Join my Hospitalogy Membership! If you’re a VP or Director working in strategy or corporate development at a hospital, health system or provider organization, you will get a lot of value out of my community as I purpose-build the content, fireside chats, and conversations for this group. Join for free today.

Welcome to Hospitalogy, a newsletter breaking down healthcare finance, M&A, and strategy twice weekly. Join 42,000+ executives and investors from leading healthcare organizations by subscribing here!

Happy Tuesday Hospitalogists.

Today’s newsletter is a recap of major news (maybe even some rumors!) from the past month or so. Something on your radar I missed? Hit me up.

Let’s dive in!

Big Healthcare Stories:

The big stories from the month

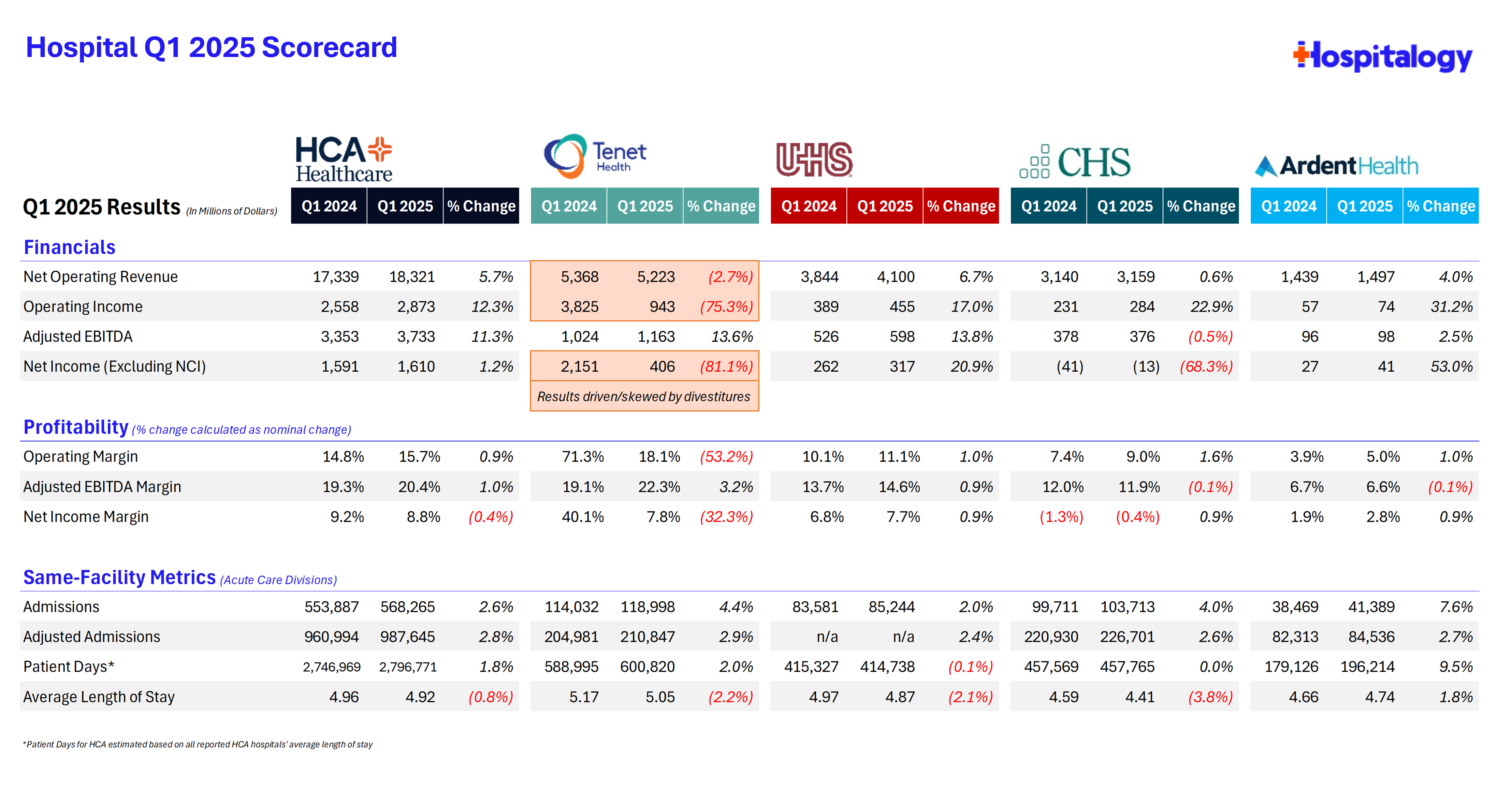

Hospital Q1 Round-up: A good quarter for the for-profit’s. Expanding margins, rising acuity, favorable payor mix from exchange volumes, decreased length of stay, a low point in the labor market, operating expense leverage, strong utilization and same-store volumes, murky tariff and policy (Medicaid) on Capitol Hill, supplemental payments flux, and more updates happened this quarter from the for-profit hospital crop. Read my breakdown here to get caught up.

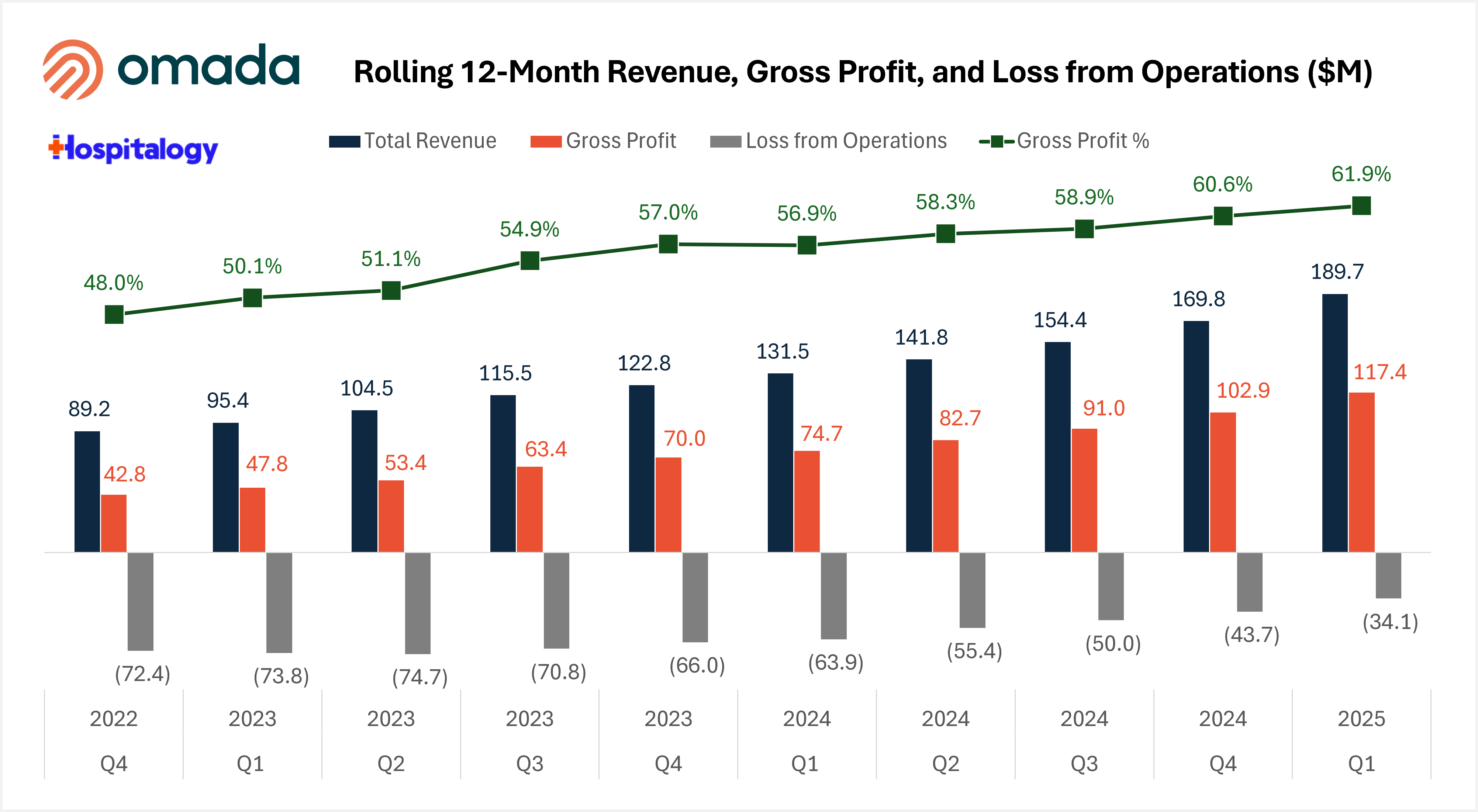

Hinge Health goes public, raising $437M: Hinge’s successful IPO debut, raising $437M at a $32 per share price and then trading up from there to $42+ as of this writing, bodes well for the rest of the late stage digital health crowd vying to go public later this year. In case you missed it, I covered Hinge’s Q1 2025 performance here (along with a snapshot of Omada), and I broke down Hinge’s S-1 and company thesis here.

Another Round from Abridge coming…at a reported $5B valuation: The Information reported (paywall) this week that Abridge, 2025’s absolute health tech darling, is reportedly in talks to raise another funding round at a reported $5B valuation. Abridge seems to notch a new enterprise partnership around its belt every time I look up and the ambient space is THE dominant use case for AI in healthcare particularly as the space expands into new downstream capabilities like coding and RCM functions. Abridge last raised a Series D publicly at a $2.75B valuation reported back in February. So for you math wizards and witches out there, Abridge would have doubled its value (on paper) in under half a year. $10B+ IPO inbound, you heard it here first.

Karoo Health Fundraising Rumors: Speaking of fundraising rumors, I have it on good authority that Karoo Health is raising – or starting to raise – a new round. Karoo last raised $3.4M in an oversubscribed seed round.

Sword Health Rumored to acquire Kaia Health: Classify this piece of news under the complete rumor mill, as I’ve heard it second hand and can’t take credit for it, but I have HEARD that Sword Health may be acquiring Kaia Health, which would be a huge consolidation / land grab play in the MSK space, especially as names like Hinge and Omada go public.

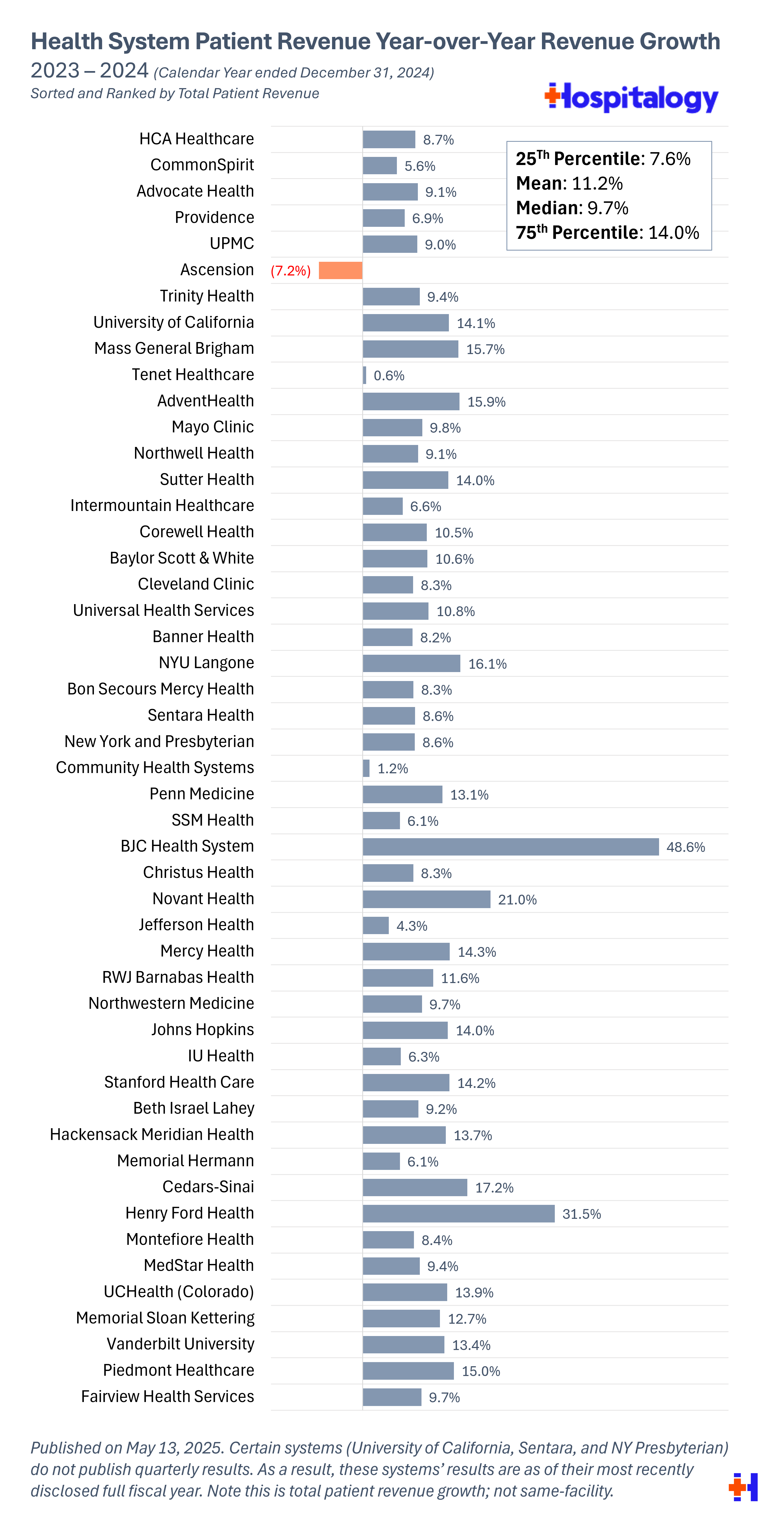

Largest Hospitals & Health Systems in 2025: As an original analysis by me, you can take a look at the top 80 health systems (for profit and nonprofit) by both total revenue and patient revenue through calendar year ended December 31, 2024. Check it out here. Here’s the top 50 health systems’ year-over-year growth sorted by total patient revenue:

Dialysis Giants Sued by Employers: A union-affiliated benefits fund, UFCW Local 1776, filed a proposed nationwide class action in Colorado against dialysis giants DaVita and Fresenius Medical Care, alleging that since at least 2021 the two firms conspired to carve up U.S. markets and impose parallel price hikes that artificially inflated outpatient dialysis costs by billions.

23andMe sold to Regeneron: Regeneron Pharmaceuticals agreed to acquire bankrupt genetic-testing firm 23andMe for $256 million via a bankruptcy auction, pledging to uphold existing privacy policies and ethically use more than 15 million customer DNA profiles. The transaction is expected to close in Q3 2025, excludes 23andMe’s Lemonaid Health telehealth arm (have to wonder where this ends up – probably in Fabric’s arms eh?), and follows the company’s bankruptcy filing after a 2023 data breach and declining consumer demand.

Northwell CEO Transition: A staple of the healthcare industry, Northwell Health President & CEO Michael Dowling announced he will step down on October 1, 2025, after more than two decades leading the system; he will be succeeded by Executive Vice President Dr. John D’Angelo.

Function Health acquires Ezra: Longevity startup Function Health acquired full-body MRI player Ezra and launched the first FDA-cleared, AI-powered full-body MRI that cuts scan time from 60 to 22 minutes, cutting the price of the service to $499 from over $1,500. The service is immediately available at nearly 100 U.S. locations, with plans to expand to over 1,000, and complements Function’s existing lab testing platform accessible at 2,200 Quest Diagnostics sites. Another big consolidating, land grab play in the longevity space.

Join the thousands of healthcare professionals who read Hospitalogy

Subscribe to get expert analysis on healthcare M&A, strategy, finance, and markets.

No spam. Unsubscribe any time.

New Mountain Capital’s Coding Consolidation Play: In a massive consolidating move within healthcare RCM and AI, New Mountain Capital combined its portfolio companies SmarterDx, Thoughtful.ai, and Access Healthcare into a single AI-powered platform named Smarter Technologies. Led by CEO Jeremy Delinsky, the new entity will serve over 200 clients (including 60+ hospital systems), process 400 million transactions, manage over $200 billion in annual revenue, and is projected to generate more than $800 million in revenue.

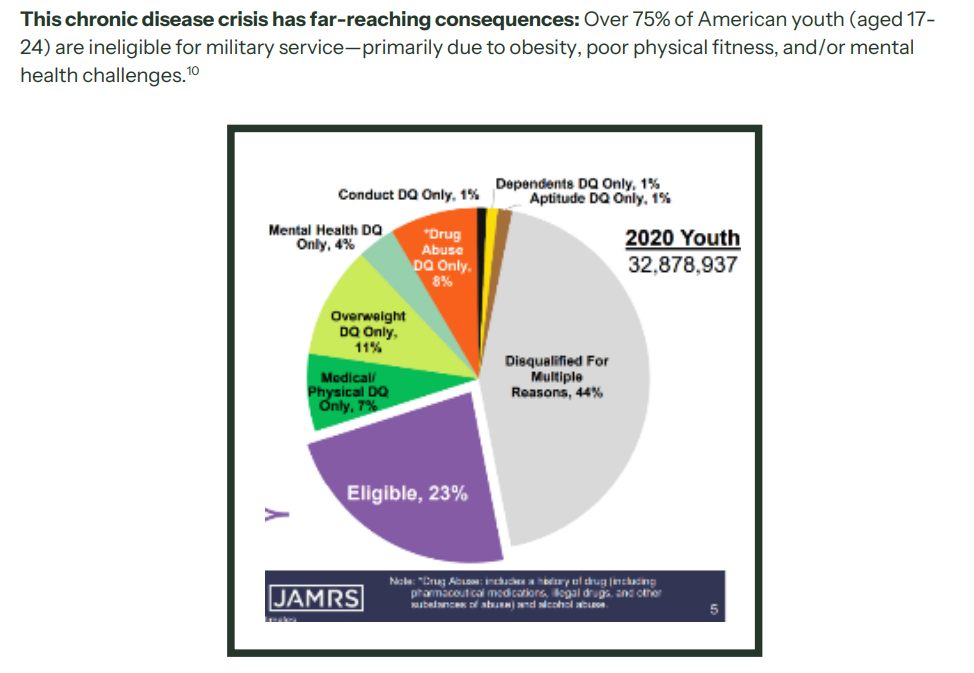

MAHA Report: Hospitalogists may recall that President Trump signed an executive order commissioning MAHA to provide an assessment of the current state of chronic disease and health in children within 100 days – and a next-steps strategy within 180 days. This report is now live, and top takeaways include identifying behavior and lifestyle drivers – shift to ultra-processed foods, exposure to environmental chemicals, prevalence of medications, physical activity levels (including sleep, and use of technology (AKA social media).

Other policy / compliance notables from May/April timeframe:

- Good Health Affairs overview of what’s in store for healthcare within the ‘Big Beautiful Bill’

- CMS proposed adding select Medicare Part B drugs to its price negotiation program for 2028, targeting high-cost injectables and biologics.

- CMS rolls out aggressive strategy to crack down on Medicare Advantage audits. CMS also plans to close a funding ‘loophole’ that allows states to boost Medicaid payments by inflating upper payment limit calculations.

- A federal judge extended an injunction preventing HHS from terminating billions in public health grant funding under the Ryan White HIV/AIDS Program.

- A federal court ruled in favor of HHS oversight over drug rebate calculations under the 340B program, ensuring manufacturers must comply with agency price-setting rules for covered entities.

- The DOJ opened an investigation into alleged kickbacks by CVS and Humana to brokers steering beneficiaries into their Medicare Advantage plans.

- Providence St. Joseph Health, Sutter Health, and Universal Health Services challenged CMS’s proposed Medicaid supplemental payment tariffs in federal court. The systems argue the rule unfairly caps reimbursement and jeopardizes safety-net funding.

- CMS proposed using AI-driven health risk assessments to adjust Medicare Advantage plan payments, seeking to improve accuracy in capturing beneficiary acuity. The initiative would tie advanced predictive analytics to risk scores and capitation rates.

Ascension posted a $466 million operating loss through fiscal Q3, attributed to escalating labor and supply expenses amid its portfolio realignment and reconstruction. It’s still trending on the path back to positive margin.

Northwell Health and Nuvance Health finalized their merger into a $23 billion, 28-hospital system.

Abundant Venture Partners has launched a new venture growth platform backed by 17 healthcare provider organizations to accelerate investment in early-stage care delivery and digital health companies. The platform will pool capital and provider expertise to support startups that address clinical workflow, patient engagement, and analytics needs. Yet another innovation play! Here’s the website.

OpenAI introduced HealthBench, an evaluation framework designed to test large language models for safety, reliability, and compliance in healthcare applications.

Mass General Brigham announced a $400 million investment to expand its primary care network and value-based care programs across Massachusetts.

Emory Healthcare expects to hit a 6% operating margin in FY 2025 following a two-year financial turnaround.

Aetna plans to exit several ACA exchange markets ahead of the 2026 plan year, citing adverse selection and unprofitable risk pools.

CVS Caremark designated Novo Nordisk’s Wegovy as its preferred GLP-1 obesity therapy on its formularies

Quick Notables

Collaborations, launches, and other tidbits to keep on your radar.

- SCAN Group acquires myPlace Health to scale its PACE program. I recently caught up with MyPlace’s CEO Robbie Pottharst, and he took time out of his day to walk me through the current state of PACE as well as MyPlace’s comprehensive platform. Keep these guys in mind in the space!

- DOJ blocks UnitedHealth-Amedisys hospice divestiture, per Hospice News.

- Cressey & Company buys majority of Paradigm to grow its hospice platform.

- Estes Park Health will join UCHealth with $30m in pledged capital.

- AMMC and Baptist Memorial sign LOI to pursue merger.

- HealthEdge has secured a strategic investment from Bain Capital to expand its payment and care management platform for payers and providers.

- Revelstoke Capital Partners made a significant growth investment in AOM Infusion, a provider of specialty pharmacy and infusion services.

- McKesson completed its acquisition of PRISM Vision Holdings, integrating its ophthalmic technology solutions into McKesson’s Medisoft and Trace platforms.

- Emergency Care Partners, staffing 1,100 EM physicians and clinicians with 1.5M annual patient visits across 63 locations, completed a recap with MidOcean Partners including a $100M preferred equity investment. Varsity Healthcare Partners and Regal Healthcare Capital Partners backed ECP prior.

- GI Alliance announced the acquisitions of Urology America and Potomac Urology, expanding its specialty practice network across five new states and 40+ new providers.

- U.S. Urology Partners secured a growth investment from General Atlantic to accelerate its multi-specialty urology platform.

Innovation / Products / Partnerships

- Michigan Medicine joins Longitude Health as the health system innovation engine’s newest member.

- UPMC Enterprises and Redesign launch Glimmer, a virtual chronic pain management clinic for PCPs.

- Sanford Health adds Cedar digital billing for 2.4 M rural patients.

- McFarland Clinic rolls out Nabla across 12 specialties, initially rolled out to 70 of 360 McFarland providers. Then Neighborhood Healthcare rolled out Nabla to up to 220 clinicians. Finally, Paragon Denali announced an integration with Nabla.

- Commure and HealthTap unveil plug-and-play virtual primary-care stack. Here’s the kicker: care delivery orgs already using Commure’s platform can plug into HealthTap for no upfront cost.

- Sutter study finds Abridge cuts note time and boosts clinician well-being.

- Riverside Health reports 11% wRVU jump after Abridge rollout.

- NYCBS adopts DeepScribe ambient OS in 30+ oncology sites. DeepScribe is going…deep in oncology

- Infinitus adds an AI voice agent that doubled early HRA rates.

- Austin providers adopt Watershed to share one record and target $2.2 B in waste cuts.

- Creyos and Redox will stream cognitive test data into EHRs.

- Ayble Health goes in-network with Priority Health for 500K members.

- GI Alliance selects IKS Health for RCM for its 900 gastroenterologists.

- Cost Plus Drugs partners with EverPharm and Morris & Dickson to deepen specialty drug supply – injectables, more specifically.

- Oshi Health goes full downside and puts fees at risk with a new ROI-backed GI care guarantee.

- Photon’s e-script tool shows real-time Amazon Pharmacy inventory.

- Teladoc Health acquired mental health platform UpLift to expand its covered telebehavioral health services for payers and employers.

Policy / Public Health

- NIH plans a real-time autism database via nationwide EHR integration.

- World’s first bladder transplant completed by UCLA–USC surgeons.

- Cancer report finds mortality falling but disparities persist, per study.

- CDC data show autism at 1 in 31 eight-year-olds, up 17% since 2020, per survey.

Hospitalogy Top Reads & Resources

My favorite healthcare essays from the week

Bass Berry & Sims released its 2025 healthcare M&A outlook, forecasting continued dealmaking driven by value-based care consolidation and digital health investment.

Cohere Health’s Series C and a case study on why they were created.

The Healthcare AI Adoption Index.

Reimagining the healthcare workforce of the future.

Women in focus: understanding women as digital health consumers

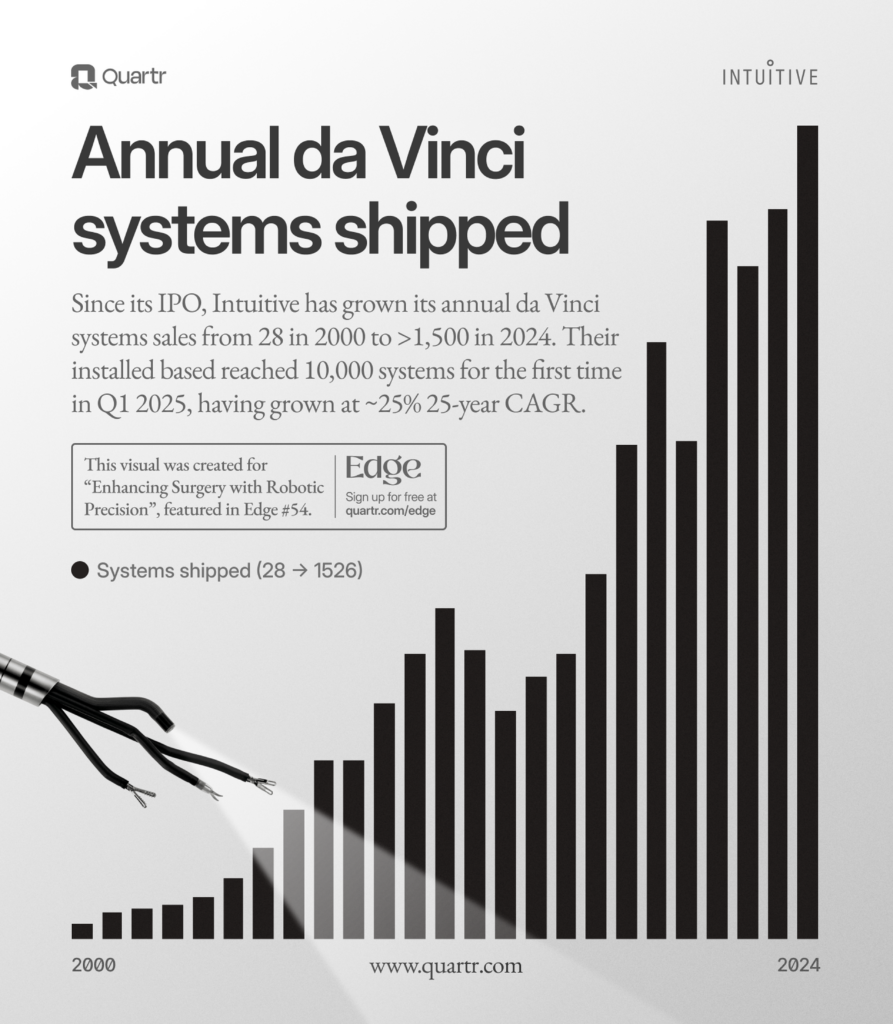

The history of Intuitive Surgical

Other posts of mine from the month:

- The health system innovation engine picks up speed in 2025

- The Fairview turnaround: talking all things Fairview Health Services with President and CEO James Hereford

- Value-based cardiology care the Karoo Health Way

- Privia’s Quiet Powerhouse: Q1 review

- HCA Q1 Breakdown