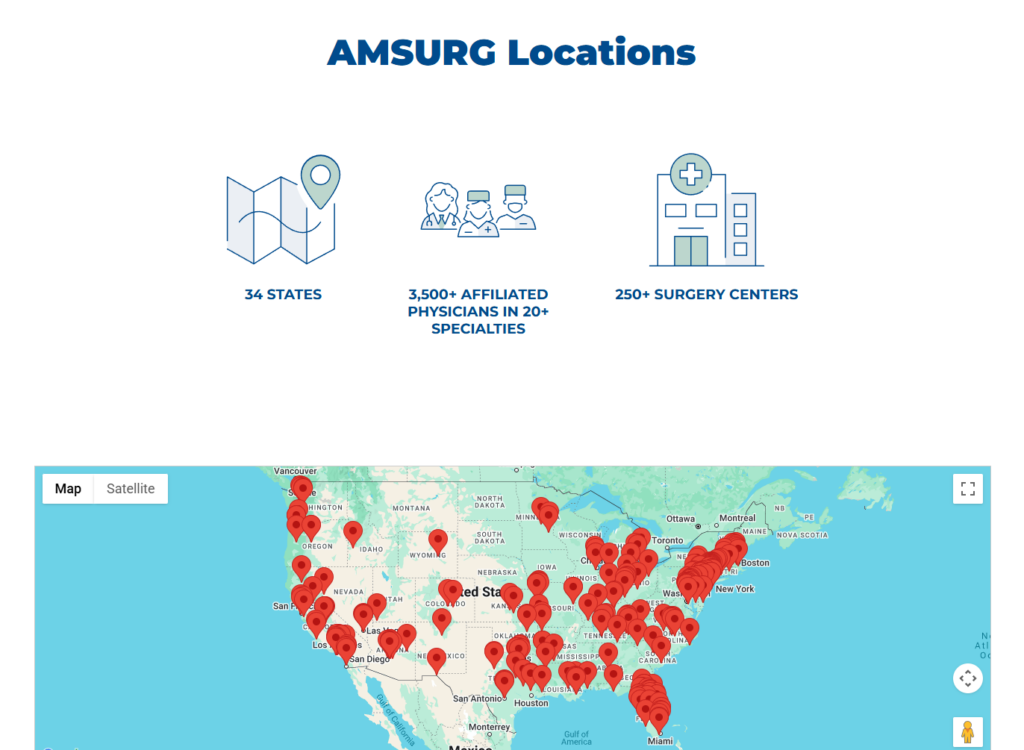

Ascension Rumored to be buying AmSurg in $4B move

After emerging from bankruptcy by an investor group not necessarily looking to hold a healthcare asset for the long-term, AmSurg is on the market. And per Bloomberg, a nonprofit health system with $27B in annual revenue – Ascension – is in ‘advanced talks’ to acquire AmSurg for a rumored $3.9B. The move would mark the largest M&A deal in the ambulatory space in some time, and echoes Tenet’s strategy involving going all-in on USPI – something that has benefited its enterprise quite a bit in recent years as it de-levers its balance sheet and moves outpatient.

In fact, when looking at strategic moves over the past 12-18 months, Tenet and Ascension’s deals have rhymed pretty heavily. While Ascension has gone on a selling spree divesting struggling hospitals and non-core assets (including additional sales of 4 hospitals and associated assets to Beacon Health in 2025 and a small but notable acquisition of Cedar Park Med Ctr in Austin, Texas), Tenet has likewise sold some of its hospital portfolio – but more from a position of strength rather than one of necessity, filling its balance sheet for the right opportunity.

So for that reason, that Ascension would be the winning bidder surprises me. Wouldn’t this process have been pretty competitive given how scarce of an asset a scaled independent network of ambulatory surgery centers is? Is Optum shying away from M&A given the problems at home? What about HCA, or Tenet and USPI themselves – was the valuation too rich? More focus on de-novos and tuck-ins? Bad cultural fit? Or is Ascension overpaying in a desperate attempt to eventually get out of the red? Ascension received a credit downgrade from S&P, while Moody revised its outlook to ‘negative’ – both in late 2024.

No matter the reason, Ascension needs to continue making moves, and its intent to transform its operations is clear. Through an AmSurg acquisition, Ascension gets immediate value accretion through what I expect to be higher ASC rates (note: not HOPD conversion), shared staffing and resources, broader physician alignment within its network, and potential new market entrances.

This move hits on the major themes playing out with hospitals and health systems today: adapt or die. Diversify, scale with appropriate density, and compete for margin on the ambulatory side. Feed the mother ship (inpatient, HOPDs) with higher acuity volumes.

Virta Health’s GLP-1 Guarantee, and catching up with CEO & Founder Sami Inkinen

Chronic disease companies are having a moment. And Virta Health, under the helm of Sami Inkinen & team, is on a mission to reverse chronic disease. Not just manage chronic disease – reverse it altogether.

This week the Virta Health team announced a GLP-1 utilization guarantee for its employer and health plan partners, meaning that the firm takes on the financial risk for all growth in GLP-1 utilization at a time when utilization in the drug class is growing 100%+ across the nation. To me, that seems insane, but to Virta, they’re fully bought in on the effectiveness of their model, and they seem to have the data to back it up:

- Virta is the only nutrition-based solution clinically proven to match or exceed GLP-1 weight loss, with members losing 13% on average at one year in a peer-reviewed, clinical trial—comparable to the 10–15% from drugs like semaglutide. This provides members with options to achieve lasting results with or without GLP-1s, and in turn enables employers and health plans to get the most out of their medication investment.

The bigger trend here is that there exists rampant demand for weight loss drugs, and employers and health plans are scrambling to find ways to manage utilization of GLP-1s. For coverage of GLP-1s, there’s no longer a question of SHOULD we cover these drugs – it’s now how do we RESPONSIBLY cover these drugs. But costs and utilization dynamics are out of control.

So these chronic disease management reversal companies can step in and find creative ways to do so – actually engaging members, doing the dirty work of meeting them where they are, providing them with 24/7 access to nutritionists and other care team members / coaches, and meaningfully drive behavior change in patients with pre or Type-2 diabetics and beyond (their average patient has a high BMI, 80 pounds overweight, aged 55+).

Sami compared Virta’s model to drive patient behavioral change to a self-driving car. With remote continuous care, Virta’s own employed physicians, and the rest of the care team, Virta creates a tight, closed feedback loop including a rapid sampling rate which allows the firm to individualize care and course correct quickly. Along with the feedback loop, Virta’s individualized nutrition protocols aim to eliminate hunger and cravings in the same way GLP-1 medications do – but obviously without the injection part.

Given the level of utilization exposure, Virta very clearly has to believe its engagement model is compelling. Since the utilization guarantee is measured by prescription volume for organizations with existing GLP-1 coverage, this announcement by Virta is a pretty savvy way to get your name out there in a space with a massive growth vector.

From Virta’s perspective, Sami told me that this is just the beginning for Virta in 2025. They hit $100M+ in ARR year over year with 80% growth in Q1 (suspiciously specific numbers) through working with 550 organizations and total lives coverage of 12M, and we should look to see more published results from Virta on the cardiometabolic front and adjacent areas. “When you reduce inflammation and insulin resistance, it’s amazing what can happen to the body,” Sami told me.

The Weekly Executive Summary

(how do you like the AI-generated depiction of physician corporatization? Sorry, couldn’t help myself)

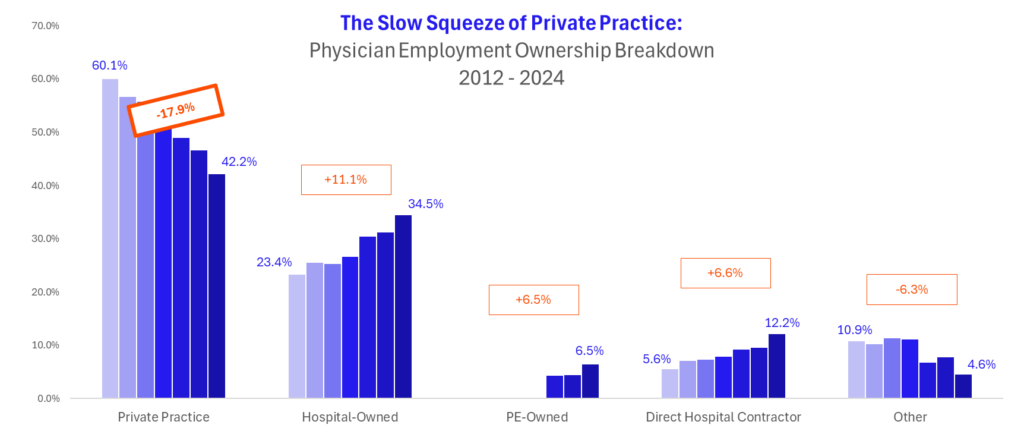

The AMA updated its report on physician employment dynamics across private practice, hospital-based, and private equity employment, and the consolidation trend continues. There are fewer private practice physicians today than there were a decade-plus ago, and this trend has only accelerated given recent inflationary pressures.

Why are physicians selling their practice? Besides retired shareholders wanting a pop prior to closing shop, here are the percentage of physicians who mentioned these factors as ‘high’ or ‘very high’:

- 70.8% – ability to negotiate higher rates

- 64.9% – improve access to costly resources (CAPEX, better equipment, etc.)

- 63.6% – reduce administrative and regulatory burden imposed by payors

- 55.1% – ease participation in risk-based payment models

- 48.0% – expand scope of services patients need

- 48.9% – better compete for employees in labor market

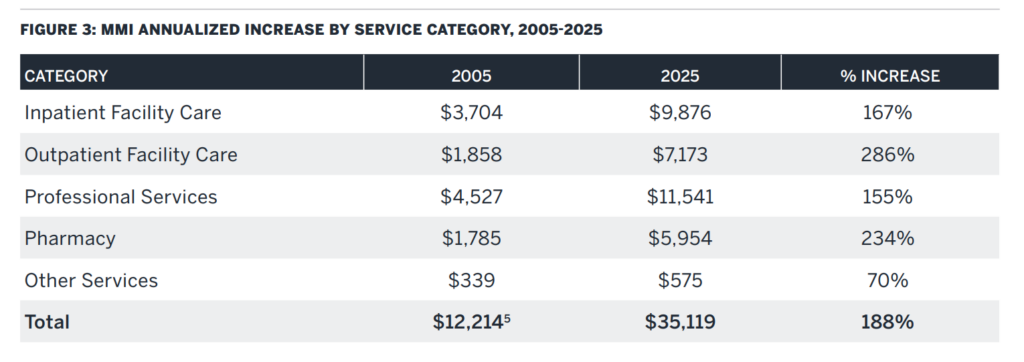

Milliman published its 2025 Milliman Medical Index this week, finding that an average family of four is spending $35,119 / year on healthcare across out of pocket, employer contributions, and employee contributions. Where’s the breaking point?

Join the thousands of healthcare professionals who read Hospitalogy

Subscribe to get expert analysis on healthcare M&A, strategy, finance, and markets.

No spam. Unsubscribe any time.

OpenEvidence is rumored to be raising $100M at a $3B valuation. If you recall, OpenEvidence announced a $75M raise at a $1B valuation…in February 2025. Between this and Abridge’s rumored $5.3B valuation, are we finding some incredible winners, or are we so back on dumping cash into digital health with reckless abandon? Notably, Sequoia is invested in OpenEvidence, and they also…sort of quietly invested into AI scribe startup Freed back in March, which seems to have come out of nowhere and seems like a pretty late entry into the game. Either way, they seem to be in love with the Doximity approach to building in healthcare – target physicians then sell their souls to Big Pharma monetize through pharmaceutical manufacturers.

Omada Health is expected to go public as soon as the end of this week at a ~$1.1B valuation. Just another billion dollar company in healthcare.

Kaufman Hall releases its June hospital flash report covering data thru April, and hospitals continue to see nice margin expansion in 2025, echoing my large health system analysis released last week.

Humana, seeing an opportunity, told congressional staffers this week that it supports changes to risk upcoding and billing practices