CVS’ $20B Consumer Pivot

CVS, the company with over $370B in revenue yet an $80B market cap, the company known as ‘3-letter’ to pharmacists, the company which operates a slowly dying retail footprint, the company which felt so threatened by Mark Cuban’s side hustle they felt the need to write out a full op-ed in Fortune, the company with 30%+ PBM market share, a segment of healthcare known for the most opaque economic practices known to mankind, and the company that has returned nothing to shareholders (outside of dividends) over the past 5 years…wants to make things easier for the healthcare consumer – and it is investing $20B over the next decade to do so.

Glaringly missing from its $20B consumer roadmap is the obvious need to make CVS Caremark, the largest PBM by market share, more transparent.

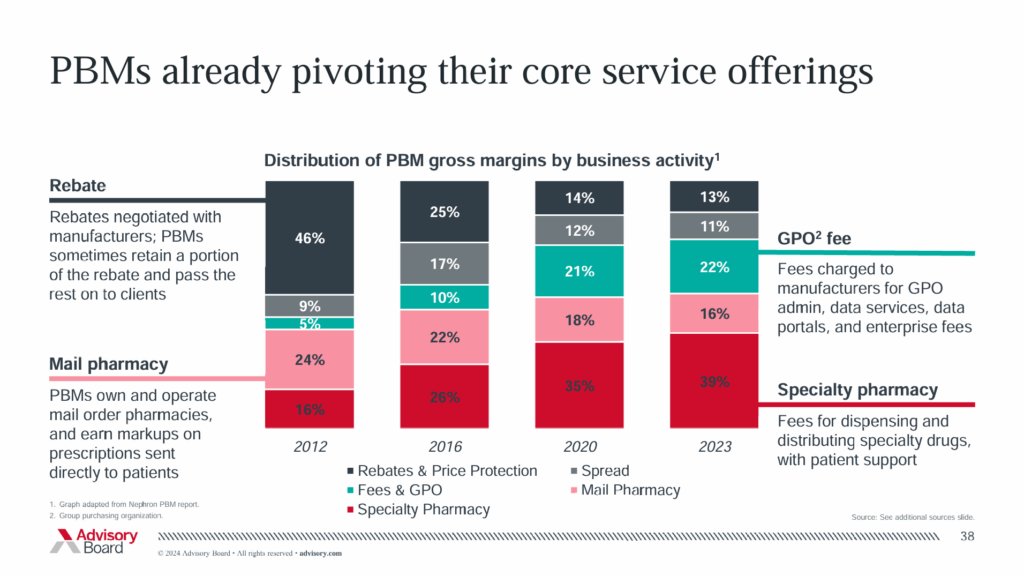

In general, non-competitive, consolidated markets lead to bad consumer experience. Vertical integration leads to patient steerage. While these dynamics CAN work to create a more cohesive, streamlined experience and perhaps more favorable situations for CVS-specific patients, in this walled garden ecosystem with basket-style pricing economics, CVS with its scale and business tactics tend toward anti-competitive practices. Plus they’re…pretty good at preserving margin and moving money away from rebates (hotly attacked in recent memory) to GPO management fees or specialty pharmacy fees (the largest growth vector nowadays) – from a great breakdown from Optum’s Advisory Board (and originally Nephron reporting):

- “While contributions from commercial rebate retention decreased from 46% of estimated profit in 2012 to 13% in 2022 as a greater share of rebates were passed through to plan sponsors, the share of PBM profits derived from fees that are less likely to be shared with plan sponsors has grown from 5% in 2012 to 22% in 2023…

- Putting it all together, we find that while increased pass through of rebates and price protection to plan sponsors have reduced these traditional sources of PBM profitability, novel PBM fees associated with contracting entities [GPOs] are more than offsetting this decline while expansion of specialty pharmacy is now the leading driver of PBM profit growth.” – Nephron Research, Trends in Profitability and Compensation of PBMs & PBM Contracting Entities

Alright. My quips are over – I promise. In an industry with scarcity and allocation of resources, someone has to be the bad guy to be a check on provider/pharma overutilization, and CVS just so happens to operate two extremely large ‘villain’ figures in healthcare – insurance and PBMs.

This rabbit hole aside, credit where credit is due for management around recognizing that CVS needs to reorient its consumer experience. Let’s dive into how they’re trying to achieve just that, since there are some interesting takeaways. While the original article is scant on details, a big part of CVS’ consumer-oriented strategy appears to be focused on interoperability: actually playing nice in the ecosystem.

- Various administrations have attempted to encourage the industry to do this over the years, and a number of startups have attempted to develop platforms to host such an environment. But all have been unsuccessful for one key reason, said Tilak Mandadi, CVS Health’s chief experience and technology officer: Companies have been unwilling to shake things up.”

Wait…is that a CVS executive who just said that?

(alright, NOW I’m done)

CVS wants to embed its consumers into its ecosystem, and that means a more integrated, streamlined experience across the enterprise – pharmacists and Oak Street Health clinicians have complete longitudinal patient records; consumers know upfront prices; better notifications or communication; using AI as a call center extender; etc.

For AI, CVS laid out specific guardrails:

- Never use AI for clinical diagnosis

- Never use AI for prior auth / denials

- Never use AI to prevent human touch

So, long story short, sounds like CVS will never use AI!

As far as CVS’ consumer-oriented strategy and vision is concerned, I’ll believe it when I see it. Actions speak louder than words, and I sure have seen a lot of words from CVS lately. This isn’t to rag on the initiative but more of a ‘raised eyebrows’ challenge at the company at the center of PBM disruption and opacity.

Inside Amazon Pharmacy’s Relentless focus on the Consumer

Here’s a company with a relentless focus on the consumer, and has held this core belief since its inception: Amazon.

Amazon, the company which has devoted every piece of capital in the name of its customers, the company which generates $630B+ in annual revenue and is worth over $2 trillion in market cap with a 65% return over the past 5 years (not market beating, to be fair), is slowly working its way deeper into the healthcare services industry.

Since acquiring PillPack in 2018 and launching Amazon Pharmacy in 2020, Amazon has emphasized affordability and transparency in pharmacy practices, initially targeting those paying cash, then moving into Medicare and directly competing with CVS’ retail pharmacy on both fronts. For Amazon, the end goal is always the consumer with an endless pursuit of making things easier for Amazon customers – even in healthcare, where incumbents don’t play nice.

Amazon bought PillPack to be a consumer healthcare platform play, and they’ve been building it that way ever since, launching transparent products like RxPass and overpaying for acquiring consumer-forward companies like One Medical:

- “[Amazon’s Nader] Kabbani shared [TJ] Parker’s concern about the pharmacy industry and the dominant players’ inability or unwillingness to put the consumer first.”

So, Amazon Pharmacy is reshaping the healthcare landscape by leveraging its unique strengths in digital consumer experience, logistics, and technology-enabled simplification. I talked to Amazon Pharmacy’s John Love last week who was a wealth of information on what they’ve been up to, including PillPack’s move into Medicare and also around enabling caregivers to support loved ones by allowing them to manage medication.

Join the thousands of healthcare professionals who read Hospitalogy

Subscribe to get expert analysis on healthcare M&A, strategy, finance, and markets.

No spam. Unsubscribe any time.

Today Amazon is working receive access to PBM APIs so that members can access their benefits and know their price estimates. Notably, despite efforts to integrate directly with pharmacy benefit managers (PBMs) to streamline copay estimates and claims, the largest three PBMs have yet to fully partner with Amazon, signaling ongoing resistance and complexities in data-sharing and transparency. Let’s just assume they’re worried about…API security.

Amazon has asked the PBMs for this access and all 3 of the big PBMs have “understood the request.”

Currently, Amazon Pharmacy serves approximately 1 in 4 customers through real-time benefit checks. Where they don’t have perfect information, the platform analyzes past claims data and other information to copays, leveraging machine learning to do so. Fascinatingly, simply by ESTIMATING copays for customers, Amazon learned they could improve medication adherence. Explain to me exactly why PBMs would be against that? (But really, if there’s a legitimate reason I’d love to know).

Amazon Pharmacy’s new offerings, PrimeRx, RxPass, and RxCoupon, illustrate Amazon’s consumer-centric approach across healthcare which has a simple goal: simplify, simplify, simplify. The team continues to recognize broken or failing aspects of the pharmacy value chain for the consumer. Quality of experience at the retail pharmacy is dismal. Mail order hasn’t evolved. So they set out a goal to get every U.S. citizen medication as quickly as possible, safely.

To that end, Amazon Pharmacy is scaling rapidly in logistical capabilities, integrating pharmacies directly into its vast logistical network to enable same-day medication delivery. By embedding pharmacies within distribution hubs, they’ve reduced delivery times from 2 days to 2-6 hours, launching services initially in urban hubs such as Seattle, New York, and Austin, with plans to build a new pharmacy operation every 18 days into major urban areas over the course of 2025.

I’m also pumped personally to hear the state of Texas approved drone delivery, which should only serve to increase medication access. But I’d love to eventually see these capabilities extend to rural areas.

In tandem with its logistical growth, Amazon continues to expand its pharmacy business through strategic partnerships, including a notable agreement with Eli Lilly as a dispensing partner and Blue Cross of California. Additionally, Amazon’s latest feature enhancements, like caregiver functionalities and Medicare-compatible payment options, directly respond to growing consumer demands for convenience, affordability, and transparency. When asking John how Amazon’s team prioritizes platform features, he noted they develop a composite score, involving the following questions and more:

- What’s the total potential impact of this feature?

- How can we improve medication adherence, access, and affordability? What are the edge cases?

- How much time is the consumer saving?

Amazon’s broader ambition remains clear: to fundamentally transform the consumer healthcare experience. With significant logistical strengths, Amazon Pharmacy seeks to remove administrative burdens – automating data entry, streamlining billing processes, and reducing pharmacy deserts.

- “We want the pharmacy to be as simple as shopping on Amazon is…make what should be simple…simple.”

In essence, Amazon Pharmacy’s expansion and innovative approach underline healthcare’s shift towards consumerism, and despite ongoing friction with major PBMs, the trajectory suggests continued disruption as Amazon leverages its considerable technological and logistical resources to reshape the patient pharmacy experience.

And it looks like incumbents are taking notice as consumers demand more from their healthcare services.

- “[Customers] really want to trust and engage with companies that have earned the right to be in healthcare,” [now-former CEO Karen Lynch] said. “I think about Amazon as sort of a transactional company today.”

- “We welcome competition.” – now-CEO David Joyner

This isn’t intended to be a CVS slam piece or an Amazon puff piece. It’s intended to be a …”who is making the consumer experience in healthcare better?” piece. And so far, it seems as if Amazon is doing a hell of a better job, but CVS has the immense incumbency and assets to deliver incredible impact.

Who do you trust more to ship for consumers in healthcare – Amazon, CVS, or neither?

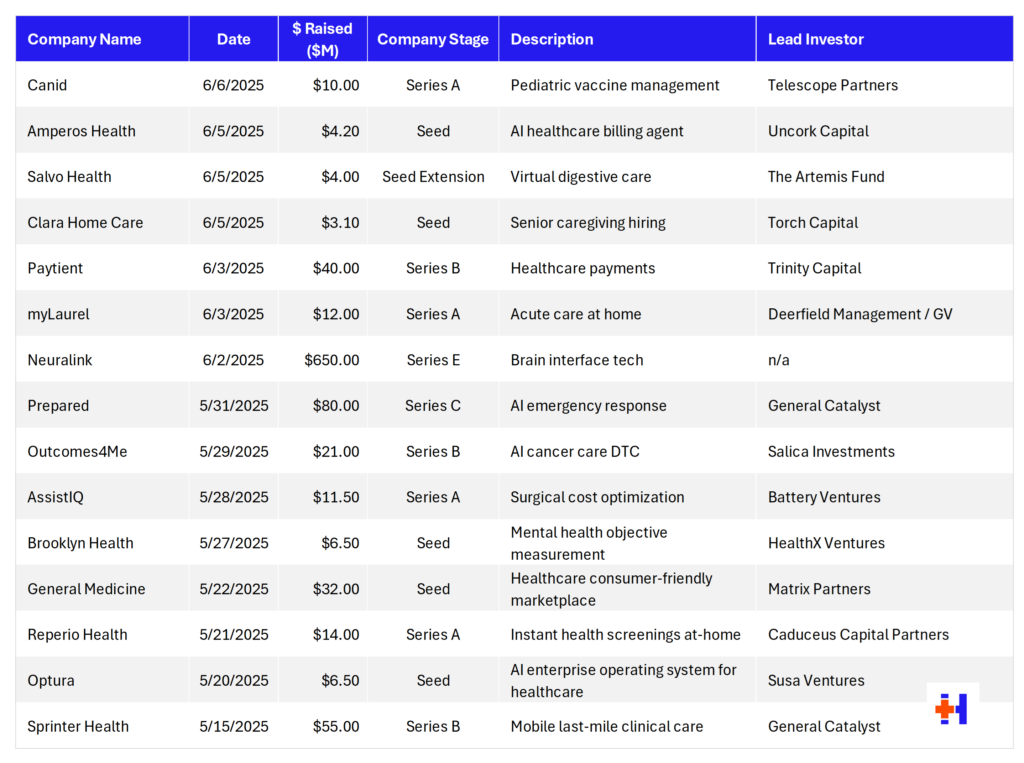

Health Tech Funding Summary