It’s currently 105 in Dallas, so I’d appreciate you sharing this newsletter with some extra friends so that I can foot my electric bill!

Want to get these in your inbox to never miss an edition? Subscribe to Hospitalogy today!

Primary Care Fire Sale

Several news stories dropped this week related to payors holding talks with publicly traded facility-based primary care platforms.

Shares of One Medical skyrocketed 22% immediately after sources reported that CVS, which has been on the hunt for a primary care deal for some time, was in talks to acquire (paywall – Bloomberg) the embattled primary care player. Apparently One Medical is still weighing potential acquisition offers to this day!

Just a day or two later, Humana was rumored to be eyeing a takeover of Cano Health, somewhat of a peer to One Medical focused on the Medicare Advantage space and primarily located in Florida. I should note that Humana also has the right of first refusal to any potential acquisition of more than 20% of Cano Health, so it makes sense that Humana would look into buying Cano after a steep drop-off in share price and valuation in the primary care facility-based players.

Along with these two players, the entire primary care platform industry saw a boost in stock price on the heels of the news:

- One Medical jumped 26%

- CareMax climbed 25%

- Cano rose 22%

- Oak Street increased 19% (I’m out of synonyms for ‘increased’)

- agilon and ApolloMed spiked (aha! fooled you) 16%

- Privia swelled 12% along with Teladoc

Madden’s Musing

It’s an interesting juxtaposition – these facility-based players seem to have a vast amount of untapped potential and value to be unlocked by being acquired strategically by a payor, yet at the same time, are heavily discounted in the public markets.

In a standalone business, the economics of value-based primary care platforms are tough. It seems to a long time to breakeven while transitioning patient panels. But assimilated into a payor? Lots of value to unlock there. Literally.

Facility-based VBC platforms are a FANTASTIC strategic asset for payors who can manage medical spend. For instance, Cano’s guided medical loss ratio in 2022 is around 76%! That’s insane savings to acquire for payors.

Keep in mind that Humana also has a MA-facility joint venture with Welsh Carson thru CenterWell to develop 150+ MA clinics by 2025.

Whenever one of these players gets acquired, I’ll be taking a deep dive into the acquisition!

Anotha One: Finally, I also want to note here that Premier Inc likewise spiked on reports of private takeover interest, although this flew under the radar quite a bit.

I predicted just a couple of weeks ago that healthcare assets at these valuation levels were pretty enticing for strategic and financial players alike. Looks like that prediction is rapidly approaching reality!

Want to get these in your inbox to never miss an edition? Subscribe to Hospitalogy today!

CMS cuts physician reimbursement

The new CMS proposed rule just dropped!!

On July 7, CMS released its proposed rule for the Medicare Physician Fee Schedule (MPFS), and it really was quite the mixed bag. Here are the highlights:

Join the thousands of healthcare professionals who read Hospitalogy

Subscribe to get expert analysis on healthcare M&A, strategy, finance, and markets.

No spam. Unsubscribe any time.

Conversion Factor Cuts: This was the big whammy from the release. The Conversion Factor (CF) is the basis for calculating Medicare payments to physicians. CMS is cutting this component by 4.42% – from $34.61 to $33.08. CMS basically went on to say that its hands were tied from increasing the CF as a result of statutes affecting Medicare, including budget neutrality & other nuanced stuff that kept the Centers from bumping reimbursement.

ACO Expansion: CMS wants to advance shared savings payments to new ACOs participating in the MSSP program to help address the social needs of Medicare beneficiaries in rural and underserved areas. The thinking is that by providing these payments, rural providers will get the investment needed to start their own ACOs. Changes in the proposed ruling would result in $650M in new shared savings payments to ACOs.

Behavioral Health: CMS proposed to allow therapists to practice under ‘general’ rather than ‘direct’ supervision by a PCP. On top of the intent to address behavioral staffing shortages, CMS wants to further integrate behavioral health into primary care by reimbursing behavioral clinicians linked to primary care practices.

Chronic Conditions: CMS wants to bundle certain treatments into per-month payments to encourage team-based chronic condition management.

Other Stuff: The smaller, more nuanced stuff relates to slight expansion for dental coverage for organ donors under Part B, changes to colonoscopy access and starting age of coverage to 45.

Madden’s Musing

Physicians are pretty dang upset about the ~4% cut headed their way (as are most services verticals when their reimbursement is cut in a draconian fashion).

Numerous physician organizations cried foul about the proposed rule. Here’s a quote that sums up the sentiment quite tidily:

“The cost of running a medical practice has increased 39% in the past twenty years. When adjusted for inflation, the impact is a decline in value of Medicare physician payments of 28%. On top of jeopardizing patients’ access to care, the proposed cuts further exacerbate the difficult operating environment surgical practices already face and the people that are affected most are our patients.” – George Williams, MD, American Academy of Ophthalmology Senior Secretary for Advocacy

They’re right to be upset. We’re facing a bizarre dichotomy in healthcare today.

On one hand, expense inflation is vastly higher than historical norms. It’s hitting costs across the board (supplies, staff, utilities, G&A components).

No services vertical is immune to inflationary effects facing the U.S. this year and pricing power is more limited in healthcare in general as payors apply deflationary pressures on provider top lines. (I wrote about this effect back in April – in fact, it was one of my first ever Hospitalogy sends. OGs will remember!).

At the same time, CMS is hamstrung by statutory requirements to keep Medicare budget neutral along with other measures in place aimed at keeping the trust fund afloat.

It IS ironic to me, though, that CMS touts expanding access throughout the fact sheet release despite the fact that it was just forced to cut reimbursement in physician services, quite literally the most integral vertical for patient access. I think CMS is well intentioned, but the statements struck me as contradictory.

If I’m a physician or any service provider, my main beef is with Congress right now and its lack of an answer to provide funding despite unprecedented levels of government spending over the past 2 years.

We’re witnessing a massive swing in physician employment to corporate entities & hospitals right in front of our very eyes mostly driven by legislation (or lack thereof) propagated by buffoons. Independent physician groups are struggling to survive. Meanwhile, continued consolidation will drive prices higher, ironically resulting in dire financial straits for the Medicare Trust Fund.

TL;DR: AHA > AMA, and healthcare continues as always to be a consolidation game. It’s already hard enough to be a provider. Let’s not make it harder.

If you have a different perspective, I’d love to hear your argument or thoughts!

Resources:

- CMS proposed rule fact sheet press release

- Physician trade group responses to the proposed MPFS ruling

- A good read published Friday on the integration of behavioral health and primary care

Want to get these in your inbox to never miss an edition? Subscribe to Hospitalogy today!

Market Movers

In the upper Midwest, Bellin Health and Gundersen Health are expecting to complete a potential merger in what would create an 11-hospital and 100 clinic system across Wisconsin, Upper Michigan, southeastern Minnesota, and northeast Iowa. The two systems would generate $2.4B in annual revenue across 14k FTEs assuming it gets past FTC approval, which is sure to check for market concentration, impact on wages and employment, and everything in between. Here’s some more background on the deets.

Prime Healthcare, a 14-state, 45-hospital for-profit system, announced a partnership with Robotics Outpatient Center LA to offer certain robotic procedures. Another relevant tidbit from the presser: “Over the next year, Prime intends to joint venture with more ambulatory surgery centers to ensure more efficiency, appropriate care for patients, and significantly reduce healthcare costs as a nation.” In other news, grass is green.

I need yall to read this press release. P3 Health Partners, a care platform I briefly covered in a deep dive in May, dropped a press release related to their ‘multi-year relationship’ with …the Oregon State University Senior Cheer Squad. Along with other sports. I mean, I’m reading this thing thinking that P3 is about to drop an amazing partnership announcement and instead…I’m left questioning what the heck is going on over there!

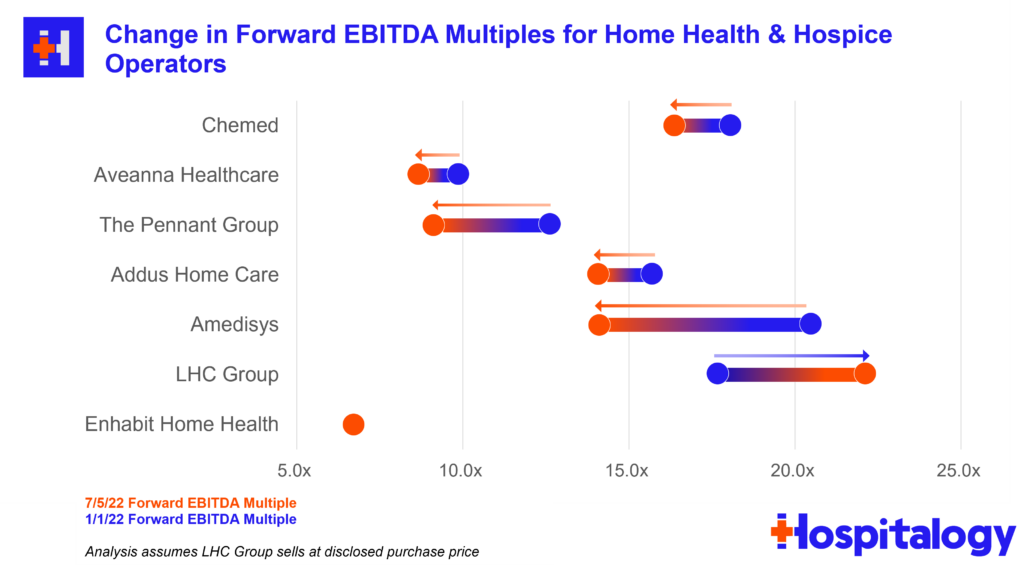

Home health multiples continue to be hammered given the current macro outlook for these operators. This week, Aveanna was downgraded by equity analysts and dropped another 7%. Meanwhile, Enhabit (Encompass spinoff) continues to get hammered and dropped under a $1B market cap while trading at a sub-7x EBITDA multiple. Check out the graphic below and make sure to share Hospitalogy with as many friends as you possibly can so that I can keep making fire analyses (and afford electricity).

Signify Health announced its intention to wind down its Episodes of Care segment. With the wind-down, Signify is leaving CMMI’s BPCI-A program, which as it turns out, was a well-intentioned flop. There were some interesting inflation-related quotes in the press release as well, including:

- “The Company’s timing and decision to terminate its participation in the BPCI-A program is driven by recent policies implemented by the Center for Medicare & Medicaid Innovation (CMMI) affecting BPCI-A pricing that the Company and its clients believe have rendered the program unsustainable.”

LHC Group shares dropped below UnitedHealth Group’s takeover price of $160 after the FTC requested additional data from the merger related to employee pay. For those paying attention, the FTC is now looking into Optum’s acquisition of both LHC and Change Healthcare the latter of which you should be more concerned about. My money is on the LHC deal going through without too many more hiccups, but the FTC has had quite a bit more bite lately in healthcare.

- On the UnitedHealthcare note – keep an eye out for their earnings dropping on Friday. They always kick off earnings season and it’s a good one to read / review given how many different parts of healthcare UNH touches. Earnings season comes as insurers like Humana and Cigna touch or near all-time highs…in this economy!!

Teladoc expanded its Primary360 offering this week. The whole-person virtual primary care platform is now integrated with fellow digital health players Capsule (digital pharmacy) and Scarlet Health (lab testing / diagnostic collection & delivery). At a stock price just above its IPO, Teladoc could be at compelling levels…unless you think the encroaching digital health players are too much to withstand.

Babylon announced a cost reduction strategy to accelerate its path to profitability. If you’re still stuck holding the Babylon bag, I feel bad for you son. I got 99 problems, but a mismanaged value-based care chart crimer ain’t one!

Cardinal Health acquired the Bendcare group purchasing organization entity and made another minority investment in the Bendcare MSO. It looks like Bendcare is a specialty practice management organization and if memory serves, there has some recent M&A interest in GPOs given global supply chain struggles and inflationary pressures.

Despite everything in the markets, Akili Therapeutics is still prepping to go public via SPAC later this year, appointing board members and moving forward business as usual. The deal was originally announced in Jan ‘22

Rev cycle management digital health firm Cedar laid off 24% of its workforce this week

Miscellaneous Maddenings

- Elon had himself a week – he had twins with a coworker and now he’s trying to get out of his merger agreement with Twitter. Shenanigans you can take part in when you have more money than Caesar.

- Today I learned that nifty is short for magnificent!! Who knew?? (Don’t lie, you didn’t know)

- Zach Wilson is uhh..apparently into older women.

- Elizabeth Holmes’ former lover and apparent mastermind Sunny Balwani was found guilty on ALL 12 charges brought against him in the Theranos suit!

Hospitalogy Top Reads

- Tejas Imandar concluded his fire PBM series by dropping his third and final part this week focused on current issues and the players involved. Drop him a sub so he stays motivated to keep writing great content!

- I wanted to share a great new resource from Xander Kerman and the team at Syntegra. Syntegra, a data analytics firm focused on democratizing healthcare data, just launched a new data resource. Data’s always been tough to access for many reasons, both good (privacy) and bad (territorialism, fear, commercial interests, & technical incompetence), which holds back innovation that could and should change lives. A new resource aimed at addressing these access challenges just went live — Syntegra is making privacy-preserved, patient-level, synthetic healthcare datasets, trained with advanced ML from real clinical data, freely available. Download the EHR and claims datasets today, in the most commonly used data formats. One more thing: help Syntegra understand how you plan to use the data in a brief survey, and they’ll send you a $25 Amazon gift card.

- The Frontier Psychiatrists wrote a fair assessment of the Cerebral saga, diving into specific behavioral health nuance that I appreciated. While the assertion that Cerebral expanded access and on a relative scale limited patient incidents is fair, I would go further to argue that the whole point of venture-backed mental health startups should aim to improve the standard of care, which in my mind is still lacking in Cerebral’s model.

- Alan Soclof, a colleague of mine at Workweek writing the Crossover, dove into the world of scrubs and the business viability of FIGS

- Jared had a great write-up last week on unwarranted clinical variation – if you’re not subscribed to Healthcare Huddle idk what you’re doing!!

Want to get these in your inbox to never miss an edition? Subscribe to Hospitalogy today!