Join 9,300+ smart, thoughtful healthcare folks and stay on top of the latest trends in healthcare. Subscribe to Hospitalogy today!

Introduction: Healthcare’s Streaming Moment.

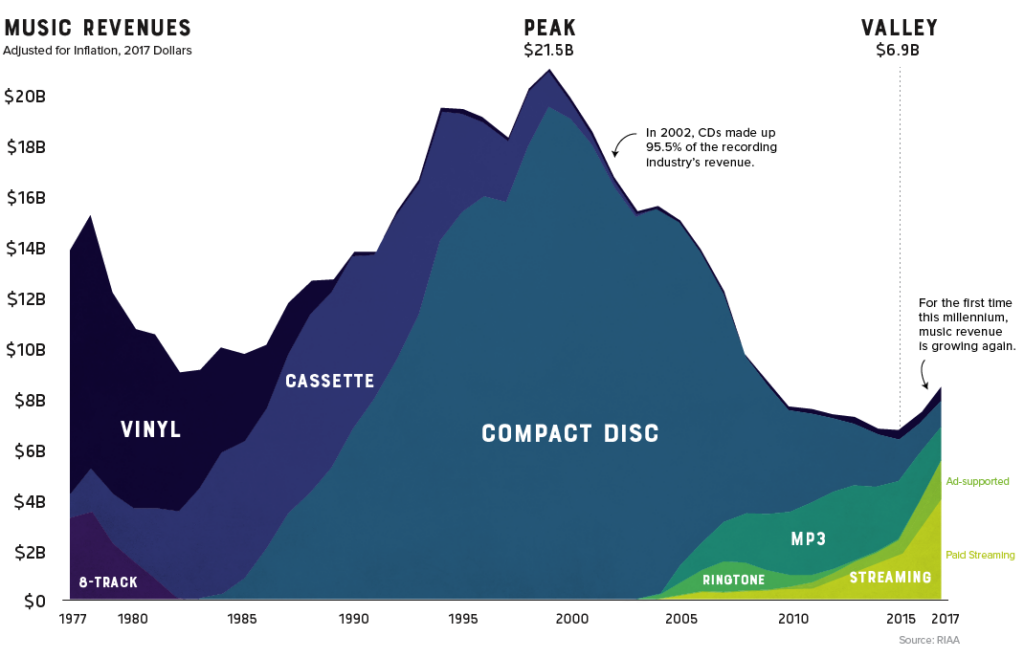

In the late 90’s, music industry sales were thriving. The rise of the CD had overtaken cassette players. Sales hit an all-time high of $21.5 billion.

But a fundamental shift – a chink in the armor – changed the game forever: the rise of the internet, mobile devices, and ultimately, music streaming.

Credit: Visual Capitalist. Source: https://www.visualcapitalist.com/music-industry-sales/

Over the next 15 years, music industry sales would experience a massive decline as better, consumer-friendly ways to consume audio emerged. Sales dropped to a low of $6.9B in 2015 and only recently recovered to the previous high set 20+ years ago.

I think we’d all agree that streaming is much a better consumer option than popping in a CD. The rise and fall and now rise again of the music industry is well-documented and widely known by everyone who is now happily tapped into Spotify, Apple Music, and other streaming ecosystems (I’m a Spotify loyalist myself).

The streaming format makes for a much better user experience. That experience forced the music industry to adapt.

Innovation and progress is inevitable, even in healthcare. That’s why the traditional hospital and health system will be forced to adapt to the new normal. The slow evolution of healthcare delivery will leave many hospitals with a similar fate to the CD or Blockbuster.

Post-pandemic, Hospitals have reached the beginning of their ‘streaming’ moment, and change will be painful but necessary.

Let’s dive into what’s impacting hospitals in 2022 and what ultimately will spur this change.

The hospital is dying: Key Takeaways.

- The traditional hospital business model is growing unsustainable.

- Long-term secular healthcare trends will force slow-moving, regulatory-heavy, acute-focused health systems to evolve their business models. Eventually.

- New entrants are optimizing care delivery for all sorts of patient cohorts beyond the four walls of the hospital and putting pressure on admissions.

- Over the coming decades, savvy health systems will find success through focusing on upstream and downstream revenue diversification. This focus will emulsify in the form of partnerships, joint ventures, outsourced functions, and a shift closer to the total premium dollar. I’ll cover this in next week’s post!

- Regardless of what happens, there will always be a need for hospitals for high acuity, trauma, and emergency situations.

P.S. / disclaimer – This is a thought experiment / thesis and a newsletter, a much more informal medium to express ideas on healthcare. I want Hospitalogy to keep an open mind with thoughts from readers. I welcome any and all opinions!

Challenges facing hospitals.

There’s no beating around the bush: operating a hospital is hard in 2022. Hospitals are cutting staff and inpatient service lines, operators with 140+ years of operation are shutting down, and access is hurting. The operating environment in 2022 and beyond will likely be very different than what we’ve experienced historically.

Here are some of the major challenges facing hospitals today. TL;DR: The macroeconomic environment does not set up well for hospital operations, and idiosyncratic issues specific to hospitals are adding fuel to the fire.

Labor: While the travel nursing and contract labor saga is slowly winding down, nursing and clinical shortages continue to plague hospitals. Nurses and unions in particular are striking, demanding higher pay in the highly inflationary environment. The labor challenges have a two-sided effect: on one hand, higher nursing salaries and benefits are eating into margin, leading to higher costs per patient day.

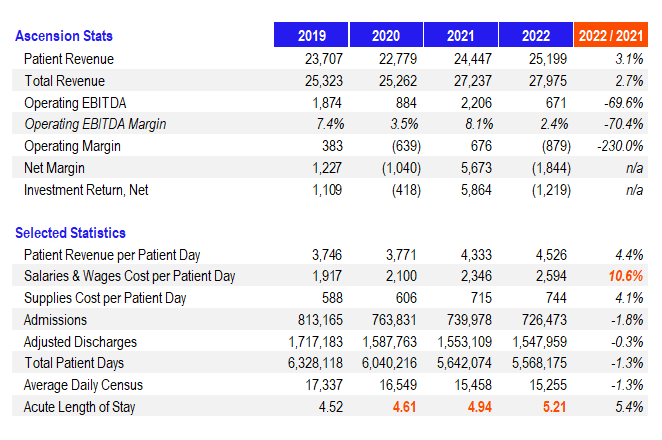

- To make things worse, nursing and clinical shortages are forcing hospitals to shutter admissions and close certain inpatient units. Post-acute labor shortages affect hospital ops too. It’s all connected. If there’s not a discharge destination available for a patient (AKA, SNF beds, inpatient rehab beds, etc.) take longer to become available) then length of stay trickles up and observation days erode DRG margins. Take Ascension’s recently released operating data, for instance. From FYE 2020 to 2022, average length of stay jumped almost 13%. So you’ve got patients in the hospital taking up beds in observation instead of getting the next high-acuity DRG in the door.

From a more human perspective, clinician and workforce burnout is at an all-time high as clinical personnel faced unprecedented hours, unsustainable staffing ratios, and trauma from the pandemic. Nurses and physicians are leaving (or considering leaving) their jobs in droves. Recruitment and retention in particular are top of mind for health systems nationwide to deal with the other aforementioned labor issues.

Inflation & Interest Rates: Although drugs & medical supplies and labor are the two big buckets on the income statement, hospitals are also dealing with overall inflation issues on the G&A side. Professional fees, purchased services, rent escalators being renegotiated with REITs, and utilities escalators are all impacting operations. The bigger picture with inflation relates to the Fed and interest rates. Just yesterday the Fed announced another 0.75% rate hike in an attempt to combat inflation sitting at 8%+. Sustained inflation will lead to higher rates expected to peak just below 5% in 2023 and will hurt unemployment. Hospitals don’t have flexible pricing power to deal with sustained inflation. Increasing rates along with poor market performance will lead to investment downgrades, higher borrowing costs, and more capital spent on interest/financing rather than investments into new service lines, geographic expansion, equipment, personnel, or technology.

Join the thousands of healthcare professionals who read Hospitalogy

Subscribe to get expert analysis on healthcare M&A, strategy, finance, and markets.

No spam. Unsubscribe any time.

Reimbursement: CMS threw hospitals a bone by updating the CMS final IPPS rule to 4.3%, but these types of rate increases are few and far between. Given that this update was the highest in the past 25 years, hospitals can’t rely on CMS to play ball, especially if inflationary pressures continue and a recession impacts tax dollars. As the Medicare trust fund dries up and Medicare Part A continues to suck up a big piece of the total pie, these types of lifts are unsustainable especially considering the coming utilization crunch with an aging population. On the commercial side, many private rate hikes are mandated and locked contractually until the next expiration / negotiation cycle; as a result, increases there will vary widely. For the largest operators, HCA and others are expecting commercial lifts in the mid to high single digits. Or you could pull a UHS and go out of network with payors not willing to negotiate higher rates. Hospitals face challenges in other categories adjacent to reimbursement like the constant, ongoing 340B battle, changes to disproportionate share payments (declining by $300 million in 2023), the end to the public health emergency designation, and the re-implementation of Medicare sequestration (mandatory cuts). Finally, the secular shift in payor mix as more Boomers enter Medicare / Medicare Advantage will shrink the available commercial honey pot and erode margin.

Legacy cost structures: Given the level of regulation and control, hospital administrative cost structures are traditionally bloated. Spreading out increased overhead over a shrinking operating/financial footprint in 2022 is a recipe for disaster. Forcing cost cuts and layoffs is not ideal, but hospitals will have to figure out ways to outsource and automate certain functions in the new normal. Hospitals will have to continually focus on cutting costs in each budget cycle, which is strenuous for ANY organization, let alone healthcare.

Shift to outpatient and structural changes in care delivery: Stakeholders including policymakers, payors, and digital health players are trying to keep patients OUT of the hospital. In addition, ambulatory surgery centers are more convenient and a more preferable setting for patients and payors (cheaper, under 24 hours) as opposed to overnight hospital stays (expensive, 24+ hours). As payors do everything they can to avoid hospital costs, risk-based models targeting specific patient populations grow more sophisticated, and the shift to outpatient services continues in settings like ASCs (a high-value fee for service offering), this secular trend has – and will continue to – put pressure on inpatient hospital admissions.

Conclusion: The new normal is here, and hospitals need to adapt.

The paradigm for hospitals has clearly shifted in 2022 and operators are scrambling to adapt to the new normal. Next week, I’ll be diving into what I think the future of the hospital will look like, whether it takes a decade or 50 years to get there.

It’s a fun thought experiment, and I hope you’ll join me!

Join 9,300+ smart, thoughtful healthcare folks and stay on top of the latest trends in healthcare. Subscribe to Hospitalogy today!