Pain sucks.

Right now, billions of people globally deal with pain on a daily basis. I personally dealt with a ton of excruciating pain when I broke my tibia and fibula as a senior in high school (no, I won’t show you the x-ray, orthopods).

So it goes without saying pain management, physical therapy, chronic disease management, and more…hold massive whitespaces for companies to tackle, and digital health players have entered these spaces in droves, raising huge sums in the post-pandemic feeding frenzy:

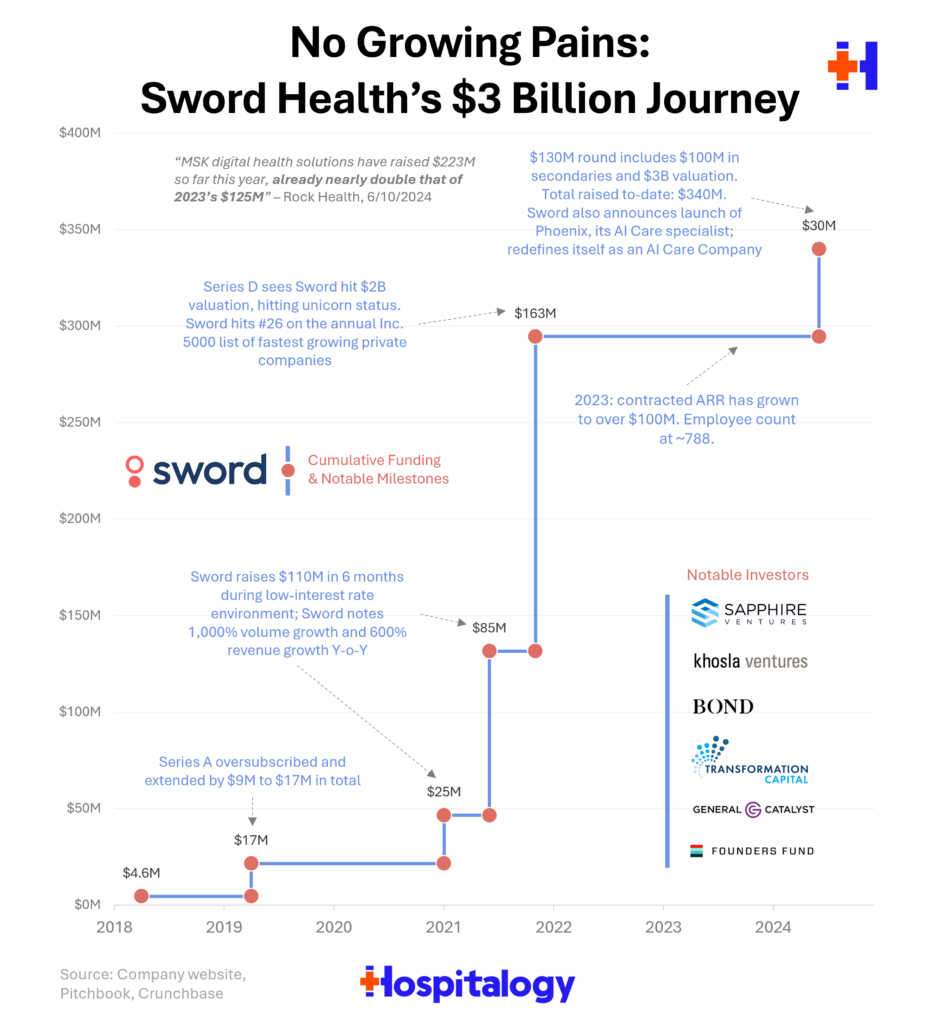

- “MSK funding grew six-fold between 2020 ($236M) and 2021 ($1.4B), as virtual MSK clinics Hinge Health ($300M and $400M) and Sword Health ($25M, $85M and $163M) each completed multiple raises across the year.” (Rock Health)

But most recent was Sword Health’s AI launch and fundraising announcement, and this one caught my eye for several reasons. The firm, led by Virgílio “V” Bento is on a journey to free 2 billion people from pain.

“Outcomes reporting and funding momentum are paving the way for continued investor and market attention—MSK digital health solutions have raised $223M so far this year, already nearly double that of 2023’s $125M.” (Rock Health)

I reached out to the Sword team this week and asked them a few questions around their team’s vision, strategy, and even company culture. They were gracious enough to respond on a quick timeline and indulge my creator procrastination.

Here were some of my more notable takeaways:

- Not just an MSK company. Sword really wants to differentiate itself and pull away from the idea it’s more than MSK. They’re focused on more than physical pain. So the plan from here is…let’s continue to go deep vertically on MSK and related conditions, but also horizontally into other chronic conditions. They’ll lean into AI to power care delivery at scale, self-describing their firm as the pioneer of AI Care (and has delivered 3 million+ ‘AI sessions’ to members to-date). A bit on the nose in 2024? Maybe, but I can appreciate the boldness.

- The team has learned from the digital health graveyard. Sword has been more thoughtful around growth, shying away from burning its cash irresponsibly, yet still growing impressively to 800 individuals and, as of August 2023, a $100M contracted ARR. Today after the June round, Sword has an extra $30M+ in the coffers for a rainy day, collecting interest and created some goodwill for its employees via a nice liquidity event.

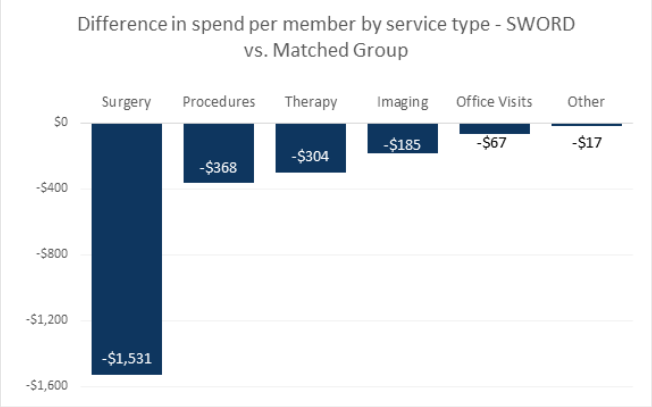

- Sword has a comparable, if not superior product to traditional PT. Of all the tech-enabled services verticals, virtual MSK in particular arguably holds up the best from a clinical rigor standpoint. The Peterson Health Technology Institute more or less corroborates this in its recent virtual MSK solution evaluation. Adding to clinical evidence and good outcomes, adherence to a PT program tends to be higher with a virtual MSK solution (as compared to in-person), Sword’s NPS is 74+, and also…interestingly…Sword contractually guarantees with employees the firm will save its clients money, attributing savings generally to the below categories (most notably surgery prevention)

- “Since 2010, more than $4.2B of venture capital has been invested in companies in the MSK space, and the value of transactions in the space has totaled $38.2B”

- “Sword has the largest base of clinical evidence among any solution evaluated in this report.”

- “Studies by Hinge and Sword compose the bulk of clinical information in the physical-therapist guided solution category, with only Sword providing prospective interventional trials within-person PT as the control.”

- Peterson Health Technology Institute Virtual MSK Health Technology Assessment

- Oh and finally…Sword will be profitable by the end of 2024. A private digital health company, launched during the pandemic, profitable by the end of the year. It’s hard to believe.

Over the course of 2024, Sword plans include continuing to innovate at scale, addressing pelvic health issues in women, and balancing growth with quality. As Sword often likes to say, they’re only 5% done!

About that Valuation…

This probably sounds a bit like a puff piece, and it is, to some extent. I’ll be honest, hand up. I want better solutions for folks, and a better patient experience. As a millennial, I want more convenient, streamlined PT and pain management. And I want that for every facet of healthcare. I know – I sound like a naive optimist. But Sword Health was exciting to learn about and hear from, and it’s delivering a good product for patients while catering to what employers and health plans want in a contractual relationship. As a result, Sword is benefiting financially. Love to see it.

Here’s my final burning question: will Sword Health overcome the digital health valuation conundrum? I can’t help but bring up valuation as a former valuation guy. It’s like a reflex for me. And I’m jaded from the Health Tech 1.0 companies. The companies that went public in the frothy public market environment and were crucified for their absurd multiples and inability to execute.

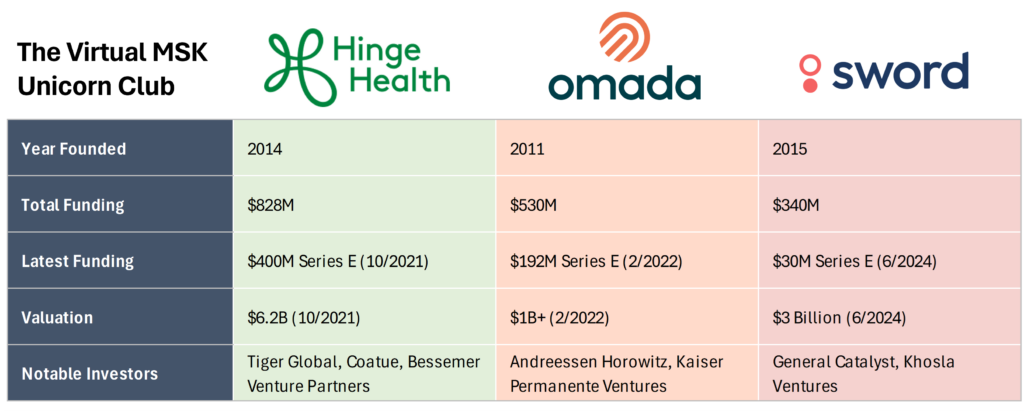

My logic is as follows: Sword privately is worth $3B today…at or around $100M in annual recurring revenue (assuming this is still correct from that mid-2023 graphic). If you do the math, that’s a hefty multiple, with quite a bit of forward growth baked in.

For an imperfect comparison (I know, tech-enabled versus traditional, Sword is more than MSK, yadda yadda – I’m sure many a VC will still scoff at this comparison), U.S. Physical Therapy – a publicly traded, traditional provider of PT services – owns and/or operates 670 or so PT clinics and generated $605 million in revenue in 2023, growing at a 9% clip. As a mature PT player, USPT is worth $1.7B and trades at 2.7x forward revenue. The delta is significant. That’s all I’m saying.

Is this time different? Will Sword grow into that valuation, or is the virtual MSK space a commodity? Today, the firm is growing like the 15-year old basketball child prodigy of a couple of D1 athletes. Since inception over 3 years ago, the firm has grown at an overall, sexy 11,000% clip. The perceived growth runway from this point is incredibly long. Can Sword continue to deliver an AI-enabled, scalable virtual solution to 2B people globally? The promise of AI here delivers a hefty promise.

If so, Sword is worth well over $3 billion.

Sword has clearly attracted a ton of investor interest, even in a tough fundraising environment, and I’ll take that as a market signal that its AI solution validates the valuation. I’m looking forward to following along Sword’s AI-enabled Care journey, and hopefully one day soon we’ll have another public digital health company to analyze. Here’s hoping this upcoming batch of Health Tech 2.0 firms have learned well from their predecessors.

Just keep in mind that private, VC-backed valuations (and most valuations, to be sure) are more art than science!

Join the thousands of healthcare professionals who read Hospitalogy

Subscribe to get expert analysis on healthcare M&A, strategy, finance, and markets.

No spam. Unsubscribe any time.

Thoughts? Opinions? Hot takes? Hit me with them anytime on my newsletter, Twitter, or LinkedIn.

Resources & Research:

- Vital Signs, Ep 45: Sword Health CEO Virgílio (“V”) Bento on Sword’s New AI Solution and the Decisions That Shaped the Company – Spotify link ; Apple podcasts link

- PHTI discusses their Virtual MSK Solutions.

- PHTI provides an Executive Summary.

- PHTI offers a detailed Assessment Report.

- Validation Institute evaluates Sword Health in their final report.

- ArcBest saves $850K by reducing MSK pain in this case study.

- Nature explores digital MSK care in this article.

- Sword Health is on Inc. Magazine’s Fastest Growing Companies List.

- Sword Health raises $85M in Series C funding.

- Sword Health reaches a $2B valuation with a $163M raise.

- Sword Health introduces Phoenix.