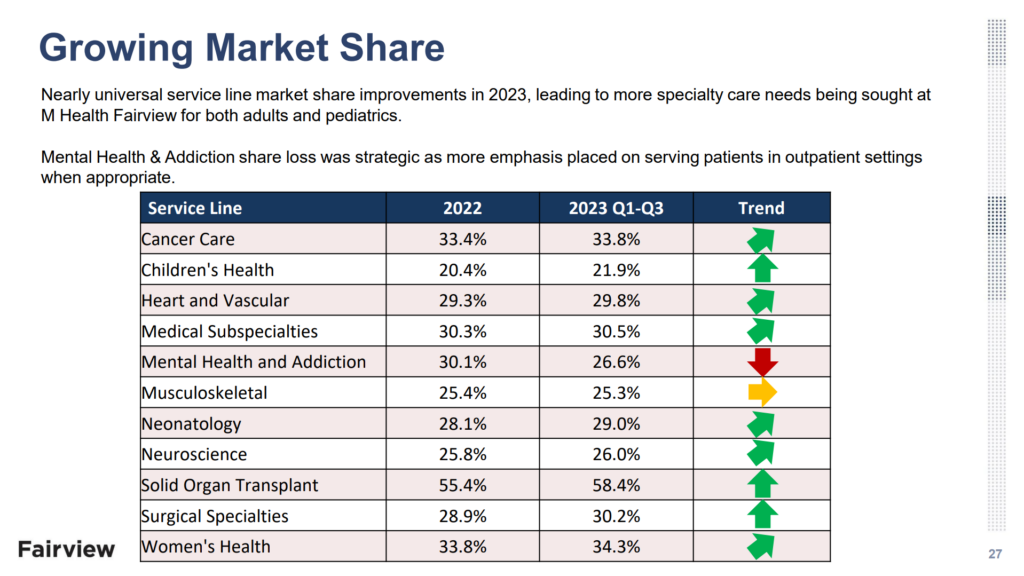

- Fairview has dominant market share (30% of inpatient admissions) in Twin Cities

- Sustainability of current commercial vs. government pricing and threat of ICHRA if defined contributions continues to gain steam → lower reimbursement to provider organizations

10,000 foot overview of Fairview Health Services

Here’s a quick overview of Fairview Health Services.

The health system is based in Minnesota and operates 10 hospitals, 37 retail and specialty pharmacies, 80 primary and specialty clinics, and is the largest nonprofit senior care provider in the country. Fairview generated over $8B in total operating revenue in 2024, operating income of $51M, and net margin of $185M – significantly greater than results in 2022 and 2023, where Fairview was losing money. It partners with the University of Minnesota on tertiary and quaternary care, and holds a network of 4,300+ affiliated providers while employing 34,000+ FTEs as one of the largest employers in the state of Minnesota. In 2024 Fairview admitted nearly 90,000 patients into its hospitals which comprises approximately 30% of inpatient market share across its geographic service area.

Fairview has been on a few years long path to financial and operating recovery post-pandemic. In talking with James, here’s what they did to turn things around.

The Turnaround: How Fairview Flipped the Script in 2024

James outlined how the organization moved from a $200M operating loss in 2023 to a $41M (and improving) operating margin in 2024 – up to $320M in net margin in 2024 as well. The recovery rested on three pillars: labor discipline, pharmacy growth, and operational rigor.

Labor discipline produced the single largest swing. Post-pandemic, labor costs were out of control. A quarter of Fairview’s workforce was travel nursing, and by the fourth quarter of 2024 that figure had fallen into the low single digits after an aggressive campaign to recruit permanent nurses, emphasize retention, rationalize premium pay policies, and standardize clinical staffing ratios. The initiative removed tens of millions of dollars in variable expense without compromising quality scores.

Length of stay management and throughput was more efficient while acuity rose. There are generally a ton of challenges with patients coming in and being put into observation care, creating challenging length of stay environments. Fairview implemented – and continues to implement – processes to manage patients who were in acute care but didn’t need acute care level care and were challenging social circumstances. The team also tackled extreme outliers, for example patients ordered by a judge to remain in the hospital or individuals with complex social circumstances who previously sat in acute beds for weeks. On a similar vein, Fairview is thinking about how to leverage post-acute assets more effectively to get people out of the hospital and into more appropriate environments to match their acuity and need. Care navigation and coordination comes to mind here, similarly to what Baylor mentioned as a core need.

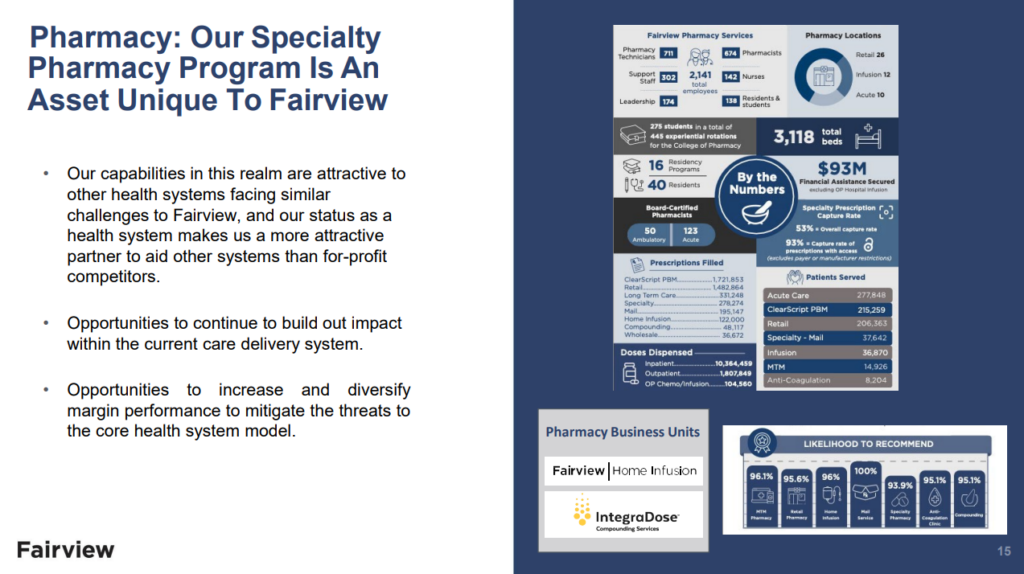

Pharmacy growth supplied a significant growth engine. Fairview’s pharmacy division reported a 20%+ increase in top‑line revenue year over year. Home infusion volumes expanded at a similar clip, capturing ambulatory utilization that previously defaulted to the inpatient setting.

Operational rigor closed the expense gap. Centralization and outsourcing were big themes for Fairview across certain administrative functions. A new system operations center provides real‑time visibility into census, acuity, and staffing across the entire network. Weekly standing meetings track throughput metrics, revenue‑cycle performance, and scheduling backlogs, creating a cadence of continuous improvement. In thinking about the operating turnaround, there was no rock that wasn’t overturned and James constantly asked the team “how can we do things better?” And these questions resulted in lots of good hard work on the ops side – revenue cycle management, care access processes, managing scheduling, and more.

There was one point where James thought everything was broken but (luckily for Minnesotans) he doesn’t feel that way anymore. Fairview is on the up and up.

Join the thousands of healthcare professionals who read Hospitalogy

Subscribe to get expert analysis on healthcare M&A, strategy, finance, and markets.

No spam. Unsubscribe any time.

Understanding Minnesota’s Healthcare Market

Let’s back up for just a second and talk about the Minnesota market, drilling down into the Twin Cities, a major population hub. One of the first questions I asked James was around Minnesota’s local markets and the Twin Cities specifically. What are the economics of the healthcare delivery market there, and how do those mechanisms differ from other areas of the country? Here were some of the more unique aspects.

An Efficient Care Delivery Market. Fairview operates in a uniquely efficient and competitive environment within the seven‑county Minneapolis Saint Paul metropolitan area. Fairview as a health system is the only care delivery organization that has complete coverage of the entire 7-county service area, but faces competition throughout those strongholds. Still, as a result, Fairview holds an impressive 30% or so inpatient market share, but the market both on the IP and ambulatory sides is competitive as a whole. James mentioned the Twin Cities is a very efficient market when it comes to care delivery.

Payor Environment. On the payor and reimbursement side, the market is growing competitively. But because of the competitive provider environment and a historically Blues plan, these combined effects kept commercial reimbursement muted. In more recent years, the state has allowed for-profit players to enter the market, so players like United and Aetna have joined in the fun, adding more competition to the market but having no effect (yet, at least) on rates.

Academic Medical Center Dynamics. Fairview partners with the University of Minnesota on academic tertiary and quaternary care, but there’s an interesting dynamic with the Mayo Clinic being 80 miles to the south. Fairview’s academic footprint tends to see more government-heavy patient mix simply because of how strong Mayo’s branding is (and this effect is nationwide). Stated differently, Mayo has an incredibly strong commercial draw of patients and tends to leave Fairview with the lower reimbursing government book of business.

Large Independents Dominate MD Affiliations. Here’s one of the more unique dynamics for a big-city healthcare market. Large independent specialty groups such as Twin Cities Orthopedics, Minnesota Oncology, and MNGI Digestive Health control significant outpatient volume. As a result, the market is driven more by ASCs and outpatient migration, moving from the hospital to ASC environment. This dynamic makes physician alignment more difficult, and health systems have to play ball. Fairview chooses not to pursue a closed‑network model, instead positioning its hospitals as the preferred inpatient destination when complex admissions are necessary.

Labor Market is Tight. James mentioned wages run relatively high in the Twin Cities and that nurses in this market hold the second highest pay rate in the country, which presents its own unique challenges, especially given nursing unions. This dynamic forces Fairview to be disciplined operationally. E.g., how to use capital to drive down its cost structure, and where to identify segments and market opportunities to leverage capabilities and expand. More on that in a bit.

On the Sustainability of the Employer Commercial Market, and ICHRA

Speaking of the labor and employee environment, James and I had a great chat around employer dynamics in both the Minnesota market, but also the dynamic that has existed in healthcare for the past 30 years between commercial insurance and government insurance and the reimbursement disparity / hidden tax.

A big worry of Hereford’s is the deteriorating cross subsidy between governmental and commercial payors, and we spent a decent amount of time dissecting the various factors at play here. Decades of underpayment by Medicare and Medicaid have been offset by consistent year‑over‑year increases in commercial premiums. Rising employer resistance, the recent emergence of Individual Coverage Health Reimbursement Arrangements (ICHRA), and the maturation of direct contracting models threaten to unwind this arrangement.

I asked James about the sustainability of all of this. And it’s something I ask a lot of people. WHEN is the breaking point? Employer healthcare costs rise so much every year, yet they continue to stomach it. What will break it?

While we don’t know the answer to that question, nevertheless, the dynamics described above will continue to catalyze employers to seek out more creative structures for their health benefits, ICHRA and direct contracting being marquee examples here (and also in line with Mark Cuban’s thoughts on all this unnecessary healthcare complexity). James mentioned this as an acute threat to the current reimbursement model for provider organizations and one Fairview needed to pay attention to. If more employers adopt ICHRA or go direct, that’s a big threat to your most lucrative source of patient revenue.

I also asked James whether he perceives employers going direct as an opportunity for Fairview given the care delivery and network asset base they operate. James said yes, but caveated it by saying a network or marketplace needs to exist to facilitate this kind of arrangement, and that complexity is holding employers back from going all in on something like this. Large employers simply don’t want the complexity of dealing with all the direct contracting – but the complexity may be worth it if the current strategies aren’t controlling costs and the tight labor market makes employers be more competitive with benefits. Health benefits act as a competitive advantage for employers in tight markets. Tight labor market makes employers less aggressive with health benefits and medical cost management.

During James’ time at Stanford Health, he noted the premier academic health system experienced this competitive employer market dynamic all the time, to Stanford’s benefit. Tech companies ONLY cared about attracting engineers. They didn’t care about healthcare services price at all. Stanford priced aggressively and benefited from that, of course.

So eventually, over time, the thesis is that we’ll see a lot more direct purchasing by large organizations of healthcare services. This thesis is in line with Mark Cuban’s thoughts on healthcare, and has also led to movements like direct primary care. A good example (noted already) of a potential ‘disruption’ path lies within ICHRA. If a large employer gets out of defined benefits and goes to defined contribution and pushes their employees to the individual markets, the tight labor market keeps people from making that move for now, but there’s a point where that pathway makes sense for employers. But overall that move would be devastating for hospitals and health systems because it fundamentally changes the calculus for organizations like Fairview and revenue reimbursement. Again, you’re losing employer sponsored insurance for something lower reimbursing.

Sustainability of the Physician Employment Model

You might notice a theme of our discussion. We talked a lot about healthcare economics and sustainability, which was right up my alley. Next I asked him about the sustainability of the current hospital physician employment subsidy model. Here were my takeaways from this portion of the conversation.

You can’t control physician behavior even if they’re employees. As soon as they become their employees, what health systems tend to do is unload their overhead on these practices. And when they acquire these practices, it’s highly probable they weren’t financially sustainable anyway how they were being run, so they add some labor and overhead by default, and the integrated practice immediately becomes a cost structure issue for the enterprise.

So Fairview tries to take a more manicured approach. It maintains employment for primary care physicians to guarantee access and moderate panel churn, but it remains agnostic for many procedural specialists who may function more efficiently as independent partners. Hereford noted Allina Health’s physician unionization effort as evidence that formal employment does not automatically align incentives or benefit a health system economically (and for physicians, they sometimes learn unionizing isn’t what it’s necessarily chalked up to be). James also said there was / is this big urge in healthcare to own everything, and owning everything doesn’t always mean finding success in everything.

For that reason, Fairview’s physician alignment posture is to be amenable as possible to independent physicians, especially given the large independent group dynamic in the Twin Cities. They never had a strategy to internalize everything. Large groups need a place to do their inpatient cases, and they want to be amenable to that. Nowadays so many cases are being done on the outpatient basis and that changes a health system’s revenue profile over time. Fairview also has to prepare for this future and continued outpatient migration. And this will continue to happen. Why? Because physicians are incentivized to move things outpatient, because this is where their ownership opportunities lie.

The Power of Specialty Pharmacy, the 340B Program and the Cost Inflation Gap

The most unique aspect of Fairview’s turnaround, in my view (apart from the secular macro trends bolstering hospital bottom lines) was its prowess in the pharmacy segment. Let’s take a closer look, and James had a lot of great commentary for me.

Fairview is also dealing with what all health systems contend with, which is the classic 2% – 4% problem. Breaking this down, a hospital’s cost structure will generally inflate 4% any given year, between labor and supplies, unless you hold massive leverage (and most don’t). Meanwhile, your blended payor reimbursement rate goes up 2%, maybe 3% in a good year. So every year, using Fairview as an example, you have $160M you’re losing to cost inflation and that you have to make up somewhere – more efficiency, more volume – just to break even. Or…as an enterprise, you need to look to other arenas. To make up that deficit, you can’t depend on payor revenue. So what’s the other avenue? Fairview, and other health systems, have to look at diversification strategies to grow and sustain.

For Fairview, its retail and specialty pharmacy segment is its most scalable lever to diversify revenues and narrow that spread. Specialty pharmacy and home infusion volumes have been massive for Fairview. For instance, Fairview’s pharmacy services revenue grew 20% year over year in 2024, and under Executive Vice President Bob Beacher, Fairview launched a new venture – Fairview Pharmacy Solutions. After identifying this core strength combined with Fairview’s intellectual capabilities, Fairview launched FPS in late 2024. The venture leverages Fairview’s strong pharmacy division and sells those infrastructure services, namely its technology stack and contract management expertise (RCM, etc.) to other large health systems, many of which operate under-optimized 340B programs – targeting Fairview’s peers: the top 50 health systems in the country – the ones big enough and complex enough to need help optimizing their 340B and pharmacy programs. This launch is just one such example of a large, scaled health system player working to diversify its revenue streams while focusing on areas of strengths.

On that 340B note, I also asked James about the 340B program as a whole and its sustainability and outlook. James noted that it’ll be evergreen to see litigation and drug manufacturer pushback (given deep legal pockets), but he doesn’t foresee wholesale elimination of the program. Stroke of pen risk gives existential heartburn to health systems. So many hospitals absolutely depend on 340B revenue and you’d end up closing a bunch of small hospitals across the countries if we saw material change to the detriment of these facilities. So the program itself isn’t at risk, but Pharma doesn’t like giving away drugs at a discount.

So what’s the balance? There are some changes you could enact to increase oversight of the program. It should have appropriate oversight, but there are other positive changes you can make. For instance, the notion that you would have to prove out the program is benefiting specific populations in your service geography. So to that end, James supports stronger program oversight provided policy makers preserve the economic lifeline the discount creates for rural and safety‑net hospitals.

Driving Transformation Through Strategic Partnerships

Transformation at Fairview is treated as a repeatable capability rather than a one‑time initiative. Recent examples include:

- Acute Diagnostic Services clinics that provide same‑day imaging and minor procedures, reducing avoidable emergency department visits and accelerating downstream scheduling.

- Hospital at Home expansion that allows high‑acuity patients to recover in their own residences, opening staffed beds for higher margin surgical admissions.

- Observation unit and emergency department expansion to relieve boarding pressure and improve throughput.

- Joint venture with Acadia Healthcare on a 144 bed inpatient treatment facility to add behavioral health capacity without monopolizing Fairview’s balance sheet (Fairview retains a minority interest in the JV).

- Artificial intelligence pilots focused on ambient documentation and predictive staffing to reduce administrative burden and overtime.

From a social determinants perspective, Fairview is exceptionally proud of its community initiatives. The health system operates a Hub for Health and Wellness in partnership with Second Harvest Heartland and the Sanneh Foundation. The program distributes more than one hundred thousand pounds of food each week, and providers can issue food prescriptions that community partners fulfill. Parallel collaborations with housing authorities increase access to stable living environments for high‑risk patients.

Looking Ahead: Community Commitment and Strategic Growth

Turning finally to strategic growth and 2025 outlook, Fairview entered 2025 on plan with early indicators tracking to budget. Leadership will focus on expanding pharmacy services, scaling home‑based care models, and deploying artificial intelligence pilots across additional service lines. Weekly operating reviews remain non‑negotiable to ensure movement forward.

Fairview continues to have good momentum in 2025, and is on plan for this year, James wants to continue to grow capabilities for the organization. But he’s most proud of Fairview’s community efforts and thinks of these efforts in the same way he thinks about the Fairview enterprise – partnering with organizations where they can extend their community services, and invest heavily in the areas Fairview serves. 20% of a population’s health is determined by social and environmental factors like where you live, zip code, access to good food, housing, etc. Fairview wants to do even more in this regard.

Fairview’s community partnership model has been huge. James mentioned that often hospitals and other healthcare entities show up and think they have all the answers when in reality partnering with community services who have better core competencies in their local communities is a much better path forward. This approach also builds trust and introduces collaboration, key components of population health from a social perspective.

Hereford closes every strategy discussion by returning to community impact. Fairview physicians now write food prescriptions, social workers match patients with affordable housing, and the system funds nonprofit partners that possess deeper expertise in neighborhood‑level interventions. In his view, health outcomes derive more from ZIP code than genetic code; therefore, Fairview’s long‑term relevance depends on marrying clinical excellence with authentic community collaboration.

More Q&A with James

I had a few rapid fire questions I sent over to James after our conversation, and this Q&A is memorialized here.

What’s your leadership style? How do you get buy-in from both your administrative and clinical teams system-wide? How do you identify talent at Fairview and build teams?

I surround myself with very smart, talented and motivated people, collaboratively set the direction, and then let them go do great things with appropriate monitoring of their progress in terms of both execution and learning.

At Fairview, buy-in starts with creating clarity. People can handle hard decisions when they understand the “why.” We talk often about leading with purpose—making sure everyone sees how their work contributes to our mission.

When building teams, I look for people who are curious, humble, and accountable. Technical skills matter, but character matters more. We’ve tried to shift the culture here to one where momentum beats perfection and where leadership is a mindset not a title.

We know a lot of the things facing hospitals and health systems today…labor shortages, rising physician subsidy costs, capacity management, Medicare Advantage denials…but what isn’t being talked about that should? What are you talking about with your peers that keeps you up at night? What’s top of mind, both good and bad?

There’s a lot of discussion about labor costs, MA denials, payer negotiations—but I don’t think we’re talking enough about the fragility of the current commercial insurance model nor what the potential solutions could be.

For decades, healthcare systems have offset losses on the government side by shifting costs to the commercial side. That model is wearing thin. If employers start moving more aggressively toward ICHRAs, direct contracting, or defined contribution models for healthcare benefits, it will fundamentally reshape how health systems sustain themselves.

That’s a strategic risk I think about a lot. And it’s why we’re trying to diversify revenue, improve operational resilience, and focus heavily on value creation—not just service volume.

In what ways are you engaging in health system transformation, both from a partnerships perspective, innovation perspective, and consumer perspective? How does physician investment move the needle for Fairview versus allocating capital to other projects? Are there any interesting new partnership models or ventures that are promising from your perspective? (e.g., your new Acadia joint venture, ASC strategy, observation unit expansion, ED expansion)

We know that the status quo is not sustainable and that the only way we can be successful over the long term is to drive significant levels of transformation. That level of transformation will require us to look at our clinical models of care as well as driving administrative efficiency. We also cannot do this by ourselves. We have to create smart partnerships to leverage their capabilities and capital investments.

We are deeply committed to addressing the social determinants of health through partnership. Collaborating with organizations like Second Harvest Heartland and the Sanneh Foundation, we operate our Hub for Health and Wellness, distributing more than 100,000 pounds of food each week to patients and families. We work closely with housing and public health partners to connect patients with stable housing and other essential services. We believe true community health improvement is only possible through deep trust, collaboration, and shared purpose.

We are expanding the use of AI for operational and administrative optimization and piloting ambient clinical documentation tools to ease the administrative burden on providers. We’re investing in observation unit models and expanding our Hospital at Home program where it makes sense—helping improve throughput, access, and patient experience without defaulting to inpatient expansion.

From a consumer perspective, we are building faster, more flexible care options. We now have five Acute Diagnostic Services (ADS) sites across the Twin Cities—giving patients immediate access to diagnostic testing and minor procedures that historically would have required an emergency room visit or long wait times. For example, if a primary care physician identifies a concern during an appointment, the patient can often be sent to an ADS clinic and have an outpatient procedure scheduled that same day. It’s a faster, smarter, and more patient-centered model.

We view transformation not as a destination, but as a perpetual capability—building a smarter, faster, and more resilient system prepared not just for today’s healthcare environment, but for the realities of tomorrow.

Related to hospitals and health systems and AI…what is the most exciting use case today for Fairview? Is there anything you guys are working on in the near future you’re looking forward to?

AI has tremendous potential, but we’re approaching it with a “use case first, hype second” mentality.

Today, we’re most excited about the operational uses of AI—things like predictive analytics for patient throughput, workforce scheduling, and revenue cycle optimization. Those are immediate ways AI can ease burdens and create real value.

On the clinical side, we’re implementing AI-supported ambient documentation tools to reduce clinician administrative load, which we believe can have a meaningful impact on burnout.

What still needs to be built is a fully trustworthy, integrated AI platform that can support longitudinal patient care—seamlessly blending clinical decision support with operational data without creating more friction for providers.

What went into the decision to dis-affiliate from the University of Minnesota?

Our relationship with the University of Minnesota has been long and important, and we continue to recognize the essential role of the University’s Medical School in Minnesota’s healthcare ecosystem. That said, it became clear that the current relationship is not sustainable as currently constructed.

The decision to create a new partnership with the UofM wasn’t about abandoning academic medicine—Fairview remains committed to supporting education, research, and high-quality clinical care. Rather, it’s about creating the space for both organizations to chart sustainable futures that are culturally aligned and mission-focused.

Throughout this process, we’ve stayed grounded in a few key principles: improving lives, ensuring long-term financial and operational sustainability, protecting strong independent governance, and preserving our nonprofit mission.

We’re currently participating in a facilitation process led by the Minnesota Attorney General’s Office, aimed at reaching a fair and structured resolution. But ultimately, any decision about Fairview’s future must be made by our board and leadership, with the best interests of our patients, employees, and communities at heart.

About James Hereford

Mr. Hereford was appointed President and Chief Executive Officer in 2016. Mr. Hereford joined Fairview after serving as Chief Operations Officer at Stanford Health Care where he was responsible for all inpatient and ambulatory operations as well as various administrative functions. Prior to his role at Stanford, he was Chief Operations Officer at the Palo Alto Medical Foundation where he was responsible for operations serving more than 800,000 people in the San Francisco Bay area. He also served as the Executive Vice President responsible for the Group Health care delivery system in Seattle, Washington, an integrated health maintenance organization that served the state of Washington and northern Idaho. Mr. Hereford holds bachelor’s and master’s degrees in mathematics from Montana State University. He has taught courses with Stanford University’s Graduate School of Business, University of Washington’s Master of Health Administration program and The Ohio State University’s Master of Business Operations Excellence Program.