Happy Thursday, Hospitalogists.

No talking about healthcare spice or physician employment dynamics today! We’re simply recapping August and the major healthcare stories in an ultra-skimmable format for your viewing pleasure.

Do you like this monthly recap format as a send? Let me know as I’m experimenting with content style. Also – shoot me a message if I missed anything big in healthcare that I either should be covering or writing about.

Hope you all have a great weekend, fam. College football is nigh, and the hopes and dreams of millions of college football fans across the nation are at an all-time high (me included)!

Subscribe to Hospitalogy, my newsletter breaking down the finance, strategy, innovation, and M&A of healthcare. Join 20,500+ healthcare executives and professionals from leading organizations who read Hospitalogy! (Subscribe Here)

Healthcare August Recap: Major Headlines

Obesity Breakthrough: A landmark trial found that Novo’s obesity drug Wegovy lowers cardiovascular risk by 20%. This has massive implications, mainly for senior populations, in gaining wider coverage access for patients. (Link)

Epic, Microsoft, and Pals: Epic implemented a new ‘Partners and Pals’ program in August. Abridge became the first “Pal” of Epic, introducing its generative AI to assist a broader range of patients and providers. Along with the announcement, Microsoft and Epic expanded their AI collaboration to enhance the role of generative AI in healthcare, announcing Nuance as one of Epic’s Partner and Pals vendor program and embedding Nuance’s ambient documentation solution within Epic workflows, among other interesting clinician and administrative productivity tools. Epic also integrated Talkdesk into its ‘Partners and Pals’ program following the Abridge and Microsoft announcements.

PBM Disruption? In likely the biggest news headline of the week, Blue Shield of CA and its 4.8 million member footprint announced its intention to ditch CVS and is replacing that 3-letter void with an ‘unbundled’ consortium of vendors – Amazon Pharmacy for at-home drug delivery, Mark Cuban Cost Plus Drugs for benefit design and medication access, Prime Therapeutics, and Abarca to fill other existing drug benefit functions. Notably, CVS is still retaining the specialty drug book of business, which contains half of the spend. CVS also issued an 8-K on the matter, notably unconcerned about the loss of business especially given the specialty moat.

MSSP Results: The Medicare Shared Savings Program saved Medicare $1.8 billion in 2022 (0.24% savings), marking the sixth consecutive year of overall savings. Low-revenue ACOs, mainly composed of physicians and serving rural areas, earned more shared savings and led high-revenue ACOs in net savings per capita. (Link)

Amazon Updates:

- Amazon launches AWS Tools HealthScribe and HealthImaging: Amazon Web Services (AWS) announced the launch of a new HIPAA-eligible service called HealthScribe that healthcare software providers can use to build their own generative AI documentation & other solutions. HealthScribe is launching in general medicine and orthopedics first, and those building in the space can leverage AWS to manage the underlying infrastructure and healthcare-specific LLMs rather than needing to do so on their own. Stated differently, the AWS offering is a lego set for AI offerings. It’s enabling healthcare software providers to build solutions across generative AI use cases in healthcare. Related to the above was Amazon’s announcement in the imaging space, launching AWS HealthImaging. From the press release, HealthImaging will serve a similar function as HealthScribe in supporting the infrastructure and providing lego bricks needed to store, analyze, and share mass amounts of medical imaging data.

- Amazon Clinic Growth: Amazon Clinic is expanding its services nationwide, operating as a platform connecting several telehealth providers with patients for low-acuity conditions.

$14B Merger between Sanford and Fairview canceled: After a drawn out process, in which even Fairview’s associated academic medical center at the University of Minnesota opposed (even going as far as to request funds from the state to acquire its affiliated hospitals), the Sanford-Fairview Health Services merger has been called off. The merger would have created a giant in the Midwest at over 50 hospitals. Don’t forget that Sanford has failed at least 3 merger attempts in recent memory, the first one being Fairview a decade ago, then Intermountain Healthcare and UnityPoint Health more recently.

Enhabit’s Strategic Shift: Enhabit declared its aim to initiate a strategic alternatives process following some talk of this happening earlier in 2023. Given that we’ve seen major takeovers of home health players of late and the fact that Encompass orphaned its home health and hospice spinoff, I wouldn’t be surprised to see yet another sale in the space. (Link)

OHSU & Legacy Merger: Oregon Health & Science University announced its intent to merge with the financially challenged Legacy Health, signifying the latest in a line of attempted health system mergers within a local market, although the two do not have existing overlapping geography. In reality, the two players are likely getting their lunches eaten by larger players in the local market. As far as the attempted merger is concerned, OHSU will be ‘acquirer’ stepping into Legacy Health’s shoes through a member substitution and promising $1 billion in local community investment for the combined entity. The systems together generated around $6.5B in revenue, though each lost money in 2023. The combined system — with more than 32,000 employees and 100-plus locations, including 10 hospitals, and more than 3 million patient visits a year — will be the largest employer in the Portland metro area, and will focus on amplifying the region’s leadership in patient- and community-focused health care, education, research and innovation. (Press Release) (Link)

Kidney Care Race Heats Up: On August 23, Strive Health and Oak Street Health launched a national collaboration to provide value-based kidney care to people with stage 4 chronic kidney disease through end-stage kidney disease across Oak Street Health’s 21-state footprint. Through the partnership, Strive will work with Oak Street Health’s care team to help manage chronic kidney disease (CKD) patients to prevent hospitalizations, drive down costs, and improve overall patient care.

- Also on August 23, and as if on cue, Humana Inc. and Interwell Health announced an agreement for Humana’s Medicare Advantage members living with chronic kidney disease in 13 states and members across the country living with end-stage kidney disease. Under the agreement, Humana members get access to Interwell services: “With this new agreement, these members have access throughout their healthcare journey to Interwell’s comprehensive care and specialized resources, including 1,700 network nephrologists, renal care coordinators, and in-home virtual support from dietitians, nurses, social workers, pharmacists, and care coordinators.”

Demise of Cano Health: After a long and beleaguered journey to this point, including a lengthy board fight, going concern…concerns, a $150M loan at a 14% interest rate for a year-long lifeline, and a rescheduled Q2 earnings conference call, Cano Health posted dismal results on its Q2 earnings release. The Medicare Advantage-focused senior clinic care platform reported a 103.5% medical loss ratio, meaning that for every premium dollar earned, Cano paid out 103.5% in medical costs. The narrative is familiar if you’ve heard my post-mortem of Babylon – Cano Health went public via SPAC at an over-exuberant valuation (I’ve heard anecdotally that the winning bid was several multiple turns above any other PE offer). The firm operated / expanded into bad markets, and facilitated extremely sketchy, borderline criminal related party transactions. So you can see why this mismanagement situation quickly devolved into a board fight over the course of 2023. After almost selling to CVS back in October (side note: I bet CVS knows exactly how bad things were once they started the diligence process), Cano is exiting several markets, including California, New Mexico, Illinois, Puerto Rico, and Florida Medicaid. Look for an impending sale or otherwise, a bankruptcy press release coming soon.

Privia’s Expansion: Privia Health announced its entry into the Washington State healthcare market through its partnership with Walla Walla Clinic comprised of 50+ providers at 3 locations, serving as the anchor practice for the enablement company in the market. (Link)

Join the thousands of healthcare professionals who read Hospitalogy

Subscribe to get expert analysis on healthcare M&A, strategy, finance, and markets.

No spam. Unsubscribe any time.

CommonSpirit and AdventHealth divided up Centura Health’s hospital portfolio, folding the joint operating company back into the two parent organizations. Don’t forget that Centura previously purchased Steward Health’s 5-hospital portfolio in Utah after HCA was unsuccessful in capturing the bid. (Link)

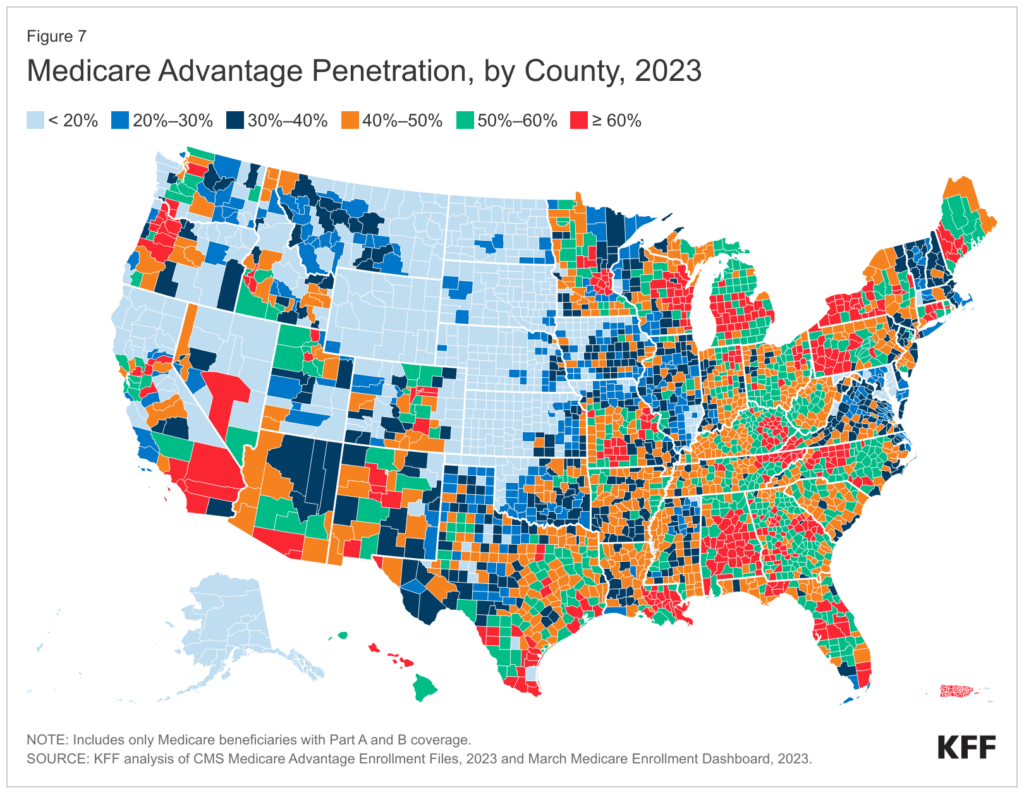

Medicare Advantage 2023: KFF highlighted several important trends in the Medicare Advantage space, including that 51% of enrollees are now on Medicare Advantage plans, and UnitedHealthcare and Humana nowcomprise about half of all MA enrollees. Very cool article and visualizations on trends throughout the Medicare Advantage landscape. (Link)

Kroger and Intermountain’s Select Health introduced a co-branded Medicare Advantage plan. The co-branded plan will be offered in Colorado, Idaho, Nevada, and Utah. Remember that SelectHealth is Intermountain’s MA subsidiary with over a million members. Meanwhile I’m just waiting for someone to partner with HEB down in Texas! Kroger has previously partnered with Elevance and Priority Health and there are several other co-branded plans out there in the wild. (Link)

Verily and OneOncology announced an interesting partnership to collaborate on cancer research to enable more efficient clinical trials. Verily will integrate its clinical trials management software into OneOncology’s platform. (Link)

Methodist Health System announced a partnership with Surgery Partners to develop and acquire ASCs in the North Texas market. (Link)

My essays from August:

- Amazon’s emerging healthcare strategy

- CVS bets the house: 4 takeaways from CVS’ Q2 report

- Who controls the healthcare spice?

- Physician dynamics are reaching a boiling point

That’s it for this week! If you enjoyed this post, subscribe to Hospitalogy, my newsletter breaking down the finance, strategy, innovation, and M&A of healthcare. Join 20,500+ healthcare executives and professionals from leading organizations who read Hospitalogy! (Subscribe Here)