How Health System M&A is Evolving

Link to Part 2 here

Today we’re diving deeper into the world of health system mergers. Specifically I’m talking about the Advocate-Aurora and Atrium $27 billion deal announced a couple of weeks ago.

If you enjoy reading Hospitalogy, I’d love your support by dropping a subscription. Sign up for Hospitalogy on Tuesdays and Thursdays here!

The essay will be split into 2 parts. Part 1 will provide context for the specific Atrium/Advocate merger, including how mergers have evolved over time and headwinds facing hospitals.

Then, next Thursday, Part 2 will cover why we’re keeping an eye on the future of population health management strategies as health system mergers evolve to prioritize risk and additional sources of revenue diversification, and we’ll make a prediction on whether or not the Advocate Aurora-Atrium and Intermountain-SCL mergers are likely to raise or lower prices based on historical precedent and the nature of each system’s operating model.

Also, for these next two weeks, I’m excited to be joined by Daran Gaus, who writes The Scroll. He knows everything value-based care (like, REALLY knows the space), so drop him a subscription!

Key Takeaways

Historically, large health systems have engaged in horizontal mergers to increase market share, gain leverage from payors for better rates, and expand access to resources. Such resources might include access to more physicians & specialties, shared staffing, new service lines, and cutting costs through combined purchase power.

In addition to the above, running hospitals is capital intensive and cost inflation from vendors and staffing are a constant pressure, eating up cash flow and margin. Some hospitals and health systems are forced to merge just to survive. This effect is most notable in the rural and critical access hospital sphere.

In the world of 2022, it’s pretty dang tough to run a hospital.

Here’s the problem, though. The hospital market is growing more and more concentrated. Hospital consolidation has developed an insane amount of notoriety for increasing prices. As a result, proposed mergers are increasingly failing state antitrust review due to hospital market concentration concerns.

Because of this antitrust concern, health systems are transforming their M&A strategy. In 2022, the two largest announced mergers between Intermountain/SCL and now Advocate-Aurora/Atrium have included pointed language around pursuing risk-based population health strategies, a focus on charity care, medical research, enhanced data analytics, and investment in digital health infrastructure. That strikes me as a major shift in the type of mega-merger we’ll be seeing from here on out.

The days and opportunities associated with consolidating JUST to boost market share and command higher payor rates are evaporating in the hospital market. From here on out, health system mega-mergers will look to open different doors that also benefit from economies of scale – like more venture investments into health tech infrastructure (for both the hospital and consumer) and the ability to get closer to the premium dollar to compete with the traditional insurer.

TL;DR – My primary thesis is that health system M&A strategy is shifting from horizontal (market power play) to vertical integration, thinking about upstream and downstream revenue, taking on risk, and becoming more of a fully integrated institution.

If you enjoy reading Hospitalogy, I’d love your support by dropping a subscription. Sign up for Hospitalogy on Tuesdays and Thursdays here!

Advocate/Atrium Merger Context

Let’s jump into the behind the scenes of the Advocate/Atrium merger. Advocate is no newbie to mergers. In 2014, the Illinois-based health system announced a merger with NorthShore Health in Illinois, which was ultimately struck down by the FTC in 2017. Turns out the merger would have resulted in 55% acute care market concentration at the time.

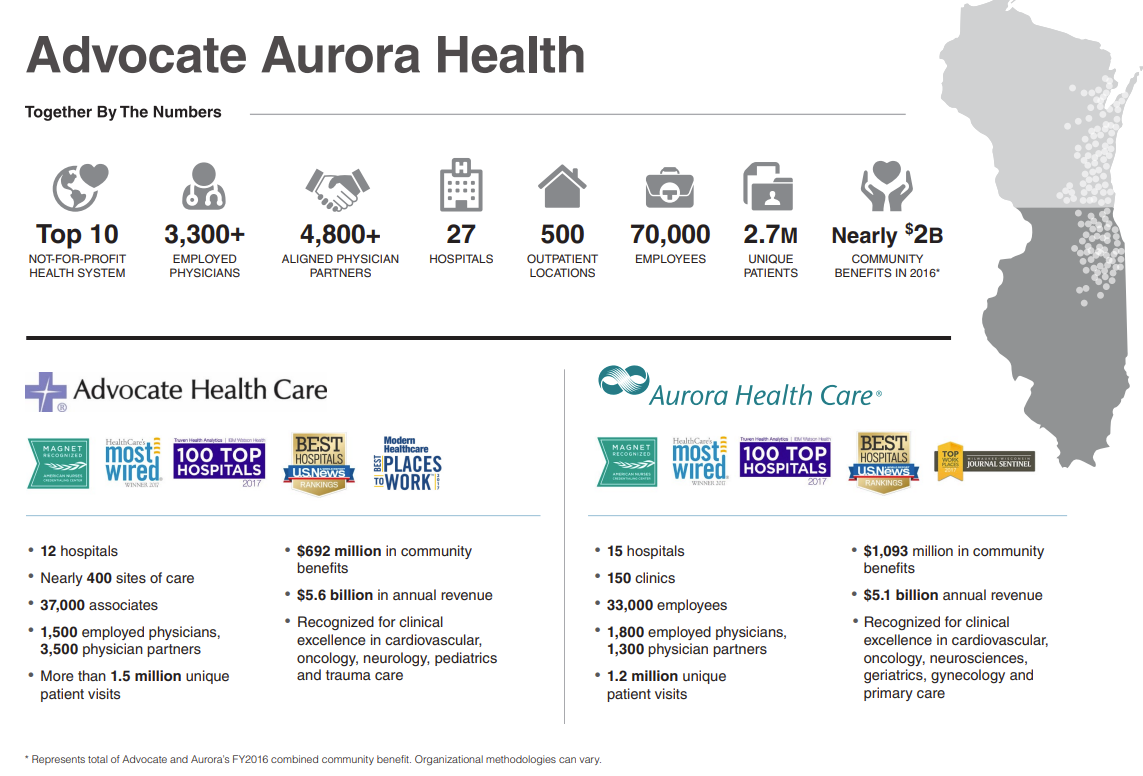

Then, in 2016 (while the NorthShore merger was still under review, mind you), Advocate Health merged with Aurora Health to create a 27-hospital footprint in Wisconsin and Illinois, around $11 billion in total revenue and good enough for the 11th largest health system at the time:

Join the thousands of healthcare professionals who read Hospitalogy

Subscribe to get expert analysis on healthcare M&A, strategy, finance, and markets.

No spam. Unsubscribe any time.

Since then, Advocate has been sniffing around the M&A market looking for another suitor.

In 2020, Advocate tried to merge with Beaumont Health to create a $17 billion system, but this attempt was ultimately called off after clinical leaders (nurses, physicians) voiced safety concerns. Beaumont is now “successfully” merged with Spectrum Health, by the way, after several failed attempts with multiple other health systems.

Finally, Advocate found a suitor in 2022 – Atrium Health.

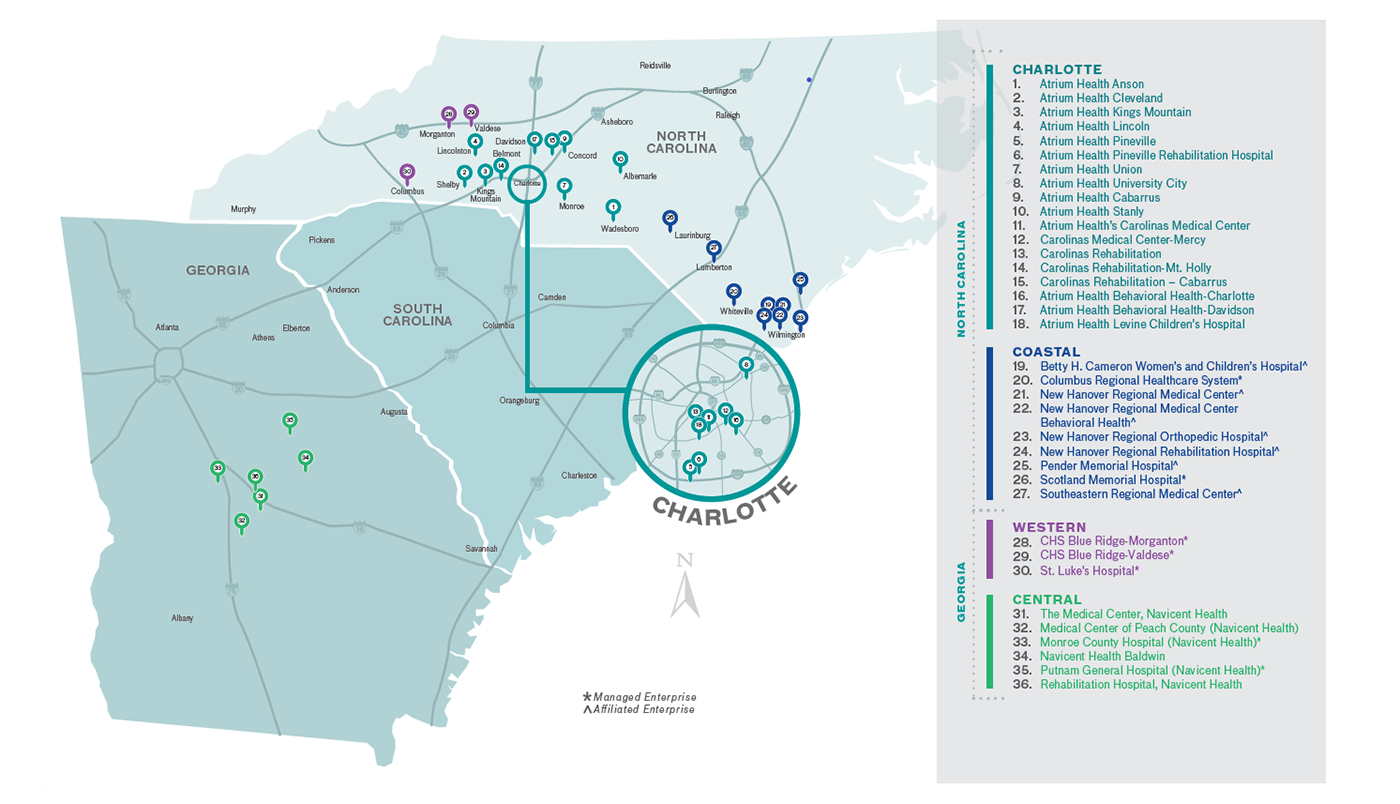

Charlotte, North Carolina-based Atrium Health enters the Advocate merger with around $11 billion in revenue. Atrium is fresh off the heels of another completed integration with Wake Forest Baptist Health, an academic-based institution, announced in late 2020.

Atrium’s footprint is connected throughout Georgia and the Carolinas:

Atrium Health, formerly known as the Carolinas Health System, has merged with Wake Forest Baptist Health, Navicent Health and Floyd Health in the past three years. The system lives in M&A integrations, apparently.

Summary of Key Advocate – Atrium Merger Provisions

Here’s the high-level overview of the AA merger.

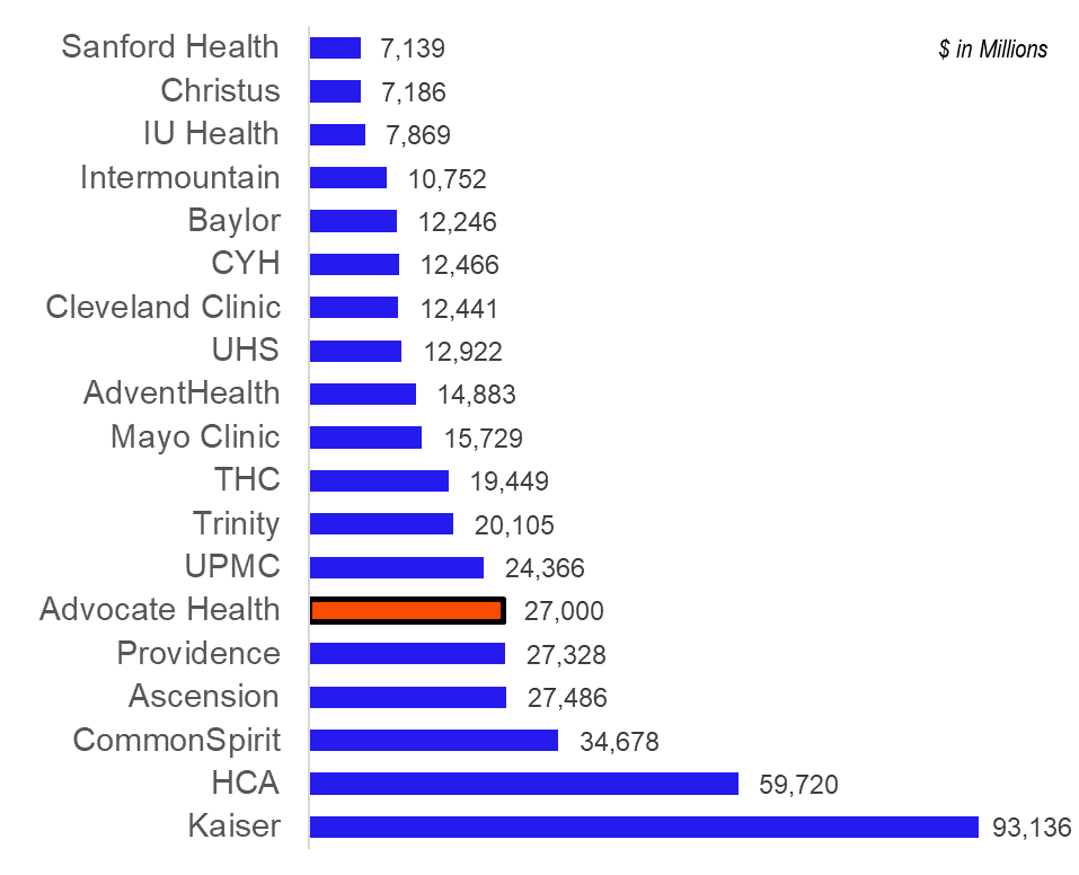

Advocate Aurora Health is merging with Atrium Health to create a $27 billion health system which will operate under a new name: Advocate Health.

The new system’s combined revenues puts it on par with that of Ascension & Providence at about $27 BILLION – good enough for the 6th largest health system in the U.S. (including Kaiser) I mean, that is just absolutely massive.

Revenue numbers as of full-year 2021:

Advocate’s new footprint will include:

- 67 hospitals

- 1,000 sites of care

- 7,600 physicians

- 150k employees

- 5.5 million patients

- 2.2 million lives through 15 ACOs and 60 value-based contracts (whatever that means)

- $5 billion in annual community benefit

- $2 billion pledged to address health equity

- Pledge to hire 20k more employees

- Operations across Illinois, Wisconsin, North Carolina, South Carolina, Georgia, and Alabama

You might be wondering – “how can there be any sort of synergy here? The two health systems are separated geographically. What’s going on?” Notably, Advocate Health will be structured as a joint operating company (JOC). Instead of just contributing assets in a specific area, the two systems appear to be layering the JOC on top of 100% of their combined footprint.

The thinking pervasive throughout most health system mergers is “bigger is better.” Even though rate plays and payor negotiation might not be as strong of a synergy here, there are other ways that a $27 billion institution can unlock value. I mean, there have to be, right? We’ll get into that a bit more in Part 2.

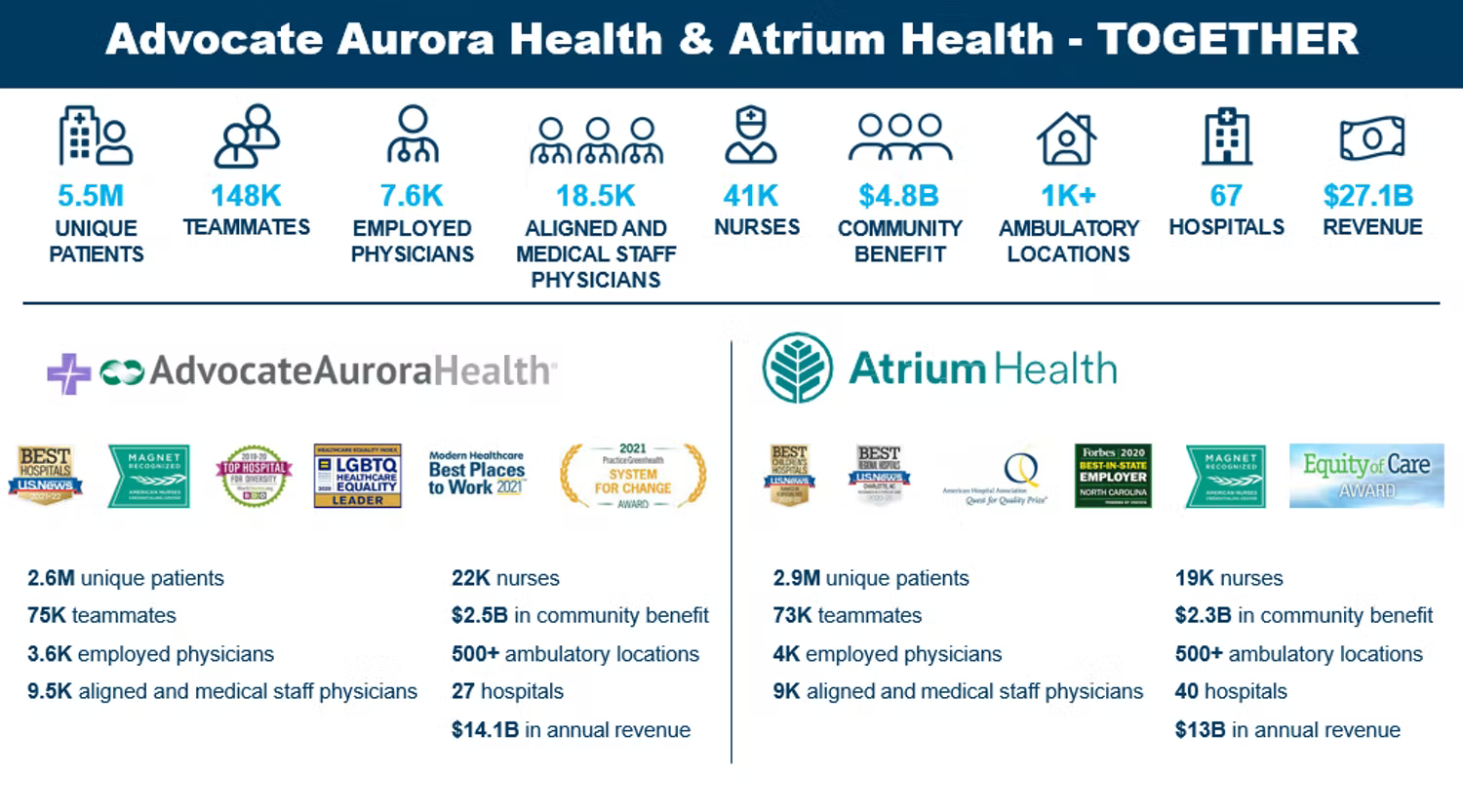

Here’s a good overview of the combined org from the press release. Like I mentioned and as you can probably imagine, the footprint is expansive:

Brief History of Health System Mergers and recent Hospital Activity

So, why do health systems merge? In the traditional sense, health systems conducted mergers for scale primarily related to rate plays and favorable expense management – better purchase agreements, contracted rates with vendors, and ability to share staffing & other resources, along with plenty of other synergies identified by a slew of consultants.

Some more notable examples of these kinds of mergers include Dignity / CHI to form CommonSpirit and Providence / St. Joseph’s to form Providence Health & Services about 5 years ago.

Some of the larger, more notable hospital & health system deals that have been announced within recent memory include the following:

- 6/5/2020: Steward Health Care physicians bought out their private equity partner Cerberus, acquiring a controlling stake in the privately held, for-profit health system. Steward is the largest physician owned health system in the country.

- 10/9/2020: Atrium Health and Wake Forest Baptist Health merged to create a $11 billion system with 42 hospitals.

- 6/17/2021: Spectrum Health and Beaumont Health merged to create a $13 billion system with 22-hospitals, now Michigan’s largest health system. Prior to the announcement, Beaumont had failed to merge with Advocate Aurora a year prior, and Summa Health before that.

- 8/2/2021: Steward Health Care acquired 5 hospitals from Tenet in South Florida for $1.1 billion.

- 8/3/2021: Piedmont Healthcare acquired 4 hospitals from HCA for $950 million.

- 9/8/2021: NorthShore University Health System and Edward Elmhurst merged to create a 9-hospital system with 25,000 employees across Illinois.

- 9/16/2021: Intermountain and SCL Health merged to create a 33-hospital conglomerate across 6 states.

- 9/21/2021: HCA acquired 5 hospitals from Steward Health Care in Utah.

- 2/3/2022: Centura Health purchased 2 hospitals from LifePoint Health

- 3/1/2022: Piedmont acquired University Health Care System, a 3-hospital system in east Georgia.

- 4/1/2022: Intermountain merges with SCL into a $14 billion health system in the Midwest and Mountain region.

- 4/19/2022: Trinity Health buys out CommonSpirit’s stake in MercyOne, a joint operating company and large health system player in Iowa

- 5/11/2022: Advocate-Aurora and Atrium Health announce the formation of a new joint operating company – Advocate Health – fully combining the two into one $27 billion health system while maintaining separate state operations. The JOC creates the 6th largest health system by revenue in the U.S.

In general, hospital deals are slowing down. We’ll increasingly start to see more creative strategic partnerships between health systems, or larger health system mergers. I’m betting that the larger, regional mergers will be structured similarly to the Intermountain/SCL and Advocate/Atrium deals. Meanwhile, I’m willing to bet that existing, scaled health systems will start to focus in on population health strategies.

Why Hospitals Merge.

Like I said in the intro, it’s tough out there for hospitals – in lots of cases, really their only option is to consolidate. Here’s a non-exhaustive list of things causing headaches for operators nationwide:

Labor Shortages & Inflation. Stemming from the pandemic and a piping hot reopening economy, the Great Resignation, and supply chain constraints, inflation and labor shortages are top of mind for healthcare executives. Like I covered in my Q1 review of publicly traded operators, hospitals saw a ton of travel agency costs, which dampened margin quite a bit – especially for the nonprofit operators.

Staffing comprises about half of a hospital’s cost structure, and 33% of nurses are planning to leave their current position. Burnout is at an all-time high in healthcare. Nursing shortages are projected to reach pretty dire levels by 2025. Turnover is costly as hell, so hospitals have been focused on retaining staff through signing bonuses and other initiatives. Once travel nurses return home, a sense of normalcy will return, but they’ll be getting some major base salary escalators. Still, that’s better than travel rates.

From a drugs & medical supply perspective, almost all hospitals in the U.S. reported facing procurement issues. Drug & equipment distributors will pass on their inflated costs to providers to maintain their already-low margins.

Finally, health systems & hospitals are dealing with general & administrative cost inflation, which will likely be the most variable. Hourly rates from lawyers, consultants, and other professionals will reflect inflation increases. Any travel costs, insurance expenses, utility bills, and more will reflect higher expenses.

Reimbursement. CMS is making changes to disproportionate share payments, while providing a pay bump of just 3.2%. Wage index adjustments (for elevated staffing costs) to Medicare payments will lag until CMS incorporates 2021 and 2022 data into the reimbursement formula. Further, boosted reimbursement from ‘Rona and the public health emergency will likely fizzle out sometime in 2022. Finally, Medicare sequestration (a mandatory 2% cut to reimbursement) will happen eventually…maybe. Unless the AHA gets its way!

Capital. Finally, interest rates are rising, tightening capital just a bit more. Hospitals refinancing debt will have to do so at higher rates and subsequent higher interest payments.

Is there an option besides merging? To combat various operational challenges, health systems are throwing around their weight and increasingly forming coalitions. For instance, health systems formed Civica Rx in 2018 to address drug shortages, Truveta in 2019 but picked up steam in 2021, a health system data platform, and now Evolve Health Alliance, a staffing agency sharing labor resources between participating hospitals to pare down travel nursing agency costs. Even UPMC created its own internal staffing agency.

- As the FTC and states continue to block mergers, I’m thinking that we’ll continue to see more collaborations and shared resources across hospitals rather than full-on horizontal mergers.

Antitrust.

Speaking of the FTC, THE biggest headwind to hospital M&A, healthcare gets a ton of antitrust scrutiny, especially when Democrats are in office. The Biden Admin made antitrust a high priority during its administrative run and has generally cracked down on mergers in healthcare along with state review.

There have been a number of health system mergers canceled or struck down in very recent memory for a number of reasons:

- Hackensack Meridian Health and Englewood Health called off their planned merger after an appeals court blocked the consolidation.

- Sentara Health and Cone Health canceled their merger in what would have created a $11.5 billion system with 17 hospitals.

- Baylor & Memorial Hermann chalked their plans after some strategic differences in what would have created a $14 billion Texas powerhouse.

- Dartmouth Health and GraniteOne Health canceled their merger after antitrust review raised similar market concentration concerns

- Lifespan and Care New England announced an intent to merge into a 7-hospital system, but shut down talks again in February 2022 after an anticipated challenge by the FTC.

Any hospital acquisition or merger that might result in increased market concentration over a certain threshold is very likely to be blocked in this transaction environment – especially in the Northeast.

Daran’s Thoughts: Why is antitrust a concern? A significant and growing body of research shows that provider consolidation leads to higher healthcare prices for insurers, and that this notion holds for both horizontal and vertical consolidation. Hospital mergers diminish market competition and increase health system negotiating leverage with payers (which means they have the bargaining power to force insurers to pay higher prices).

To put this into context, a recent RAND study found that employer-sponsored (read: commercial) health plans pay hospitals 244% more than Medicare prices in 2020. Hospitals claim that they must charge commercial insurers more (or cost-shift) to cover the losses from inadequate Medicare payments. Further, they argue their higher prices result from the need to offer unprofitable services and that quality improvements justify the price increases.

RAND researchers found no evidence to support the cost-shifting or quality premises. These price hikes do not stay with insurers, however, as they are an intermediary that passes these price increases onto employers (and employees by proxy) and taxpayers (insurance margins tend to hover around 4%). This isn’t a universal effect though. Hospital groups have presented some evidence that mergers can reduce hospital costs and improve outcomes. However, these cases tend to be the exception rather than the rule.

Got it, so you are saying that healthcare mergers are bad…right?

Not so fast. Mergers are just a tool, M&A activity isn’t inherently a good or bad thing. It is the intent behind the merger and what it achieves that matters. When mergers serve to perpetuate the volume-based, fee-for-service operating model which dominates the healthcare industry, then the increased negotiating leverage is likely to raise prices without accompanying quality improvement.

Madden’s Musing: These days, among the general population, hospital M&A is generally frowned upon since it’s notorious for increasing costs. But I’d encourage you to look at M&A from an operator’s perspective as well. Hospitals operate on razor thin margins. Yes, there’s a ton of bloat in these organizations, and hospitals could stand to lean up their expense profiles. But even the best run facilities – HCA – operate on a 20% EBITDA margin.

As hospitals continue to face pressures and headwinds outlined above – we’re going to continue to see M&A whether we like it or not, and whether it passes antitrust review or not.

Conclusion

Hospitals and health systems are reaching a critical mass in the U.S. where continued horizontal mergers are getting increasingly shut down for market concentration concerns.

As antitrust picks up, health systems are getting more creative with their merger strategy, offering more concessions, job growth in their local markets, higher levels of charity care, and investments into the local community.

In Part 2, Daran and I will cover the new value-based population health opportunity available to scaled health systems, and why we think it’s a winning strategy – if done the right way!

Link to Part 2 here

If you enjoy reading Hospitalogy, I’d love your support by dropping a subscription. Sign up for Hospitalogy on Tuesdays and Thursdays here!