Welcome to the first edition of Hospitalogy in 2023! Parth Desai and I have been jamming on some thoughts on where healthcare might be headed in the new year.

Based on discussions with industry folks, market signals buried in earnings and disclosures, and our often misguided internal dialogues, here are some of our predictions for healthcare in 2023.

Join 13,000+ executives and investors from leading healthcare organizations including HCA, Optum, and Tenet, nonprofit health systems including Providence, Ascension, and Atrium, as well as leading digital health firms like Tia, Carbon Health, and Aledade by subscribing here!

Behavioral health phoenixes: the category redefines itself, with a focus on I/DDs

As the broader behavioral health care market grows more crowded and patient acquisition costs climb, we expect to see care providers diversify their service offerings and invest in specialized services for more complex patient populations (serious mental illness, neurodivergent populations, seniors).

Specifically, intellectual developmental disabilities will emerge as the top behavioral health priority. It’s estimated that 1 in 6 children has an intellectual developmental disability and prevalence rates have been rapidly increasing. The complex needs of this population drive total public spend on care that exceeds $65B annually, largely covered by Medicaid. And given this complexity, the I/DD population has been amongst the last to transition to managed care.

However, expect this to begin to change next year. In the last 18 months managed care spending on I/DDs (particularly Autism Spectrum Disorder) has increased by as much as 150%, as a result of access constraints and reimbursement policy changes borne out of the pandemic. It’s no surprise that a quick search for “autism” on any government RFP database shows a 50% increase in posted bids over the last 12 months.

A resurgence in applications of AI for healthcare will finally be matched by accelerated adoption

We’ve long celebrated the enormous potential that artificial intelligence has to transform healthcare workflows; however, adoption rates to match the interest have yet to materialize. There are many reasons for this, but at its core, the data infrastructure to scale algorithm development has been nascent. This began to change in 2022.

This year, we’ve seen the launch of a handful of promising early stage companies with creative approaches to solve data infrastructure limitations. Additionally, larger companies like Snowflake, a pre-eminent data platform to support AI development, doubled down on healthcare this year, signaling that the sector, already one of its largest growth verticals, is expected to continue growing. Databricks, another pre-eminent data platform enabling AI development, announced a competing healthcare data lakehouse around the same time. As healthcare organizations continue to invest in improving their data infrastructures, AI development and the adoption of new applications is bound to follow.

Some interesting signals of growing adoption are scattered across recent earnings reports, such as Microsoft’s strong reported growth in its healthcare AI solutions segment, Pfizer’s AI-driven R&D breakthroughs, or even the continued steady growth of healthcare’s largest cloud data providers, Amazon Web Services, Microsoft Azure and Google Cloud Platform this year. Current buzz around the potential applications of new large language models and generative AI are likely to fuel further interest and adoption.

A Tale of Two Health Systems

As we are all aware, health system financial distress is real, but more real for some versus others. For instance, small to mid-sized health systems with limited economies of scale are likely to continue get squeezed by rising costs (contract labor), and less leverage in commercial rate negotiation.

On the other hand, large systems should rebound in 2023. HCA, Tenet, and the large nonprofits will continue to successfully negotiate commercial contracts to the tune of 5-7% rate lifts per year. As we’ve seen in the last couple of quarters of earnings, they will also have more success lowering contract labor and travel nursing costs through an elevated focus on nurse retention (market $$ adjustments, nursing task forces, equity programs, bonuses, and more). When labor comes back online, utilization will follow.

We also expect inter-hospital alliances like Truveta, Evolve, and CivicaRx to also evolve. More alliances will form in 2023 likely around expense management efforts (staffing, group purchasing power). Hospitals will also look to outsource other functions to specialized providers (lab, physical therapy, revenue cycle management).

Finally, expect cross-market mega-mergers to become the norm for the future of health system M&A. M&A is less and less feasible in the current political environment and the FTC is shutting down local market M&A (see: HCA-Steward, Saint Peter’s-RWJBarnabas, and Lifespan-Care New England in 2022). The old method of hospital mergers for rates & monopoly-esque plays are not really on the table anymore – at least not with the current administration nor with the media attention that nonprofit hospital practices are drawing as of late.

Despite challenging market dynamics, hospitals will be among the most active buyers of HCIT

The financial and operational challenges that hospitals are encountering have been a widely covered topic. While this might suggest budget constraints in 2023, in fact, the majority of hospitals expect to increase their investment into information technology next year.

Expect hospitals to prioritize solutions that create directly attributable top and bottom line ROI addressing revenue cycle, contact center / patient intake and value-based care operations. Fast integration timelines and interoperability will be rewarded. Its no surprise that across a universe of roughly 90 publicly traded healthcare IT, services and managed care companies, 4 of the top 10 fastest growing companies (based on 2022-2023 forecasted revenue growth rates) are HCIT companies focused on hospital revenue cycle, patient intake or value-based care.

Vertical Alignment = Healthcare Domination

Vertical alignment is and will continue to be the name of the game over the next decade, and things are already unfolding in this direction.

Join the thousands of healthcare professionals who read Hospitalogy

Subscribe to get expert analysis on healthcare M&A, strategy, finance, and markets.

No spam. Unsubscribe any time.

The ‘Payvidor’ space will be a key area to watch for healthcare organizations entering 2023. Managed care giants have steadily been tracking and emulating UnitedHealth Group (which has a major head start) over the past 10 years with Optum and its 70,000 physicians. Over 2022 and entering 2023, payors are actively working to expand their clinical footprints across physician practices and associated ancillaries, ambulatory surgery centers, virtual healthcare, behavioral health, and home health (Optum-LHC, Optum-Refresh, Optum-SCA Health, Humana-CenterWell/Kindred).

Major payors are now creating their own versions of Optum with full services functions across pharmacy, benefits management, healthcare services, and technical infrastructure to avoid becoming pass-thru’s just used for sub-capitated contracts to providers taking on risk.

- In March 2022, Anthem rebranded to Elevance and set up a new services entity, Carelon

- Likewise, Cigna’s Evernorth now includes its pharmacy benefit manager Express Scripts while Cigna Medical Group rebranded to Evernorth Care Group under a strategic rebrand.

- Later in September, Humana announced a similar organizational restructure, rebranding Kindred at Home to CenterWell Home Health. Humana also has existing partnerships in place with Welsh Carson to expand its primary care and senior clinic presence.

Policy and technology will finally converge around elevating the role of non-physician providers in care

Healthcare’s workforce issues are disrupting every aspect of care delivery from providers to post-acute facilities to life sciences R&D operations. While wage increases and outsourced services have been the solution thus far, the reality is that these are temporary fixes to systemic issues that are expected to worsen. This is particularly apparent when considering the physician to patient supply-demand imbalance.

While technology holds some promise in unlocking incremental physician capacity, it’s clear that a growing supply of non-physician care providers will fill the majority of the latent capacity needed to service future care demand. However, regulatory challenges and supply imbalances, among other challenges, currently limit the availability and utility of many of these providers. So in 2023, expect to see policy changes that evolve scope of practice for nurses, ancillary care providers and public health workers and emerging technology that empowers non-physician care providers to play a larger role in the workforce.

Risk Trickles into More Areas – Specialty Care, Commercial

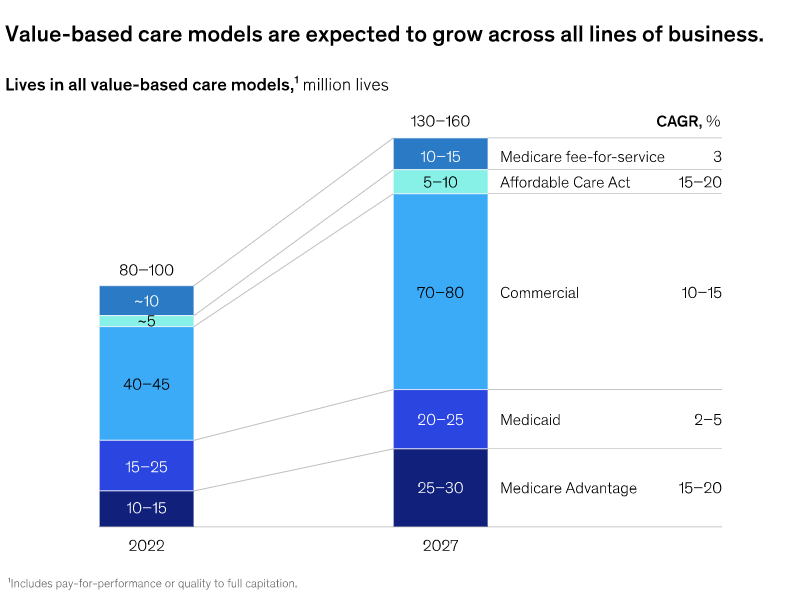

It’s only natural that specialty care and commercial, employer sponsored insurance become the next frontier of value-based care. Expect to see risk-based contracting evolve in 2023, particularly in specialty care areas like oncology, cardiology, and MSK. Along with these specialties, ambulatory surgery centers will see innovative payment models, including higher levels of price transparency and cash pay for services. Further, tech enabled services providers like Crossover are piloting value-based care arrangements in commercial plans.

At the same time, UnitedHealthcare is offering a variable copay plan called Surest with 15% lower premiums and a variable copay based on clinician quality, which we would expect to be an attractive plan for employers. We’ve heard anecdotally that risk-based contracting outside of Medicare Advantage may get quite creative, so we’re excited to see how the space evolves now that things really seem to have taken off post-pandemic.

Finally, take a look at what Optum is doing and what it did in 2022 – it quietly rebranded Surgical Care Affiliates, its specialty care segment, into SCA Health to ‘support growth into many aspects of specialty care’ like transitioning specialist practices to primary care and even pursuing risk-based contracting in the ASC setting. As Optum does, healthcare follows. McKinsey is expecting the Commercial value-based market to grow as well:

As healthcare delivery evolves, expect to see hybrid care models become table stakes for services companies. We’ll see both new and incumbent services firms adapt to this new normal. Virtual care solutions will enable brick and mortar clinics to provide better care at lower costs with higher patient engagement. Hybrid care is the best version of healthcare with services and in-person care complemented by telehealth, remote patient monitoring, and more.

The Biosimilar Boom will Accelerate Pharma’s Shift to Digital

2023 will usher in a new future for the life sciences industry, with 7 FDA-approved Humira (adalimumab) biosimilars waiting to launch in the United States and potentially more to follow. Given that the 22 biosimilars launched in the United States to-date have created an estimated $21B in cost savings, the additional potential cost savings of these new biosimilars could be substantial. And with another 96+ biosimilar development programs in progress targeting a range of therapeutic areas, the next decade promises additional growth.

Despite significant cost savings potential, coverage and prescribing policies (and therefore uptake) for biosimilars are still evolving. Key to these efforts is prescriber education and engagement, which has been disrupted by the pandemic, accelerating a trend away from in-office sales rep driven engagement to digital modalities. Expect an evolution in marketing and education campaigns to drive biosimilar adoption efforts in 2023. This will include innovation in digital prescriber education, real world data efforts to support formulary coverage and digital patient-centered education campaigns.

Now for some fun ones

I (Blake) wanted to include a few way-too-specific predictions on possible moves in healthcare and health tech this year. Here are some spice and one-liner predictions!

- Between AWS healthcare moves and One Medical’s EHR, Amazon moves toward competing with Epic and Oracle-Cerner.

- Amazon makes moves similarly to Walmart-United to tap into the Medicare Advantage space.

- Teladoc merges with a brick and mortar player and/or makes another acquisition to expand its services and value prop to health system players, employers given post-pandemic struggles, Livongo flop. BetterHelp struggles but outperforms other DTC mental health players financially.

- At least one high profile PE-backed healthcare organization declares bankruptcy and/or restructures further. ER physicians and potentially other saturated consolidated spaces begin to depart from employment arrangements as equity value shrinks. We hit peak employment in the physician space. There’s an insane, intense fight over the No Surprises Act because of these dynamics.

- Almost 90 percent of the healthcare companies rated at “B3-” or below are owned by private equity groups. Of the 34 such companies, approximately 38 percent are hospital or healthcare facility providers.

- Several small health systems restructure finances with bondholders or sell off in a fire sale.

- Hospitals get less relief at the federal level but more funding at the state & local level (jobs are a helluva drug).

- UpHealth, Babylon, Cano Health, P3 Health Partners, and Bright Health all get taken private, cease to be public, or are acquired. Cigna acquires Bright for the tax benefit.

- More venture capital partnerships with health systems take shape and grow more sophisticated in structure.

- Cerebral manages to successfully re-pivot as a major mental health player and outlasts the bad media coverage.

- Medicaid redeterminations will be discussed ad nauseam in 2023 but won’t actually matter/take place until 2024.

- Digital health infra companies selling into other digital health firms will either have to move upstream or get squeezed as cash tightens up this year.

- With ACO REACH, value-based care players differentiate themselves between contenders and pretenders in the space. After extremely poor DCE performance and a major scale back in members for ACO REACH, Clover pulls out of ACO REACH altogether by the end of 2023.

- We see at least one health system mega-merger by mid 2023 similar in structure to Advocate-Atrium.

- (Given by a subscriber): Privia enters at least two more markets with health system partners.

- (Given by a subscriber): CVS begins a ‘build’ strategy for primary care and engages with a notable private equity partner to do so (a la, Humana – WCAS and CenterWell).

- Blake’s Comeback public operators of the year in 2023: Tenet, Surgery Partners, Augmedix,

- Blake’s Best performing healthcare stock guesses in 2023: Doximity, Acadia, InnovAge

- Blake’s Worst performing healthcare stock guesses in 2023: Staffing firms (AMN, CCRN) as competition for attracting labor, investment in the space among PE, venture heats up

That’s it for our 2023 predictions! Let us know what you thought, hit us with your predictions, and I’ll include some of the spiciest takes in next week’s send!

Join 13,000+ executives and investors from leading healthcare organizations including HCA, Optum, and Tenet, nonprofit health systems including Providence, Ascension, and Atrium, as well as leading digital health firms like Tia, Carbon Health, and Aledade by subscribing here!