Physician Practice Employment Dynamics in 2024: The Latest Numbers

I shared a graphic and a brief blurb about this in last week’s newsletter but figured it was worth a deeper dive since the physician is a central figure hitting on so many trends and forces shaping healthcare.

In summary, physicians are consolidating, and are increasingly employed by health systems.

Here’s a quick breakdown, visualized by yours truly. And the full AMA report can be found here including methodologies and more color.

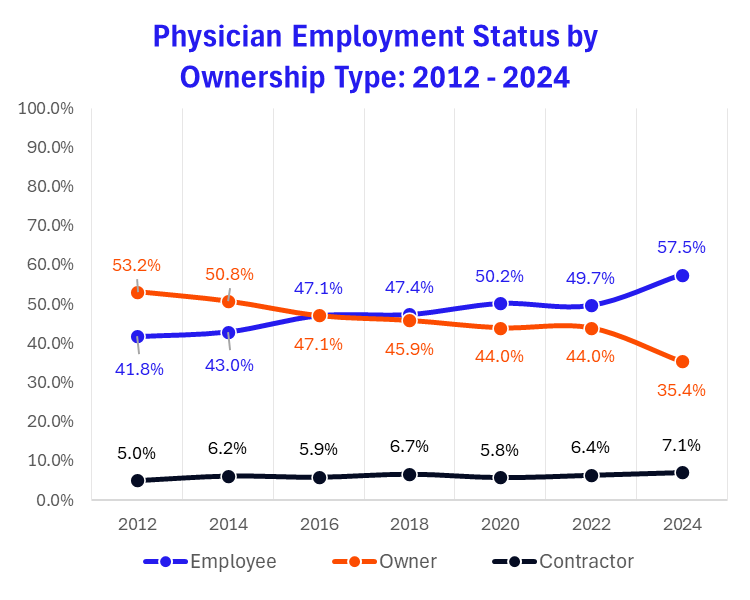

Insight #1: Fewer physicians than ever before are owners of their practice in 2024. It’s an interesting and noteworthy trend. The physician workforce is aging, and therefore many are retiring and selling their practices to PE and hospitals. Meanwhile, physicians just entering the workforce tend to be employed by hospitals and health systems, so it’s a double-whammy effect we’re seeing as hospitals are the primary driver of the increase in employed physicians and subsequent decrease in physician PRACTICE ownership. I would wonder about trends in ASC ownership, however.

Insight #2: Physician practices are consolidating into multi-specialty independent groups or being employed as hospital professional entities.

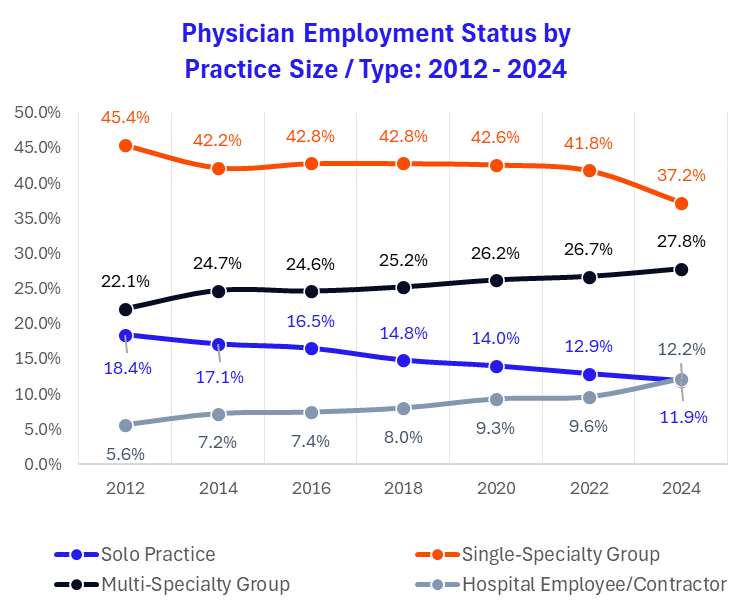

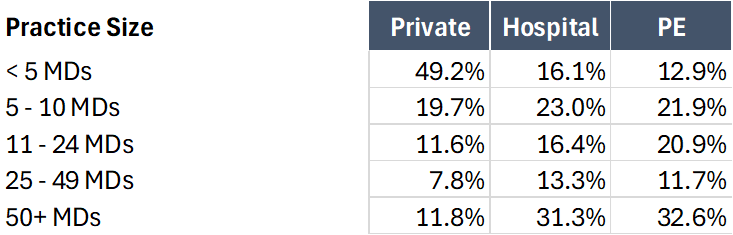

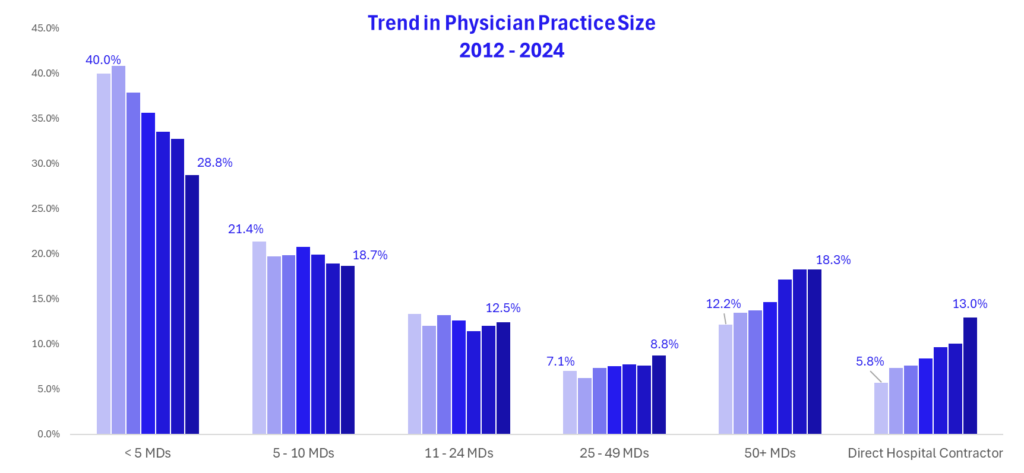

Insight #3: Similar to the above, practice sizes are either increasingly either really big, or really small. As hospitals and PE-backed groups are focused on cornering their respective local markets or specialties to drive higher rates, have greater coverage of important sub-specialists to corner payors, or provide more integrated care, these entities aggregate platform-level, large physician groups of 50+ MDs. Meanwhile the reverse is true in private practice, as you’d expect. 49% of private practices contain 5 or fewer physician, meaning there’s a long tail of fragmented physician practices STILL across the nation.

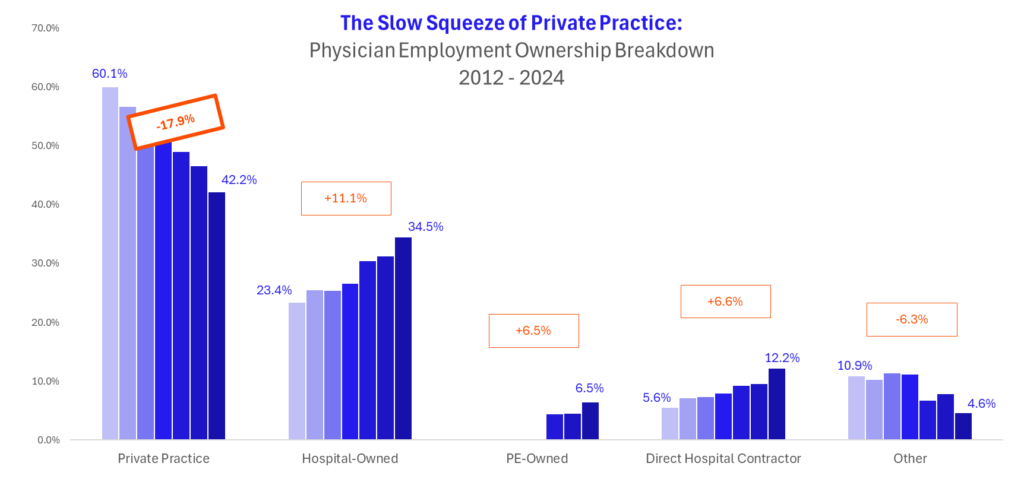

Insight #4: Hospitals and PE-backed groups are the primary beneficiaries of the private practice squeeze. As expense inflation, need for more expensive equipment, and inability to negotiate with larger payors continues, economics of healthcare favor scale and scale with density in particular – so, naturally consolidation happens.

Insight #5: Physician practices are getting bigger as strategics vie for scale in their markets. And the trend appears to have accelerated in 2024 as seen in the big dip in MDs < 5:

The Weekly Executive Summary

Notable moves, policies, and strategies from around healthcare.

Strategy, Finance, M&A:

- Omada’s Successful Public Debut: While the stock has sold off since, Omada notched a successful IPO, raising $150M and signaling stability for health tech IPOs to come.

- Duly Acquisition: Duly Health and Care acquired Alliance Clinical Associates to expand its multi-specialty outpatient network in the Midwest, adding 5 new clinical sites. A little bird told me Duly may not stay out of the news in 2025.

- Advocate Income: Advocate Health’s operating income jumped 217% in Q1, driven by strong patient volumes and improved cost management. What an incredible jump.

- Concentra acquisitions: Concentra completed its acquisition of Pivot Onsite Innovations, bolstering its workplace health and onsite medical services. The deal brings Pivot’s tech-enabled injury prevention and telehealth solutions into Concentra’s network.

- Rural Partnership: Homeward and Meijer launched a rural health partnership to bring primary care, chronic disease management, and social support services to underserved Michigan communities.

- Stonepeak Walks: Private equity firm Stonepeak reportedly walked away from a $1.9 billion acquisition of a national radiology group over valuation disagreements.

- Best Buy Health Impairment: Best Buy Health wrote off $109M mostly related to its healthcare acquisitions (presumably Current?). Probably signals slow decay of the promise of at-home care models, alongside the Dispatch-Medically Home merger.

- United’s Comms Snafu: UnitedHealth accidentally leaked a set of prepared talking points for executives to address investors. Whoops!!

Innovation:

- OpenEvidence and JAMA Partner: OpenEvidence and The JAMA Network signed a strategic content agreement to deliver peer-reviewed medical insights and clinical summaries to health professionals. OpenEvidence claims it’s used by over a third of doctors and 10,000 hospitals and medical centers nationwide, so it’s definitely a name to watch and a potential Doximity target, eh? Alright…maybe not at a $3B valuation.

- Khosla R1 Investment and Palantir Involvement: R1 secured growth capital from Khosla Ventures to accelerate its AI-driven revenue cycle and patient engagement solutions following the launch of R37 with Palantir (extremely notable development). Lotssssss of activity in RCM right now given the prevalence of AI use cases and consolidation plays

- Epic Launchpad: Epic introduced Launchpad, a new framework to help health systems deploy and govern generative AI applications within its EHR. The tool provides guided templates, risk controls, and performance monitoring for clinical workflows.

- Amazon Pharmacy Launches Support for Caregivers: Amazon Pharmacy introduced a caregiver support feature for Medicare PillPack customers, allowing designated family or professional caregivers to manage prescription orders and dose reminders.

Policy:

- ACO Reach Update: CMS released a quick-reference guide for Performance Year 2026 of the ACO REACH model, outlining updated benchmarks, participant criteria, and payment policies. What do we think about the sustainability and invest-ability of a program that raises the benchmark bar every year? Thoughts?

- Medicaid Utilization: KFF’s brief compares healthcare utilization among Medicaid expansion and non-expansion states, finding expansion leads to higher preventive service uptake and lower uninsured rates. The analysis highlights disparities in hospital and outpatient service use.

- Healthy America: The HHS unveiled its Administration for Healthy America to coordinate federal public health efforts and centralize programs across disease prevention, health promotion, and community partnerships.

- NIH Budget: The FY 2026 HHS budget proposal includes $2 billion in NIH cuts and reverses certain Trump-era healthcare regulations.